Question: The table above contains the return and standard deviation for Portfolio P and the benchmark Market portfolio. Assuming a risk-free rate of 1.7%, and that

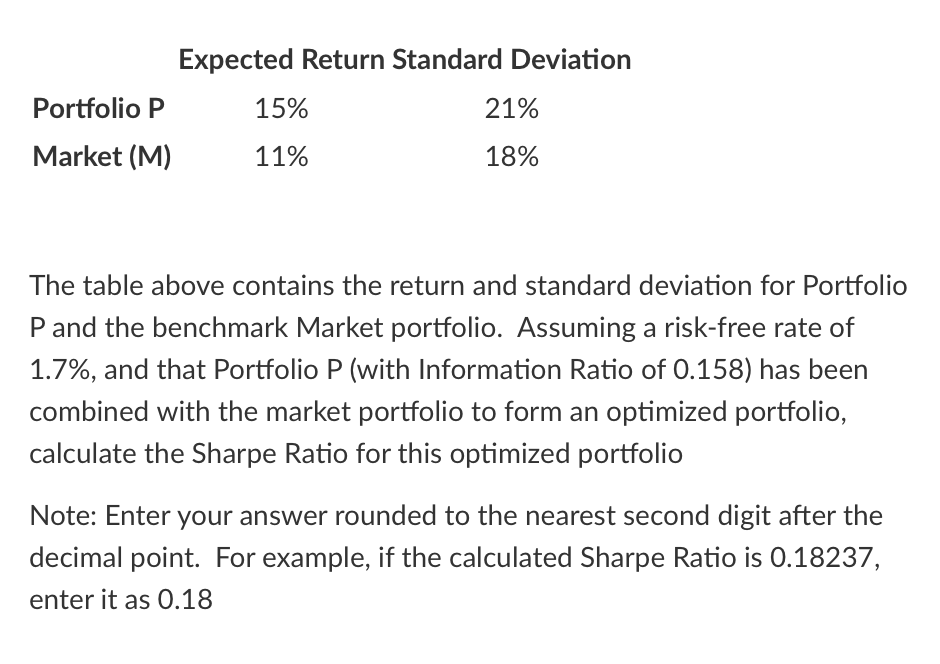

The table above contains the return and standard deviation for Portfolio P and the benchmark Market portfolio. Assuming a risk-free rate of 1.7%, and that Portfolio P (with Information Ratio of 0.158 ) has been combined with the market portfolio to form an optimized portfolio, calculate the Sharpe Ratio for this optimized portfolio Note: Enter your answer rounded to the nearest second digit after the decimal point. For example, if the calculated Sharpe Ratio is 0.18237 , enter it as 0.18

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock