You are a new supervisory accountant at Sportsman Company, reporting to the controller. On your second...

Fantastic news! We've Found the answer you've been seeking!

Question:

![[Replace with] The 22 March sales return entry should be a debit entry of ( $ 14,000 ). [Replace with] The 22 March sales](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2022/08/62e7bd4683022_1659354439367.jpg)

![Highlight #5 The 29 March customer account recovery credit entry of ( $ 14,000 ) is correct. [Delete text] [Replace with]](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2022/08/62e7bd46c56d8_1659354439653.jpg)

![Highlight #6 The 31 March credit sales debit entry of ( $ 636,250 ) is correct. [Original text] The 31 March credit sales](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2022/08/62e7bd46c8131_1659354439697.jpg)

![Highlight #7 The 31 March credit sales credit entry of ( $ 314,800 ) is correct. Choose an option [Delete text] [Replace w](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2022/08/62e7bd46c7b11_1659354439745.jpg)

![Highlight #8 The March ending balance of ( $ 791,650 ) is correct. [Delete text] [Replace with] The March ending balance s](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2022/08/62e7bd4613bd4_1659354439805.jpg)

Transcribed Image Text:

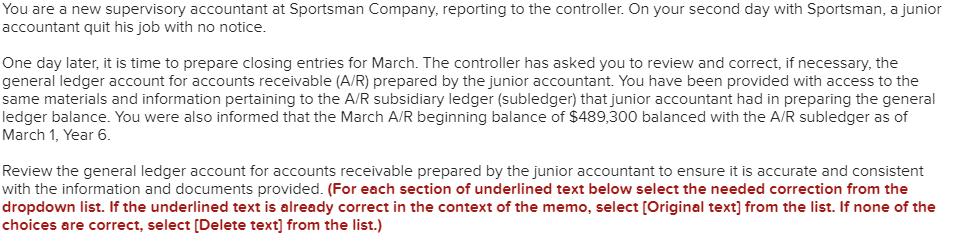

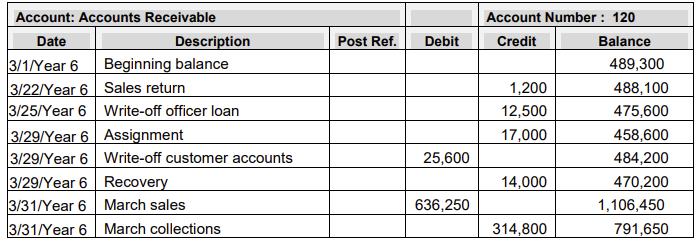

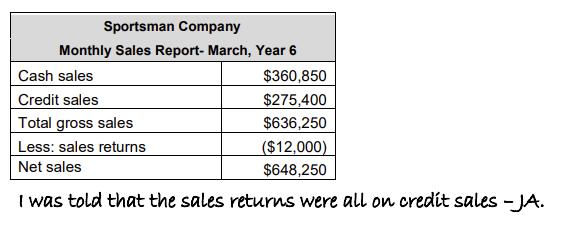

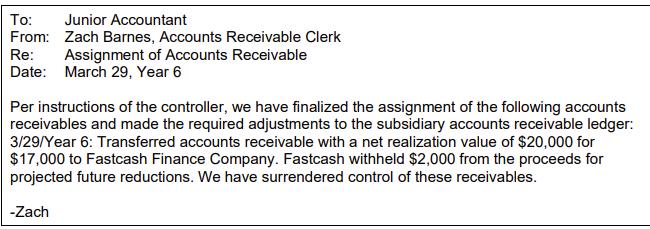

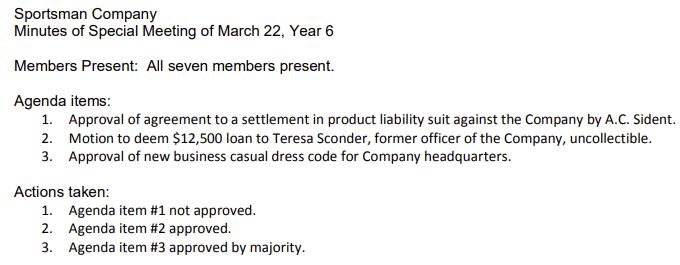

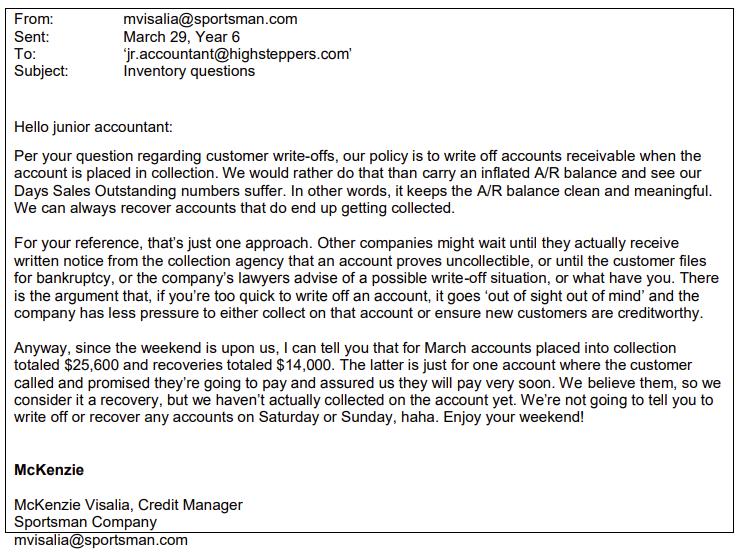

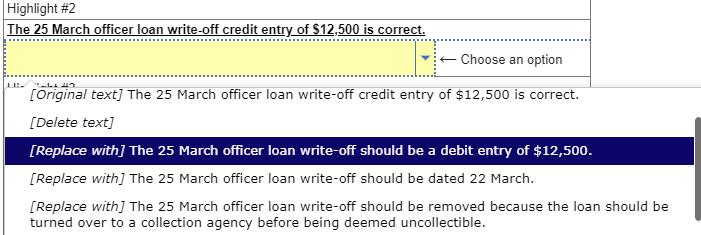

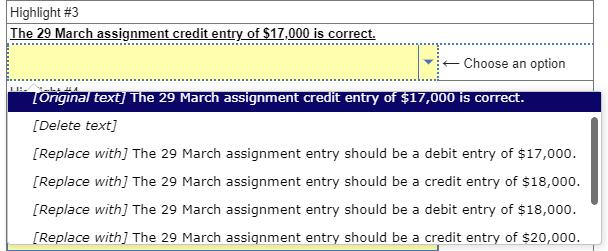

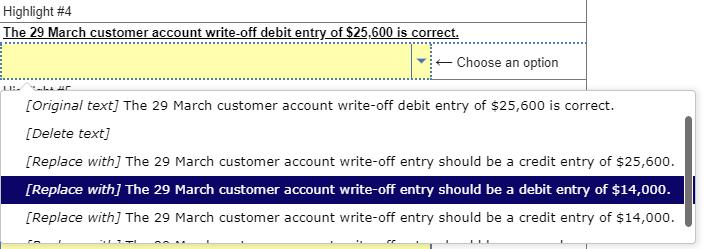

You are a new supervisory accountant at Sportsman Company, reporting to the controller. On your second day with Sportsman, a junior accountant quit his job with no notice. One day later, it is time to prepare closing entries for March. The controller has asked you to review and correct, if necessary, the general ledger account for accounts receivable (A/R) prepared by the junior accountant. You have been provided with access to the same materials and information pertaining to the A/R subsidiary ledger (subledger) that junior accountant had in preparing the general ledger balance. You were also informed that the March A/R beginning balance of $489,300 balanced with the A/R subledger as of March 1, Year 6. Review the general ledger account for accounts receivable prepared by the junior accountant to ensure it is accurate and consistent with the information and documents provided. (For each section of underlined text below select the needed correction from the dropdown list. If the underlined text is already correct in the context of the memo, select [Original text] from the list. If none of the choices are correct, select [Delete text] from the list.) Account: Accounts Receivable Date Description 3/1/Year 6 Beginning balance 3/22/Year 6 Sales return 3/25/Year 6 Write-off officer loan 3/29/Year 6 Assignment 3/29/Year 6 Write-off customer accounts 3/29/Year 6 Recovery 3/31/Year 6 March sales 3/31/Year 6 March collections Post Ref. Debit 25,600 636,250 Account Number: 120 Credit 1,200 12,500 17,000 14,000 314,800 Balance 489,300 488,100 475,600 458,600 484,200 470,200 1,106,450 791,650 Sportsman Company Monthly Sales Report-March, Year 6 Cash sales Credit sales Total gross sales Less: sales returns Net sales I was told that the sales returns were all on credit sales -JA. $360,850 $275,400 $636,250 ($12,000) $648,250 Sportsman Company Cash Receipts Report - March, Year 6 Cash sales Collections on credit sales Total cash receipts $360,850 $314,800 $675,650 To: Junior Accountant From: Zach Barnes, Accounts Receivable Clerk Assignment of Accounts Receivable Re: Date: March 29, Year 6 Per instructions of the controller, we have finalized the assignment of the following accounts receivables and made the required adjustments to the subsidiary accounts receivable ledger: 3/29/Year 6: Transferred accounts receivable with a net realization value of $20,000 for $17,000 to Fastcash Finance Company. Fastcash withheld $2,000 from the proceeds for projected future reductions. We have surrendered control of these receivables. -Zach Sportsman Company Minutes of Special Meeting of March 22, Year 6 Members Present: All seven members present. Agenda items: 2. 1. Approval of agreement to a settlement in product liability suit against the Company by A.C. Sident. Motion to deem $12,500 loan to Teresa Sconder, former officer of the Company, uncollectible. Approval of new business casual dress code for Company headquarters. 3. Actions taken: 1. Agenda item #1 not approved. 2. Agenda item #2 approved. 3. Agenda item #3 approved by majority. From: Sent: To: Subject: mvisalia@sportsman.com March 29, Year 6 'jr.accountant@highsteppers.com' Inventory questions Hello junior accountant: Per your question regarding customer write-offs, our policy is to write off accounts receivable when the account is placed in collection. We would rather do that than carry an inflated A/R balance and see our Days Sales Outstanding numbers suffer. In other words, it keeps the A/R balance clean and meaningful. We can always recover accounts that do end up getting collected. For your reference, that's just one approach. Other companies might wait until they actually receive written notice from the collection agency that an account proves uncollectible, or until the customer files for bankruptcy, or the company's lawyers advise of a possible write-off situation, or what have you. There is the argument that, if you're too quick to write off an account, it goes 'out of sight out of mind' and the company has less pressure to either collect on that account or ensure new customers are creditworthy. Anyway, since the weekend is upon us, I can tell you that for March accounts placed into collection totaled $25,600 and recoveries totaled $14,000. The latter is just for one account where the customer called and promised they're going to pay and assured us they will pay very soon. We believe them, so we consider it a recovery, but we haven't actually collected on the account yet. We're not going to tell you to write off or recover any accounts on Saturday or Sunday, haha. Enjoy your weekend! McKenzie McKenzie Visalia, Credit Manager Sportsman Company mvisalia@sportsman.com Highlight #1 The 22 March sales return credit entry of $1,200 is correct. H Choose an option [Replace with] The 22 March sales return entry should be a debit entry of $14,000. [Replace with] The 22 March sales return entry should be a credit entry of $14,000. [Replace with] The 22 March sales return entry should be a debit entry of $12,000. [Replace with] The 22 March sales return entry should be a credit entry of $12,000. [Replace with] The 22 March sales return entry should be removed. Highlight #2 The 25 March officer loan write-off credit entry of $12,500 is correct. Choose an option EB. Cal 47. [Original text] The 25 March officer loan write-off credit entry of $12,500 is correct. [Delete text] [Replace with] The 25 March officer loan write-off should be a debit entry of $12,500. [Replace with] The 25 March officer loan write-off should be dated 22 March. [Replace with] The 25 March officer loan write-off should be removed because the loan should be turned over to a collection agency before being deemed uncollectible. ← Highlight #3 The 29 March assignment credit entry of $17,000 is correct. - Choose an option LA [Original text] The 29 March assignment credit entry of $17,000 is correct. [Delete text] [Replace with] The 29 March assignment entry should be a debit entry of $17,000. [Replace with] The 29 March assignment entry should be a credit entry of $18,000. [Replace with] The 29 March assignment entry should be a debit entry of $18,000. [Replace with] The 29 March assignment entry should be a credit entry of $20,000. Highlight #4 The 29 March customer account write-off debit entry of $25,600 is correct. 1.11. Choose an option ALLER [Original text] The 29 March customer account write-off debit entry of $25,600 is correct. [Delete text] [Replace with] The 29 March customer account write-off entry should be a credit entry of $25,600. [Replace with] The 29 March customer account write-off entry should be a debit entry of $14,000. [Replace with] The 29 March customer account write-off entry should be a credit entry of $14,000. DETAL Highlight #5 The 29 March customer account recovery credit entry of $14,000 is correct. LE. PALLE [Delete text] Choose an option [Replace with] The 29 March customer account recovery entry should be a debit entry of $14,000. [Replace with] The 29 March customer account recovery entry should be a credit entry of $25,600. [Replace with] The 29 March customer account recovery entry should be a debit entry of $25,600. [Replace with] The 29 March customer account recovery entry should be removed until the customer begins paying on the account. Highlight #6 The 31 March credit sales debit entry of $636,250 is correct. LELA47 - Choose an option [Original text] The 31 March credit sales debit entry of $636,250 is correct. [Delete text] [Replace with] The 31 March credit sales entry should be a credit entry of $636,250. [Replace with] The 31 March credit sales entry should be a debit entry of $275,400. [Replace with] The 31 March credit sales entry should be a debit entry of $263,400. [Roplaco with The 21 March credit calor ontor should be a dobit ontne of $214 900 Highlight #7 The 31 March credit sales credit entry of $314,800 is correct. LE. ← Choose an option Lohtyinar cexcy me 31 March credit sales creant entry of $314,800 is correct. [Delete text] [Replace with] The 31 March credit sales entry should be a debit entry of $314,800. [Replace with] The 31 March credit sales entry should be a credit entry of $275,400. [Replace with] The 31 March credit sales entry should be a credit entry of $263,400. [Replace with] The 31 March credit sales entry should be a credit entry of $360,850. Highlight #8 The March ending balance of $791,650 is correct. - Choose an option [Delete text] [Replace with] The March ending balance should be $406,300. [Replace with] The March ending balance should be $409,300. [Replace with] The March ending balance should be $383,800. [Replace with] The March ending balance should be $392,300. You are a new supervisory accountant at Sportsman Company, reporting to the controller. On your second day with Sportsman, a junior accountant quit his job with no notice. One day later, it is time to prepare closing entries for March. The controller has asked you to review and correct, if necessary, the general ledger account for accounts receivable (A/R) prepared by the junior accountant. You have been provided with access to the same materials and information pertaining to the A/R subsidiary ledger (subledger) that junior accountant had in preparing the general ledger balance. You were also informed that the March A/R beginning balance of $489,300 balanced with the A/R subledger as of March 1, Year 6. Review the general ledger account for accounts receivable prepared by the junior accountant to ensure it is accurate and consistent with the information and documents provided. (For each section of underlined text below select the needed correction from the dropdown list. If the underlined text is already correct in the context of the memo, select [Original text] from the list. If none of the choices are correct, select [Delete text] from the list.) Account: Accounts Receivable Date Description 3/1/Year 6 Beginning balance 3/22/Year 6 Sales return 3/25/Year 6 Write-off officer loan 3/29/Year 6 Assignment 3/29/Year 6 Write-off customer accounts 3/29/Year 6 Recovery 3/31/Year 6 March sales 3/31/Year 6 March collections Post Ref. Debit 25,600 636,250 Account Number: 120 Credit 1,200 12,500 17,000 14,000 314,800 Balance 489,300 488,100 475,600 458,600 484,200 470,200 1,106,450 791,650 Sportsman Company Monthly Sales Report-March, Year 6 Cash sales Credit sales Total gross sales Less: sales returns Net sales I was told that the sales returns were all on credit sales -JA. $360,850 $275,400 $636,250 ($12,000) $648,250 Sportsman Company Cash Receipts Report - March, Year 6 Cash sales Collections on credit sales Total cash receipts $360,850 $314,800 $675,650 To: Junior Accountant From: Zach Barnes, Accounts Receivable Clerk Assignment of Accounts Receivable Re: Date: March 29, Year 6 Per instructions of the controller, we have finalized the assignment of the following accounts receivables and made the required adjustments to the subsidiary accounts receivable ledger: 3/29/Year 6: Transferred accounts receivable with a net realization value of $20,000 for $17,000 to Fastcash Finance Company. Fastcash withheld $2,000 from the proceeds for projected future reductions. We have surrendered control of these receivables. -Zach Sportsman Company Minutes of Special Meeting of March 22, Year 6 Members Present: All seven members present. Agenda items: 2. 1. Approval of agreement to a settlement in product liability suit against the Company by A.C. Sident. Motion to deem $12,500 loan to Teresa Sconder, former officer of the Company, uncollectible. Approval of new business casual dress code for Company headquarters. 3. Actions taken: 1. Agenda item #1 not approved. 2. Agenda item #2 approved. 3. Agenda item #3 approved by majority. From: Sent: To: Subject: mvisalia@sportsman.com March 29, Year 6 'jr.accountant@highsteppers.com' Inventory questions Hello junior accountant: Per your question regarding customer write-offs, our policy is to write off accounts receivable when the account is placed in collection. We would rather do that than carry an inflated A/R balance and see our Days Sales Outstanding numbers suffer. In other words, it keeps the A/R balance clean and meaningful. We can always recover accounts that do end up getting collected. For your reference, that's just one approach. Other companies might wait until they actually receive written notice from the collection agency that an account proves uncollectible, or until the customer files for bankruptcy, or the company's lawyers advise of a possible write-off situation, or what have you. There is the argument that, if you're too quick to write off an account, it goes 'out of sight out of mind' and the company has less pressure to either collect on that account or ensure new customers are creditworthy. Anyway, since the weekend is upon us, I can tell you that for March accounts placed into collection totaled $25,600 and recoveries totaled $14,000. The latter is just for one account where the customer called and promised they're going to pay and assured us they will pay very soon. We believe them, so we consider it a recovery, but we haven't actually collected on the account yet. We're not going to tell you to write off or recover any accounts on Saturday or Sunday, haha. Enjoy your weekend! McKenzie McKenzie Visalia, Credit Manager Sportsman Company mvisalia@sportsman.com Highlight #1 The 22 March sales return credit entry of $1,200 is correct. H Choose an option [Replace with] The 22 March sales return entry should be a debit entry of $14,000. [Replace with] The 22 March sales return entry should be a credit entry of $14,000. [Replace with] The 22 March sales return entry should be a debit entry of $12,000. [Replace with] The 22 March sales return entry should be a credit entry of $12,000. [Replace with] The 22 March sales return entry should be removed. Highlight #2 The 25 March officer loan write-off credit entry of $12,500 is correct. Choose an option EB. Cal 47. [Original text] The 25 March officer loan write-off credit entry of $12,500 is correct. [Delete text] [Replace with] The 25 March officer loan write-off should be a debit entry of $12,500. [Replace with] The 25 March officer loan write-off should be dated 22 March. [Replace with] The 25 March officer loan write-off should be removed because the loan should be turned over to a collection agency before being deemed uncollectible. ← Highlight #3 The 29 March assignment credit entry of $17,000 is correct. - Choose an option LA [Original text] The 29 March assignment credit entry of $17,000 is correct. [Delete text] [Replace with] The 29 March assignment entry should be a debit entry of $17,000. [Replace with] The 29 March assignment entry should be a credit entry of $18,000. [Replace with] The 29 March assignment entry should be a debit entry of $18,000. [Replace with] The 29 March assignment entry should be a credit entry of $20,000. Highlight #4 The 29 March customer account write-off debit entry of $25,600 is correct. 1.11. Choose an option ALLER [Original text] The 29 March customer account write-off debit entry of $25,600 is correct. [Delete text] [Replace with] The 29 March customer account write-off entry should be a credit entry of $25,600. [Replace with] The 29 March customer account write-off entry should be a debit entry of $14,000. [Replace with] The 29 March customer account write-off entry should be a credit entry of $14,000. DETAL Highlight #5 The 29 March customer account recovery credit entry of $14,000 is correct. LE. PALLE [Delete text] Choose an option [Replace with] The 29 March customer account recovery entry should be a debit entry of $14,000. [Replace with] The 29 March customer account recovery entry should be a credit entry of $25,600. [Replace with] The 29 March customer account recovery entry should be a debit entry of $25,600. [Replace with] The 29 March customer account recovery entry should be removed until the customer begins paying on the account. Highlight #6 The 31 March credit sales debit entry of $636,250 is correct. LELA47 - Choose an option [Original text] The 31 March credit sales debit entry of $636,250 is correct. [Delete text] [Replace with] The 31 March credit sales entry should be a credit entry of $636,250. [Replace with] The 31 March credit sales entry should be a debit entry of $275,400. [Replace with] The 31 March credit sales entry should be a debit entry of $263,400. [Roplaco with The 21 March credit calor ontor should be a dobit ontne of $214 900 Highlight #7 The 31 March credit sales credit entry of $314,800 is correct. LE. ← Choose an option Lohtyinar cexcy me 31 March credit sales creant entry of $314,800 is correct. [Delete text] [Replace with] The 31 March credit sales entry should be a debit entry of $314,800. [Replace with] The 31 March credit sales entry should be a credit entry of $275,400. [Replace with] The 31 March credit sales entry should be a credit entry of $263,400. [Replace with] The 31 March credit sales entry should be a credit entry of $360,850. Highlight #8 The March ending balance of $791,650 is correct. - Choose an option [Delete text] [Replace with] The March ending balance should be $406,300. [Replace with] The March ending balance should be $409,300. [Replace with] The March ending balance should be $383,800. [Replace with] The March ending balance should be $392,300.

Expert Answer:

Answer rating: 100% (QA)

Accounts Receivable for the month of march Date Description Debit Credit Balance 03Jan Beginning bal... View the full answer

Related Book For

Business Statistics A First Course

ISBN: 978-0321979018

7th edition

Authors: David M. Levine, Kathryn A. Szabat, David F. Stephan

Posted Date:

Students also viewed these accounting questions

-

Since 1984, all automobiles have been manufactured with a middle tail-light. You have been hired to answer the following question: Is the middle tail-light effective in reducing the number of...

-

In practice, there is often a tendency to simplify approximations of cost-behavior patterns, even though the true underlying behavior is not simple. Choose from the following graphs AH the one that...

-

Since 1935, there have been 11 changes of prime minister in Canada, including Pierre Trudeau's re-election in 1980 after a period in Opposition. The political party of each new prime minister is...

-

As our energy structure transitions toward renewable fuels, forest-based biomass fuels benefit from this transition. What are the likely effects of this transition on consumers, producers, and the...

-

John Brown, 62 years old, has been at the State Bank for 40 years. For the past 20 years, he has worked in the banks investment department. During his first 15 years in the department, it was managed...

-

a. Describe briefly the legal rights and privileges of common stockholders. b. Use a pie chart to illustrate the sources that comprise a hypothetical company's total value. Using another pie chart,...

-

Explain the differences between the various types of e-commerce marketplaces.

-

The following transactions apply to Jova Company for 2016, the first year of operation: 1. Issued $10,000 of common stock for cash. 2. Recognized $210,000 of service revenue earned on account. 3....

-

A 5 000-N weight is held suspended in equilibrium by two cables. Cable 1 applies a horizontal force to the right of the object and has a tension, T. Cable 2 applies a force upward and to the left at...

-

The Tusquittee Company is a retail company that began operations on October 1, 2018, when it incorporated in the state of North Carolina. The Tusquittee Company is authorized to issue 100,000 shares...

-

As a result of the COVID lockdown in Victoria you have created a blog site which discusses various aspects of insurance. On your site you have a Q & A section where you invite questions from your...

-

The bonds of Simons, Inc. carry a 89 monthly coupon and mature in six years. Bonds of equivalent risk yield 9.5% What is the market value of Simons's bonds? (4 points) The bonds of Simons, Inc. carry...

-

Compare the federal regulatory agencies that oversee the activities and operations of credit unions, savings and loan associations and savings banks, and security brokers and dealers. In what ways...

-

If an interest rate is currently 6% and a lending institution announces a 25 basis point increase, what percentage increase does this represent? Calculate the straight-line and sum-of-years-digits...

-

For every buyer of, say, a call option, there must of course also be a seller. Why would someone sell a call option on some shares he or she already owned? How would this be different than buying a...

-

The Clinton administration proposed in the spring of 1993 to shorten the average maturity of the federal debt to reduce interest outlays in the budget. How would the administration do this, and what...

-

Describe the type of the object x in the following declarations in English (for example: int **x: x is a pointer to a pointer to integer) int *x [10]; int (*x) (); int (**[]));

-

d. The characteristic equation of a control system is given by s+2s+8s+12s+20s+16+16=0. Determine the number of the roots of the equation which lie on the imaginary axis of s-plane

-

Data were collected on the typical cost of dining at American-cuisine restaurants within a 1- mile walking distance of a hotel located in a large city. The file Bundle contains the typical cost (a...

-

In Problem 13.6 on page 470, you used the total worldwide revenue ($ millions) and full time voluntary turnover (%) data stored in Best Companies to predict the number of full time jobs added. Using...

-

The bottling division of Sweet Suzys Sugarless Cola maintains daily records of the occurrences of unacceptable cans flowing from the filling and sealing machine. The data in Colaspc lists the number...

-

Electronic devices contain electric circuits etched into wafers made of silicon. These silicon wafers are sealed with an ultrathin layer of silicon dioxide, in a process known as oxidation. This can...

-

Using the data in Exercise 2: a. Find the first and third quartiles of the profit. b. Find the median profit. c. Find the upper and lower outlier boundaries. d. Are there any outliers? If so, list...

-

For each of the following scatterplots, state the type of association that is exhibited: Choices: positive linear, negative linear, positive nonlinear, negative nonlinear, weak linear. b. d. e.

Study smarter with the SolutionInn App