Question: The risk-free rate is currently 7.9 %. Use the data in the accompanying table for the Fio family's portfolio and the market portfolio during the

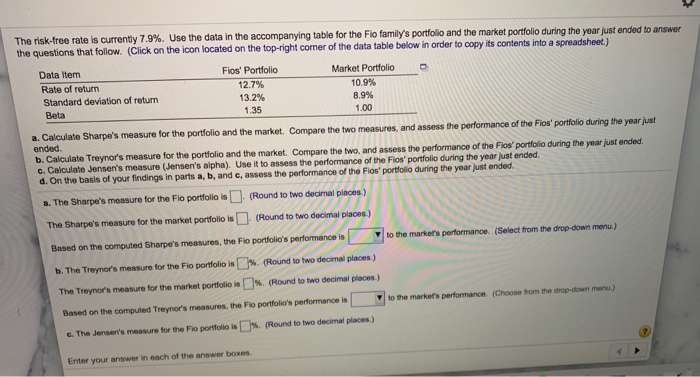

The risk-free rate is currently 7.9 %. Use the data in the accompanying table for the Fio family's portfolio and the market portfolio during the year just ended to answer the questions that follow. (Click on the icon located on the top-right comer of the data table below in order to copy its contents into a spreadsheet.) Data Item Fios' Portfolio Market Portfolio Rate of return Standard deviation of return 12.7% 10.9% 8.9 % 13.2% Beta 1.35 1.00 a. Calculate Sharpe's measure for the portfolio and the market. Compare the two measures, and assess the performance of the Fios' portfolio during the year just ended. b. Calculate Treynor's measure for the portfolio and the market. Compare the two, and assess the performance of the Fios' portfolio during the year just ended c. Calculate Jensen's measure (Jensen's alpha). Use it to assess the performance of the Fios' portfolio during the year just ended d. On the basis of your findings in parts a, b, and c, assess the performance of the Fios' portfolio during the year just ended (Round to two decimal places.) a. The Sharpe's measure for the Fio portfolio is (Round to two decimal places.) The Sharpe's measure for the market portfolio is (Select from the drop-down menu.) to the market's performance. Based on the computed Sharpe's measures, the Fio portfolio's performance is %. (Round to two decimal places.) b. The Treynor's measure for the Fio portfolio is The Treynor's measure for the market portfolio is %. ( Round to two decimal places.) to the markers performance. (Choose from the drop-down menu.) Based on the computed Treynor's measures, the Fio portfolio's performance is %. (Round to two decimal places.) c. The Jensen's measure for the Fio portfolio is Enter your answer in each of the answer boxes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts