Question: The risk-free interest rate is the same as the data in Problem 4.5. What is the value of the FRA that begins after a year

The risk-free interest rate is the same as the data in Problem 4.5. What is the value of the FRA that begins after a year when it pays LIBOR for three months on a principal of 1,000,000 months of holders and receives a 4.5% (quarterly compounded) interest rate? The forward LIBOR interest rate for three months is 5% (quarter compounded).

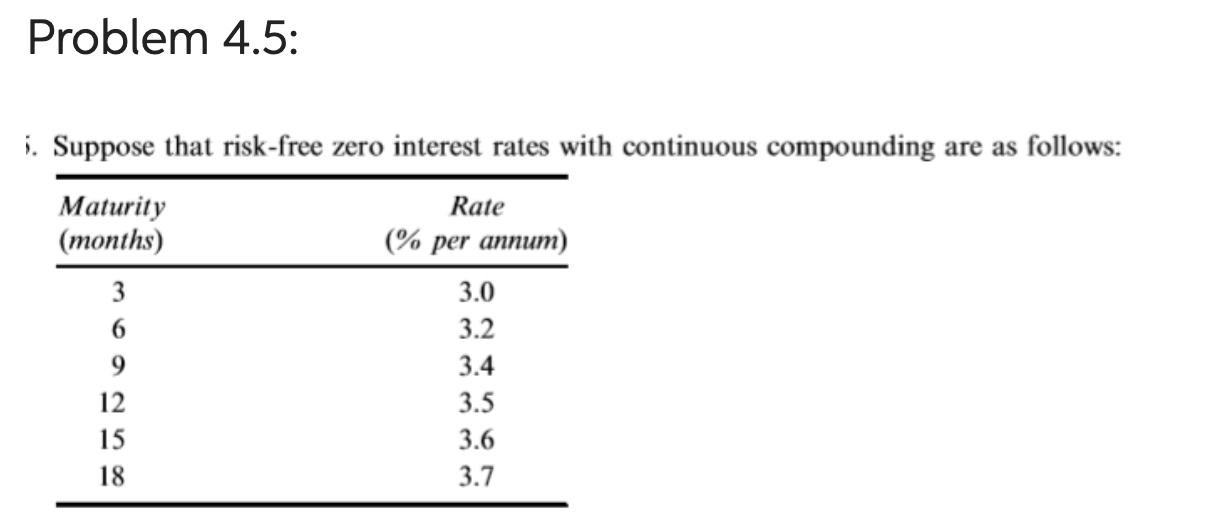

Problem 4.5: i. Suppose that risk-free zero interest rates with continuous compounding are as follows: Maturity (months) 3 6 9 12 15 18 Rate (% per annum) 3.0 3.2 3.4 3.5 3.6 3.7

Step by Step Solution

3.36 Rating (152 Votes )

There are 3 Steps involved in it

To calculate the value of the FRA we need to find the present value of the difference between the ... View full answer

Get step-by-step solutions from verified subject matter experts