Question: The problem I need help with is part B #9. Also if you see something wrong let me know. Thanks for your help. Better By

The problem I need help with is part B #9.

Also if you see something wrong let me know. Thanks for your help.

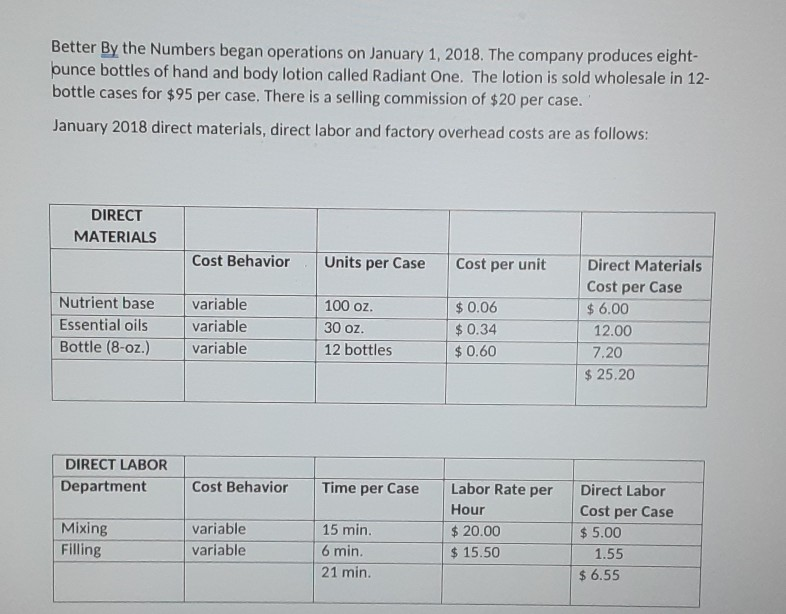

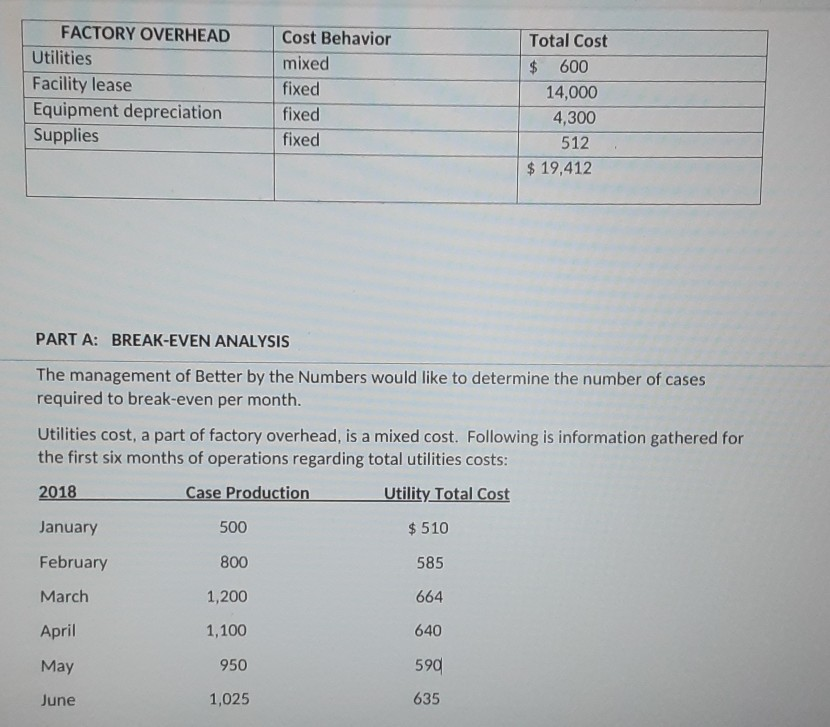

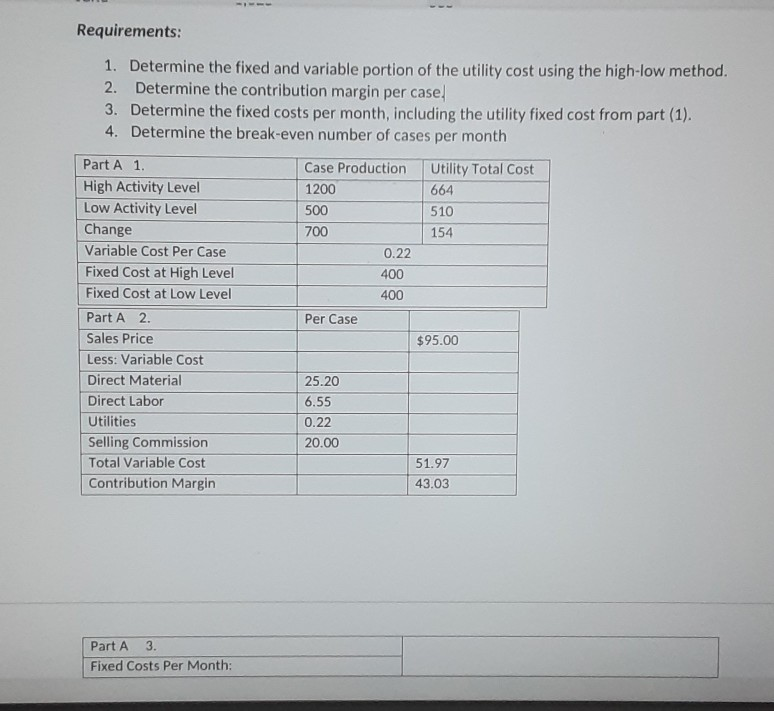

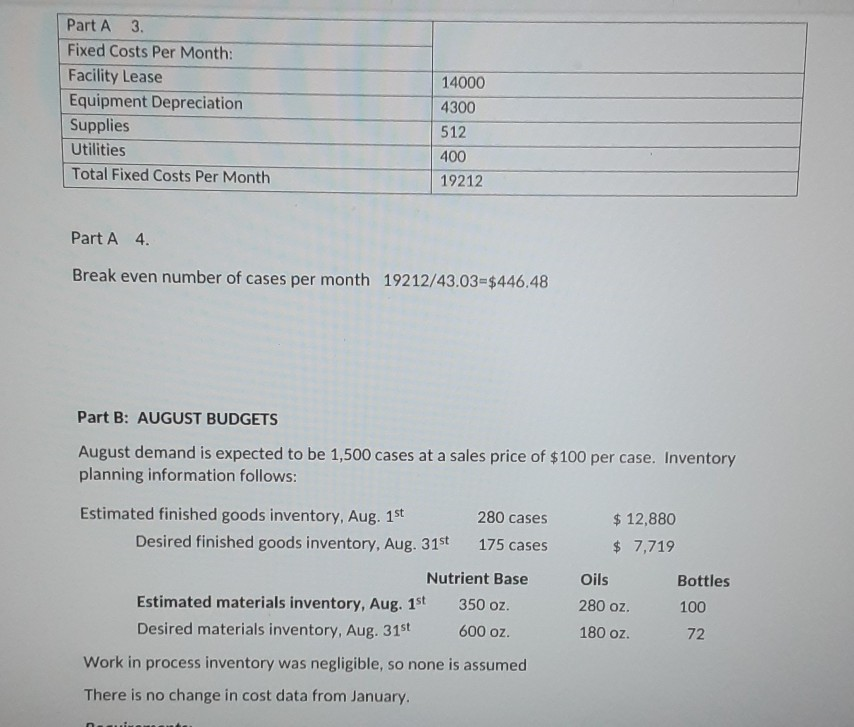

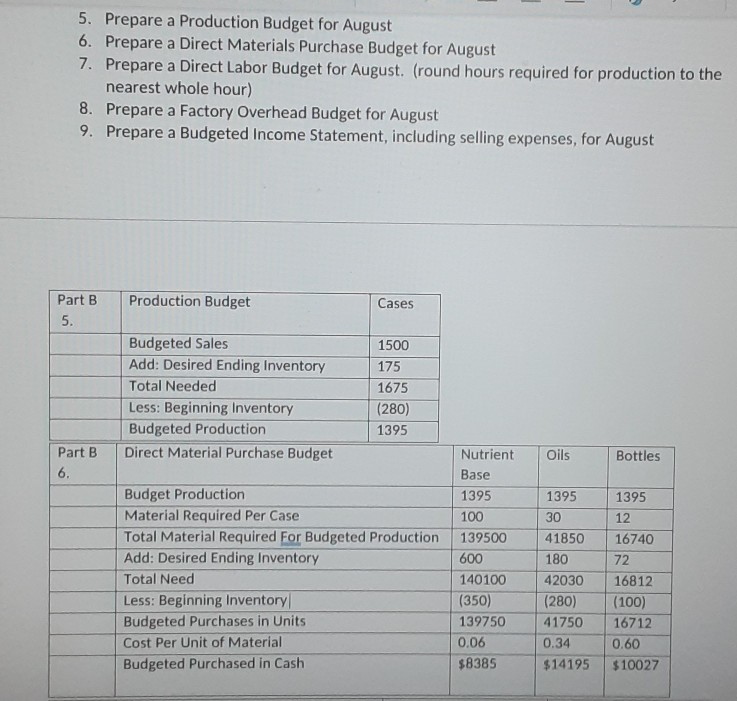

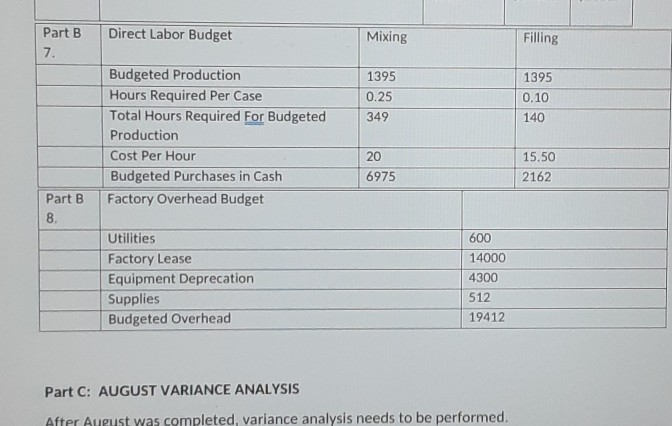

Better By the Numbers began operations on January 1, 2018. The company produces eight- punce bottles of hand and body lotion called Radiant One. The lotion is sold wholesale in 12- bottle cases for $95 per case. There is a selling commission of $20 per case. January 2018 direct materials, direct labor and factory overhead costs are as follows: DIRECT MATERIALS Cost Behavior Units per Case Cost per unit Nutrient base Essential oils Bottle (8-oz.) variable variable variable 100 oz. 30 oz. 12 bottles $ 0.06 $0.34 $ 0.60 Direct Materials Cost per Case $6.00 12.00 7.20 $ 25.20 DIRECT LABOR Department Cost Behavior Time per Case Labor Rate per Hour $ 20.00 $ 15.50 Mixing Filling variable variable 15 min. 6 min. 21 min. Direct Labor Cost per Case $ 5.00 1.55 $ 6.55 FACTORY OVERHEAD Utilities Facility lease Equipment depreciation Supplies Cost Behavior mixed fixed fixed fixed Total Cost $ 600 14,000 4,300 512 $ 19,412 PART A: BREAK-EVEN ANALYSIS The management of Better by the Numbers would like to determine the number of cases required to break-even per month. Utilities cost, a part of factory overhead, is a mixed cost. Following is information gathered for the first six months of operations regarding total utilities costs: 2018 Case Production Utility Total Cost January 500 $ 510 February 800 585 March 1,200 664 April 1,100 640 May 950 599 June 1,025 635 Requirements: 1. Determine the fixed and variable portion of the utility cost using the high-low method. 2. Determine the contribution margin per case 3. Determine the fixed costs per month, including the utility fixed cost from part (1). 4. Determine the break-even number of cases per month | 154 Part A 1. High Activity Level Low Activity Level Change Variable Cost Per Case Fixed Cost at High Level Fixed Cost at Low Level Part A 2. Sales Price Less: Variable Cost Direct Material Direct Labor Utilities Selling Commission Total Variable Cost Contribution Margin Case Production Utility Total Cost 1200 664 500 510 700 0.22 400 400 Per Case $95.00 25.20 6.55 0.22 20.00 51.97 43.03 Part A 3. Fixed Costs Per Month: Part A 3. Fixed Costs Per Month: Facility Lease Equipment Depreciation Supplies Utilities Total Fixed Costs Per Month 14000 4300 512 400 19212 Part A 4. Break even number of cases per month 19212/43.03-$446.48 Part B: AUGUST BUDGETS August demand is expected to be 1,500 cases at a sales price of $100 per case. Inventory planning information follows: Estimated finished goods inventory, Aug. 1st 280 cases Desired finished goods inventory, Aug. 31st 175 cases Nutrient Base Estimated materials inventory, Aug. 1st 350 oz. Desired materials inventory, Aug. 31st 600 oz. $ 12,880 $ 7,719 Oils Bottles 280 oz. 100 180 oz. 72 Work in process inventory was negligible, so none is assumed There is no change in cost data from January 5. Prepare a Production Budget for August 6. Prepare a Direct Materials Purchase Budget for August 7. Prepare a Direct Labor Budget for August. (round hours required for production to the nearest whole hour) 8. Prepare a Factory Overhead Budget for August 9. Prepare a Budgeted Income Statement, including selling expenses, for August Part B Production Budget Cases Budgeted Sales Add: Desired Ending Inventory Total Needed Less: Beginning Inventory Budgeted Production Direct Material Purchase Budget 1500 175 1675 (280) 1395 Part B Oils Bottles 1395 30 1395 12 16740 Nutrient Base 1395 100 139500 600 140100 (350) 139750 0.06 $8385 Budget Production Material Required Per Case Total Material Required for Budgeted Production Add: Desired Ending Inventory Total Need Less: Beginning Inventory Budgeted Purchases in Units Cost Per Unit of Material Budgeted Purchased in Cash 172 41850 180 42030 (280) 41750 0.34 $14195 16812 (100) 16712 0.60 $10027 Part B Direct Labor Budget Mixing Filling 1395 0.25 349 1395 0.10 140 Budgeted Production Hours Required Per Case Total Hours Required For Budgeted Production Cost Per Hour Budgeted Purchases in Cash Factory Overhead Budget 20 15.50 2162 6975 Utilities Factory Lease Equipment Deprecation Supplies Budgeted Overhead 600 14000 4300 512 19412 Part C: AUGUST VARIANCE ANALYSIS After August was completed, variance analysis needs to be performed

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts