The following two-step binomial tree depicts the quarterly price path of an underlying share for an American

Fantastic news! We've Found the answer you've been seeking!

Question:

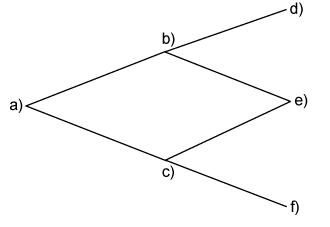

The following two-step binomial tree depicts the quarterly price path of an underlying share for an American call option. Each step represents a quarter of a year. The strike price of this option is $40 and the risk free rate is 7% pa.

a)Calculate the payoff of the option at point (b). Give your answer in dollars and cents to the nearest cent.

Payoff at point (b) = $

b)Calculate the value of the option at point (b). Give your answer in dollars and cents to the nearest cent.

Value of the option at point (b) = $

| Binomial Share Prices | ||

|---|---|---|

| a) | $40.00 | |

| b) | $42.80 | |

| c) | $37.20 | |

| d) | $45.80 | |

| e) | $39.80 | |

| f) | $34.60 | |

Expert Answer:

Related Book For

Posted Date: