Question: The selected answer (D) is NOT CORRECT, plz help. The selected answer (B) is NOT CORRECT, plz help. The selected answer (B) is NOT CORRECT,

The selected answer (D) is NOT CORRECT, plz help.

The selected answer (B) is NOT CORRECT, plz help.

The selected answer (B) is NOT CORRECT, plz help.

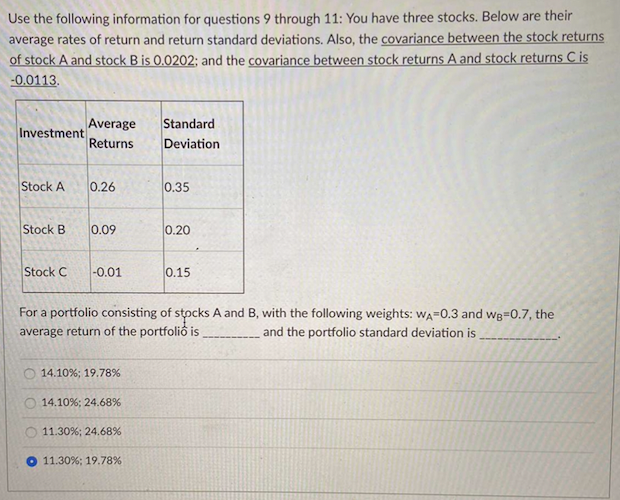

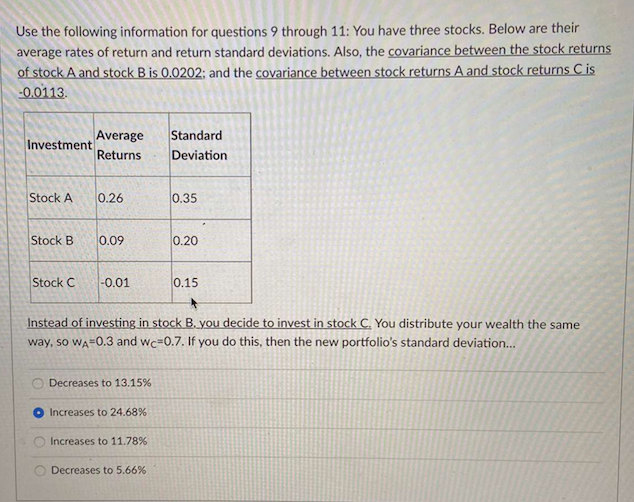

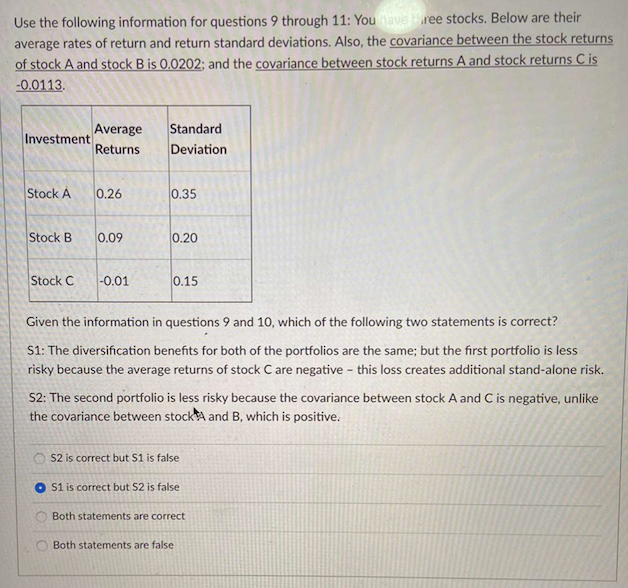

Use the following information for questions 9 through 11: You have three stocks. Below are their average rates of return and return standard deviations. Also, the covariance between the stock returns of stock A and stock Bis 0.0202; and the covariance between stock returns A and stock returns C is -0.0113 Average Investment Returns Standard Deviation Stock A 0.26 0.35 Stock B 0.09 0.20 Stock C -0.01 0.15 For a portfolio consisting of stocks A and B, with the following weights: Wa=0.3 and we=0.7, the average return of the portfolio is and the portfolio standard deviation is 14.10%; 19.78% 14.10%; 24.68% 11.30%; 24.68% o 11.30%: 19.78% Use the following information for questions 9 through 11: You have three stocks. Below are their average rates of return and return standard deviations. Also, the covariance between the stock returns of stock A and stock B is 0.0202; and the covariance between stock returns A and stock returns C is -0.0113 Average Investment Returns Standard Deviation Stock A 0.26 0.35 Stock B 0.09 0.20 Stock C -0.01 0.15 Instead of investing in stock B, you decide to invest in stock C. You distribute your wealth the same way, so Wa=0.3 and wc=0.7. If you do this, then the new portfolio's standard deviation... Decreases to 13.15% Increases to 24.68% Increases to 11.78% Decreases to 5.66% Use the following information for questions 9 through 11: You averee stocks. Below are their average rates of return and return standard deviations. Also, the covariance between the stock returns of stock A and stock Bis 0.0202; and the covariance between stock returns A and stock returns C is -0.0113. Average Investment Returns Standard Deviation Stock A 0.26 0.35 Stock B 0.09 0.20 Stock C -0.01 0.15 Given the information in questions 9 and 10, which of the following two statements is correct? S1: The diversification benefits for both of the portfolios are the same; but the first portfolio is less risky because the average returns of stock C are negative - this loss creates additional stand-alone risk. S2: The second portfolio is less risky because the covariance between stock A and C is negative, unlike the covariance between stock!A and B, which is positive. S2 is correct but S1 is false S1 is correct but S2 is false Both statements are correct Both statements are false

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts