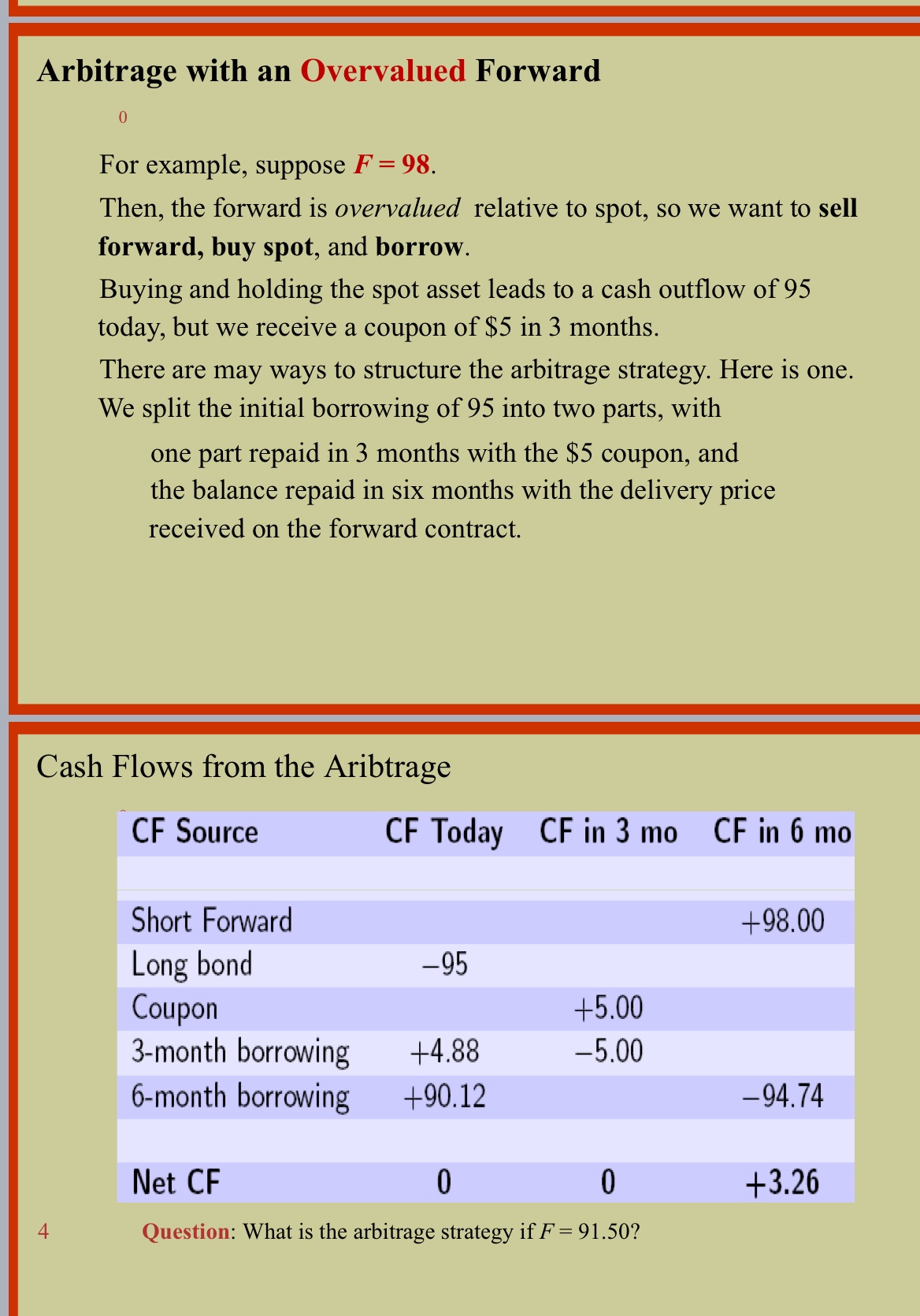

Question: The question down also when you answer write table Arbitrage with an Overvalued Forward 0 For example, suppose F = 98. Then, the forward is

The question down also when you answer write table

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock