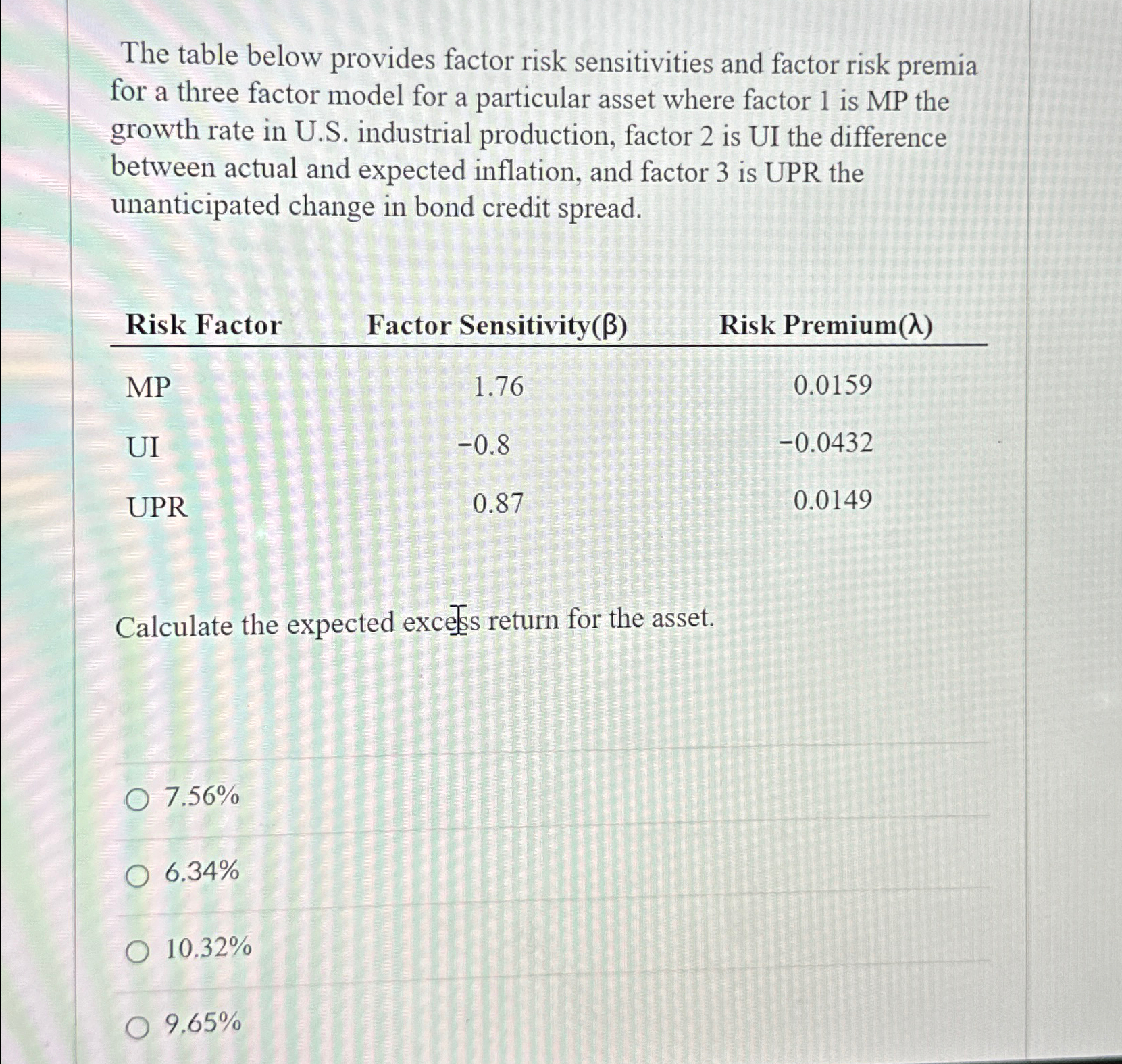

Question: The table below provides factor risk sensitivities and factor risk premia for a three factor model for a particular asset where factor 1 is MP

The table below provides factor risk sensitivities and factor risk premia for a three factor model for a particular asset where factor is MP the growth rate in US industrial production, factor is UI the difference between actual and expected inflation, and factor is UPR the unanticipated change in bond credit spread.

tableRisk Factor,Factor Sensitivity Risk Premium

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock