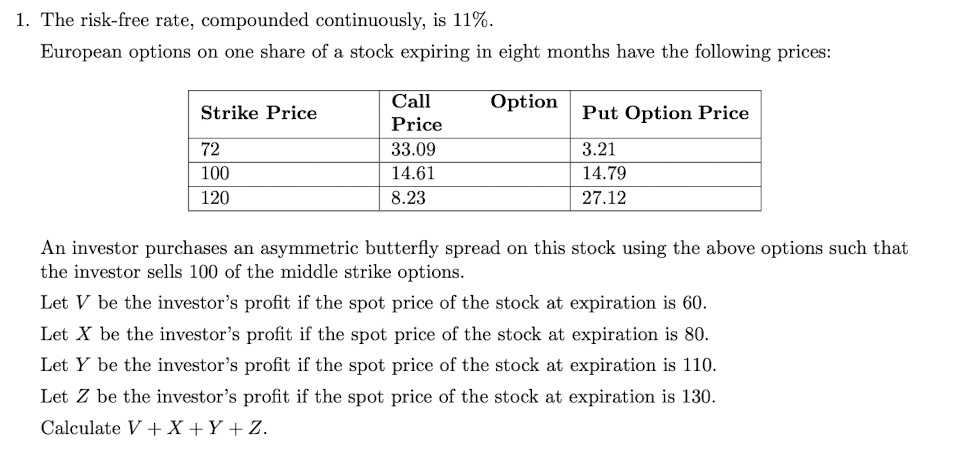

Question: The risk - free rate, compounded continuously, is 1 1 % . European options on one share of a stock expiring in eight months have

The riskfree rate, compounded continuously, is

European options on one share of a stock expiring in eight months have the following prices:

An investor purchases an asymmetric butterfly spread on this stock using the above options such that

the investor sells of the middle strike options.

Let be the investor's profit if the spot price of the stock at expiration is

Let be the investor's profit if the spot price of the stock at expiration is

Let be the investor's profit if the spot price of the stock at expiration is

Let be the investor's profit if the spot price of the stock at expiration is

Calculate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock