Question: The previous two problems asked for the price to Johnson at a market rate of 9% followed by a price after 1 year has passed

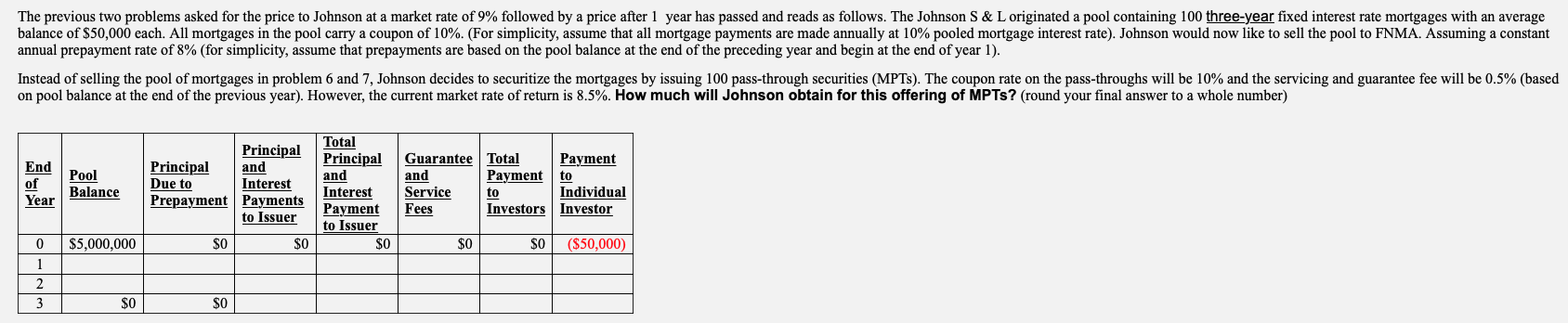

The previous two problems asked for the price to Johnson at a market rate of 9% followed by a price after 1 year has passed and reads as follows. The Johnson S&L originated a pool containing 100 three-year fixed interest rate mortgages with an average balance of $50,000 each. All mortgages in the pool carry a coupon of 10%. (For simplicity, assume that all mortgage payments are made annually at 10% pooled mortgage interest rate). Johnson would now like to sell the pool to FNMA. Assuming a constant annual prepayment rate of 8% (for simplicity, assume that prepayments are based on the pool balance at the end of the preceding year and begin at the end of year 1). Instead of selling the pool of mortgages in problem 6 and 7, Johnson decides to securitize the mortgages by issuing 100 pass-through securities (MPT). The coupon rate on the pass-throughs will be 10% and the servicing and guarantee fee will be 0.5% (based on pool balance at the end of the previous year). However, the current market rate of return is 8.5%. How much will Johnson obtain for this offering of MPTs? (round your final answer to a whole number) End of Pool Balance Principal Principal and Due to Interest Prepayment Payments to Issuer Total Principal and Interest Payment to Issuer $0 Guarantee Total and Payment Service to Fees Investors Payment to Individual Investor Year 0 $5,000,000 $0 $0 $0 SO ($50,000) 11" 2 3 $0 SO The previous two problems asked for the price to Johnson at a market rate of 9% followed by a price after 1 year has passed and reads as follows. The Johnson S&L originated a pool containing 100 three-year fixed interest rate mortgages with an average balance of $50,000 each. All mortgages in the pool carry a coupon of 10%. (For simplicity, assume that all mortgage payments are made annually at 10% pooled mortgage interest rate). Johnson would now like to sell the pool to FNMA. Assuming a constant annual prepayment rate of 8% (for simplicity, assume that prepayments are based on the pool balance at the end of the preceding year and begin at the end of year 1). Instead of selling the pool of mortgages in problem 6 and 7, Johnson decides to securitize the mortgages by issuing 100 pass-through securities (MPT). The coupon rate on the pass-throughs will be 10% and the servicing and guarantee fee will be 0.5% (based on pool balance at the end of the previous year). However, the current market rate of return is 8.5%. How much will Johnson obtain for this offering of MPTs? (round your final answer to a whole number) End of Pool Balance Principal Principal and Due to Interest Prepayment Payments to Issuer Total Principal and Interest Payment to Issuer $0 Guarantee Total and Payment Service to Fees Investors Payment to Individual Investor Year 0 $5,000,000 $0 $0 $0 SO ($50,000) 11" 2 3 $0 SO

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts