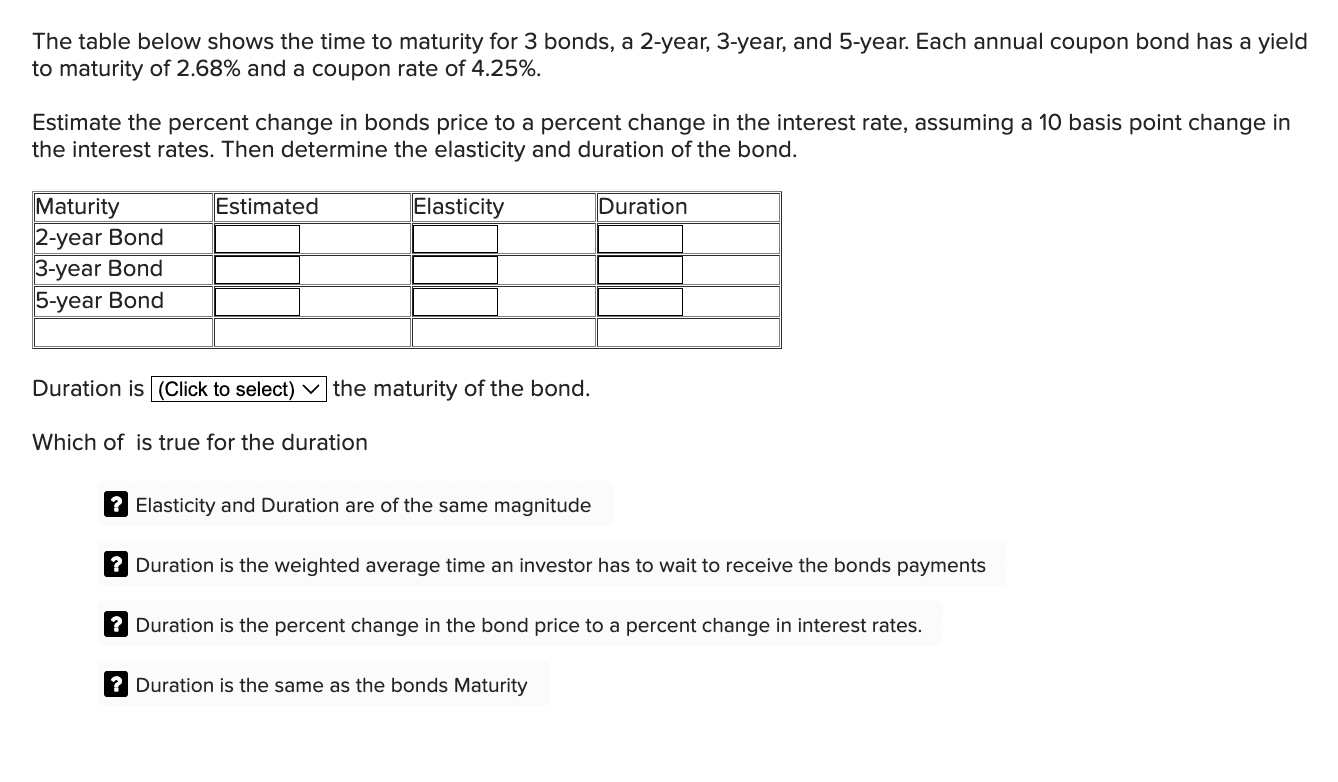

Question: The table below shows the time to maturity for 3 bonds, a 2 - year, 3 - year, and 5 - year. Each annual coupon

The table below shows the time to maturity for bonds, a year, year, and year. Each annual coupon bond has a yield to maturity of and a coupon rate of

Estimate the percent change in bonds price to a percent change in the interest rate, assuming a basis point change in the interest rates. Then determine the elasticity and duration of the bond.

Duration is Click to select v the maturity of the bond.

Which of is true for the duration

Elasticity and Duration are of the same magnitude

Duration is the weighted average time an investor has to wait to receive the bonds payments

Duration is the percent change in the bond price to a percent change in interest rates.

Duration is the same as the bonds Maturity

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock