The Plastics Division of the United Chemical Co. manufacture s and sells a line of raw materials

Question:

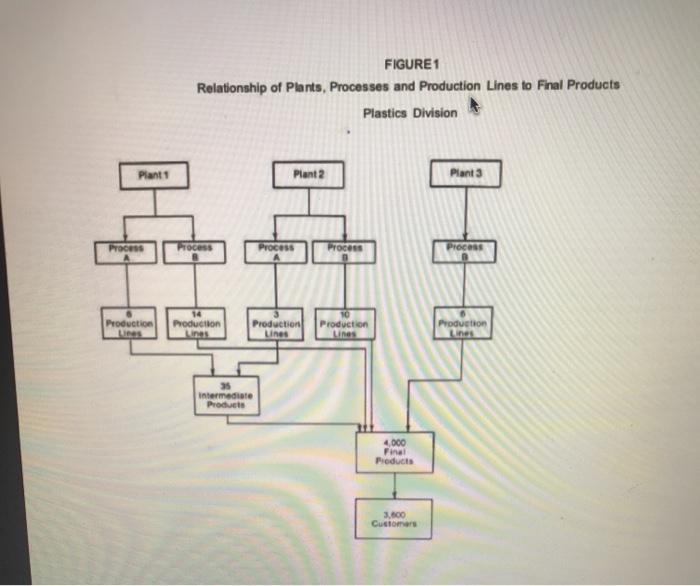

The Plastics Division of the United Chemical Co. manufacture s and sells a line of raw materials used by plastic converters in the fabrication of components fordurable goods manufacture. The Plastics Division has three manufacturing plantsthat employ a two-step process using 39 production lines. They manufacture 4,000 final products (grade/color combinations) for sale to 3,600 customers. Figure 1 (below) describes the production facilities.

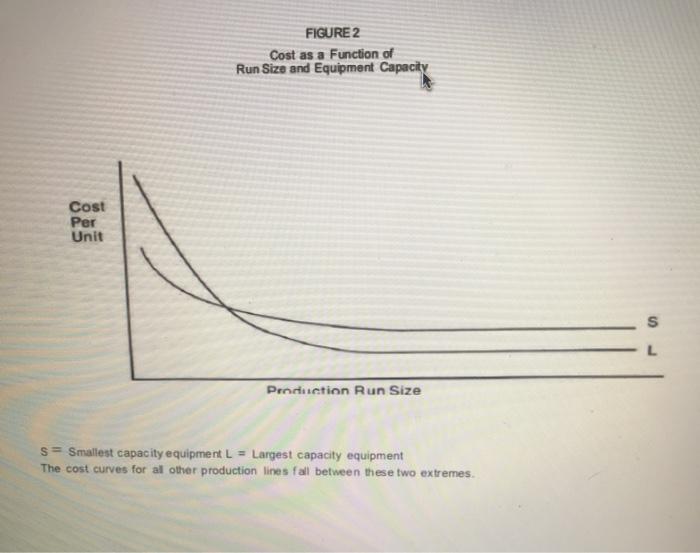

There are significant differences among the various production lines. Some grades of products can only be produced on certain lines. There are differences in equipment capacity that dictates the run size that is most efficient in each line (see Figure 2 below for run size/cost relationships for the range of equipment sizes). These differences in the production lines require constant monitoring by production scheduling in order to match the mix and volume of sales orders with the production capabilities to achieve the most economic production results. The Plastics Division uses a standard cost system for evaluating the performance of the production facilities.

The financial reports being routinely prepared for use by division management currently include:

1) Income statement,balance sheet, and cash flow statement for the division asa whole.

2) Standard cost performance reports for manufacturing.

Upon special request, individual product-cost estimates are made. These estimates are usually used in pricing considerations.

The Current Environment

The division has grown rapidly in the past several years.Consequently, the business has become more complex because of the large number of customers, products, and production lines. The marketing department views the market (3,600 customers) asbeing made up of five major segments and twenty sub segments.

The controller, Bill Brown, has observed that the decisions being made by the manufacturing manager are quite different from the decisions required of the marketing manager. Brown concluded that the different decisions require different financial information. He believed that through financial analysis his staff could provide marketing with data that could be used to guide marketing strategy and improve the profitability of the division. Brown observed that the lowest unit selling price of a product was about 30 percent of the division's highest priced product, and that the lowest unit cost was about 25 percent of the highest unit cost. He therefore reasoned that there must be a wide variation in profitability from product to product, customer to customer, and transaction to transaction. He concluded that a system was needed that would clearly define the profitability of each sale in order to provide the basis for marketing emphasis and pricing. However, significant questions remained in his mind.

Required

Brown recognizes that the current evaluation processes no longer meet United’s needs.

Brown has been asked by senior management to recommend changes that could be made to the profit analysis system so it better meets the different needs of the marketing, and manufacturing managers.

Required:

1. What are the critical information needs of (a) the marketing manager, (b) the manufacturing manager, and (c) the general manager?

How should a profitability analysis system use standard/budgeted cost data?

How should a profitability analysis system be different from a manufacturing performance measurement system since they both use cost data and if so why?

What changes should Brown recommend United consider making? Explain the advantages these changes would bring.

Expert Answer:

1 a The goal as a marketing manager in a construction company is to generate leads for the sales team It requires a lot of information about external sources competitors opportunities as well as inter... View the full answer

Financial Management Principles and Applications

ISBN: 978-0134417219

13th edition

Authors: Sheridan Titman, Arthur J. Keown, John H. Martin