Question: The question is complete. Use the following data for a fictitiously named company OPPS to answer the questions that follow: The current stock price S

The question is complete.

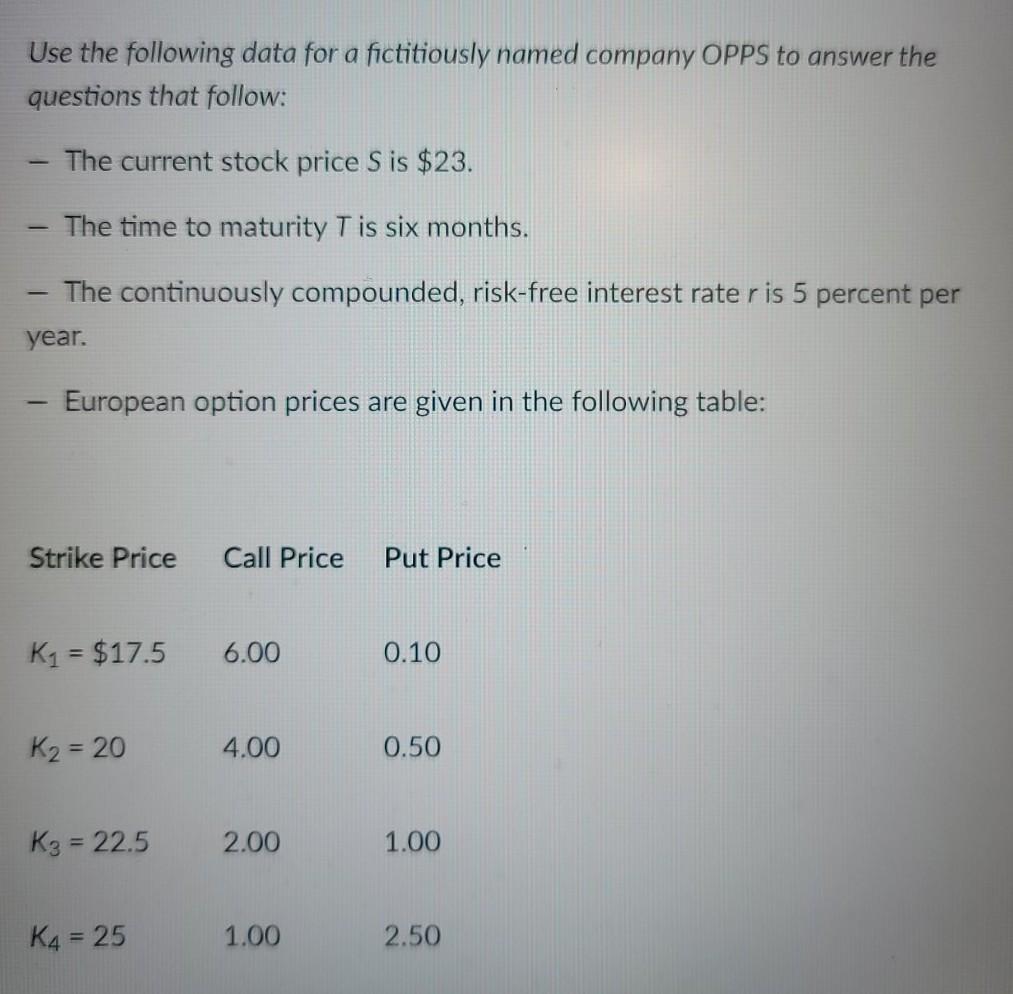

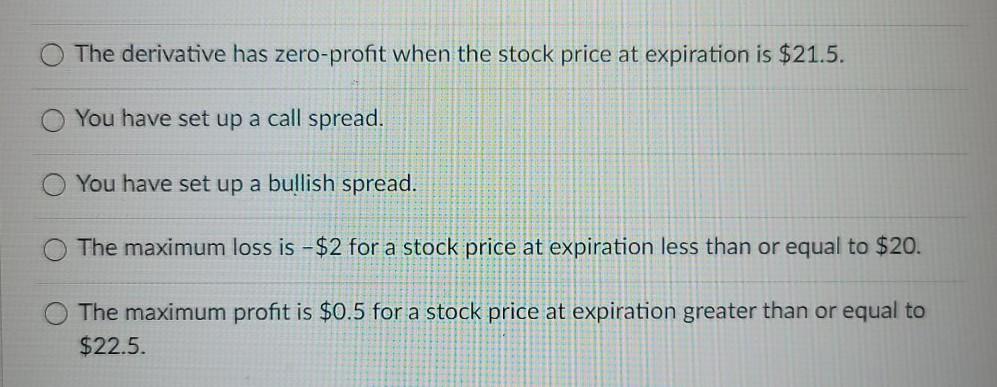

Use the following data for a fictitiously named company OPPS to answer the questions that follow: The current stock price S is $23. The time to maturity T is six months. The continuously compounded, risk-free interest rate ris 5 percent per year. European option prices are given in the following table: Strike Price Call Price Put Price K1 = $17.5 6.00 0.10 K2 = 20 4.00 0.50 K3 = 22.5 2.00 1.00 K4 = 25 1.00 2.50 The derivative has zero-profit when the stock price at expiration is $21.5. You have set up a call spread. You have set up a bullish spread. The maximum loss is - $2 for a stock price at expiration less than or equal to $20. The maximum profit is $0.5 for a stock price at expiration greater than or equal to $22.5. Use the following data for a fictitiously named company OPPS to answer the questions that follow: The current stock price S is $23. The time to maturity T is six months. The continuously compounded, risk-free interest rate ris 5 percent per year. European option prices are given in the following table: Strike Price Call Price Put Price K1 = $17.5 6.00 0.10 K2 = 20 4.00 0.50 K3 = 22.5 2.00 1.00 K4 = 25 1.00 2.50 The derivative has zero-profit when the stock price at expiration is $21.5. You have set up a call spread. You have set up a bullish spread. The maximum loss is - $2 for a stock price at expiration less than or equal to $20. The maximum profit is $0.5 for a stock price at expiration greater than or equal to $22.5

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts