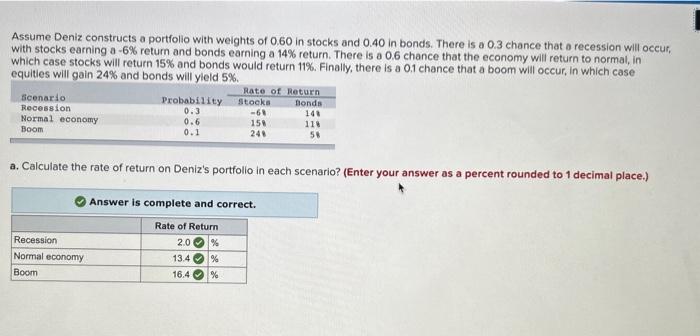

Question: the last answer is wrong please solve the last one Assume Deniz constructs a portfolio with weights of 0.60 in stocks and 0.40 in bonds.

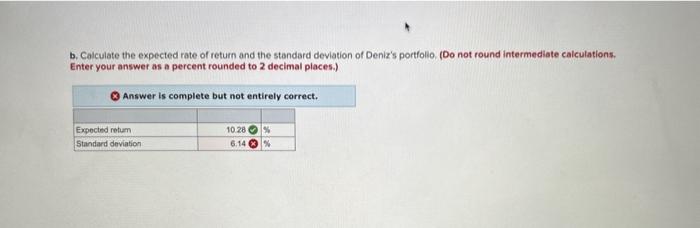

Assume Deniz constructs a portfolio with weights of 0.60 in stocks and 0.40 in bonds. There is a 0.3 chance that a recession will occur, with stocks earning a 6% return and bonds earning a 14% return. There is a 0.6 chance that the economy will return to normal, in which case stocks will return 15% and bonds would return 11\%. Finally, there is a 0.1 chance that a boom will occur, in which case equities will gain 24% and bonds will yield 5%. a. Calculate the rate of return on Deniz's portfolio in each scenario? (Enter your answer as a percent rounded to 1 decimal place.) b. Calculate the expected rate of return and the standard deviation of Deniz's portfolio, (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Answer is complete but not entirely correct

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts