Question: The question instruction is in the picture, it doesn't allow me to type the full question in box. Let 5 = $300, K = $300,

The question instruction is in the picture, it doesn't allow me to type the full question in box.

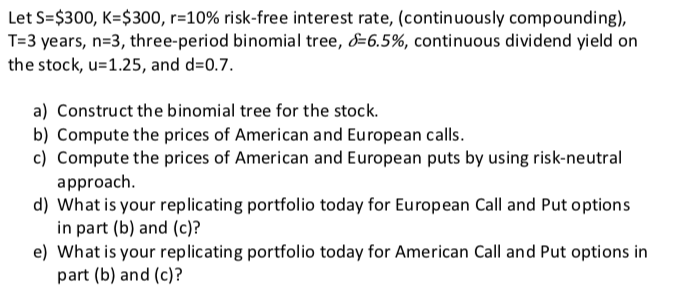

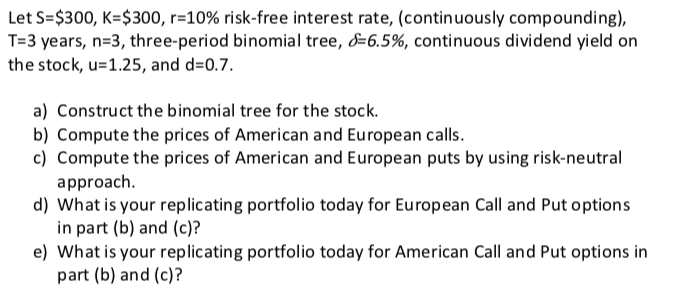

Let 5 = $300, K = $300, 1= 10% risk - free interest rate , ( continuously compounding ) , T = 3 years , n = 3, three - period binomial tree , ${_ 6.5%6 , continuous dividend yield on the stock , 4 = 1. 25, and d = 0. 7 . a ) Construct the binomial tree for the stock . b ) Compute the prices of American and European calls . c ) Compute the prices of American and European puts by using risk - neutral approach . d ) What is your replicating portfolio today for European Call and Put options in part ( b ) and ( C ) ?" e ) What is your replicating portfolio today for American Call and Put options in part ( b ) and ( c )

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts