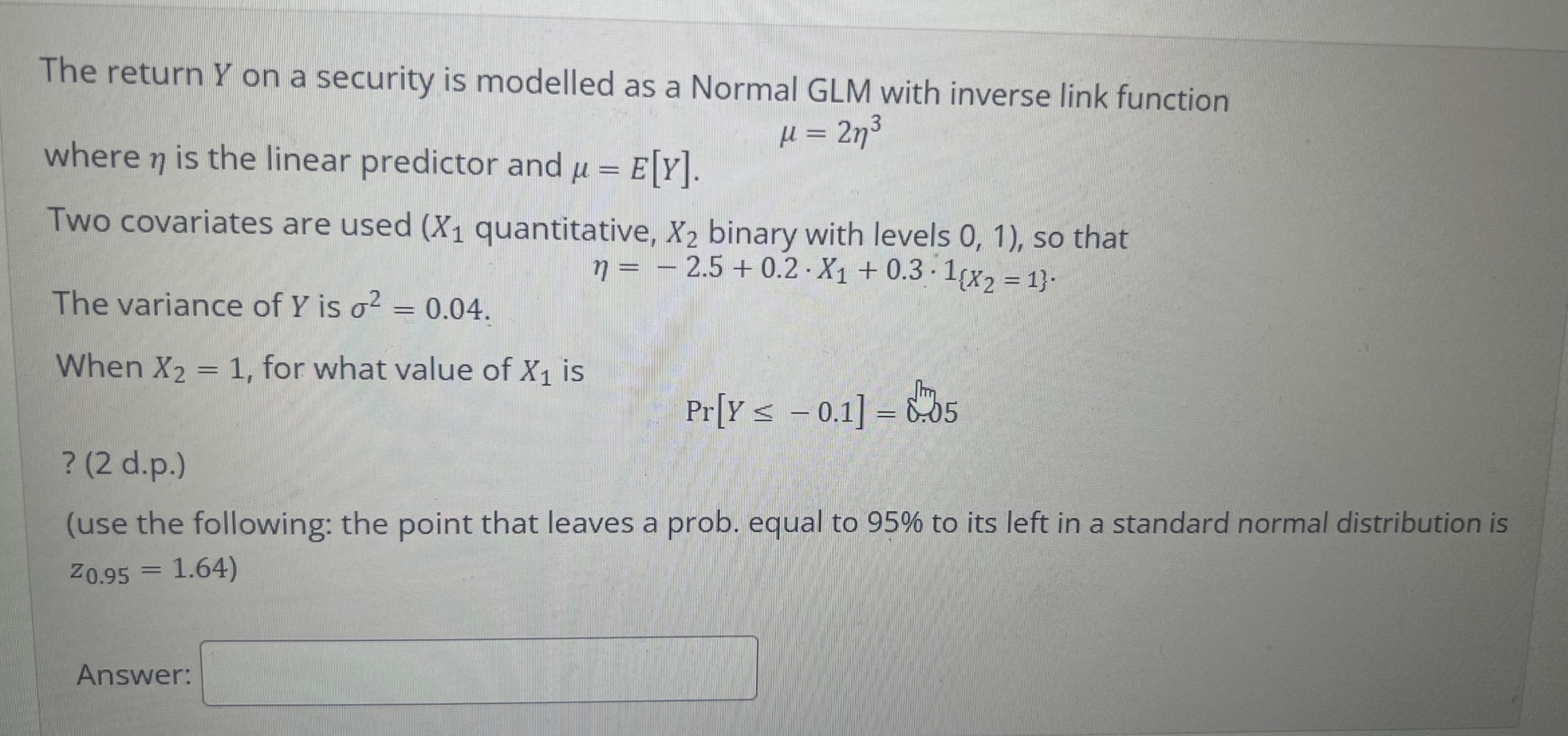

Question: The return Y on a security is modelled as a Normal GLM with inverse link function H = 2n3 where n is the linear predictor

The return Y on a security is modelled as a Normal GLM with inverse link function H = 2n3 where n is the linear predictor and u = E[Y]. Two covariates are used (X1 quantitative, X2 binary with levels 0, 1), so that n = - 2.5 + 0.2 . X1 + 0.3 - 1{x2 = 1} The variance of Y is o2 = 0.04. When X2 = 1, for what value of X1 is Pr[Y S - 0.1] = 8:05 ? (2 d.p.) (use the following: the point that leaves a prob. equal to 95% to its left in a standard normal distribution is Z0.95 = 1.64)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock