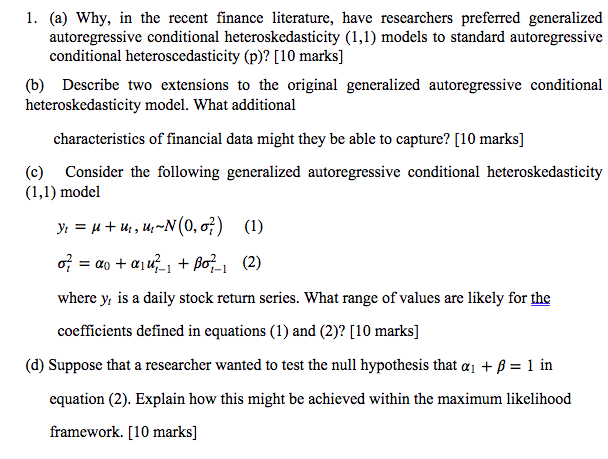

Question: The question is attached as below: 1. (a) Why, in the recent finance literature, have researchers preferred generalized autoregressive conditional heteroskedasticity (1,1) models to standard

The question is attached as below:

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock