Question: the table on exhibit 5-3 is also provided Fundamental Assignment Material 5-A1 Special Order Consider the following details of the income statement of the Manteray

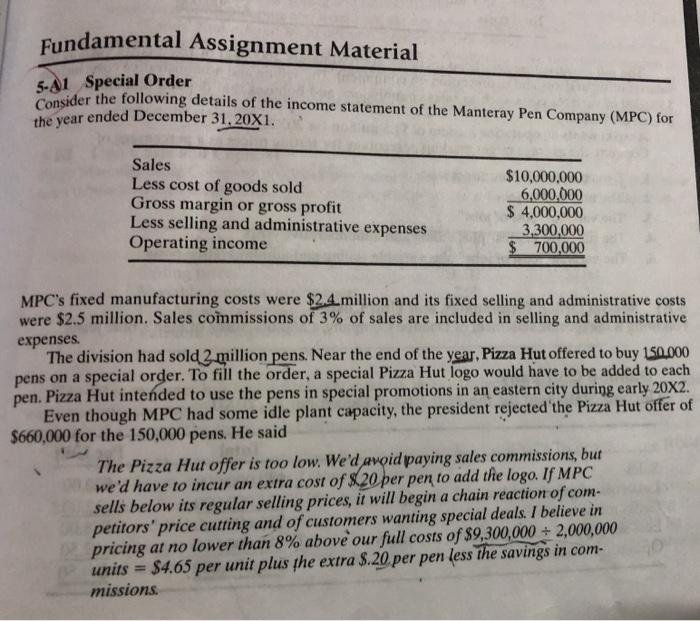

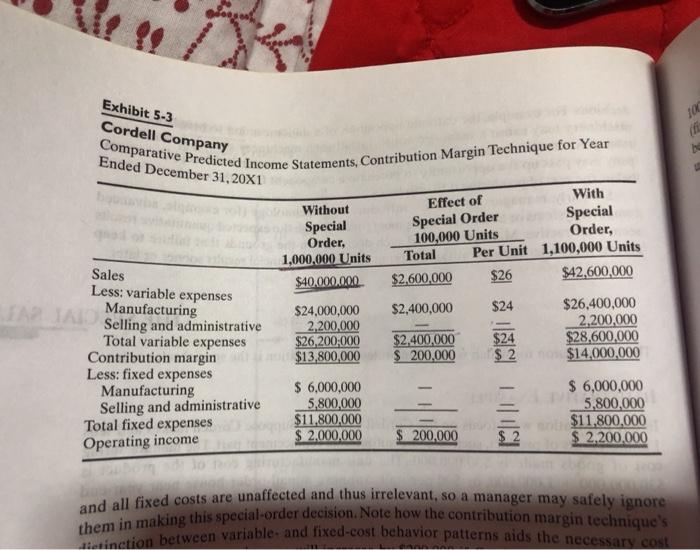

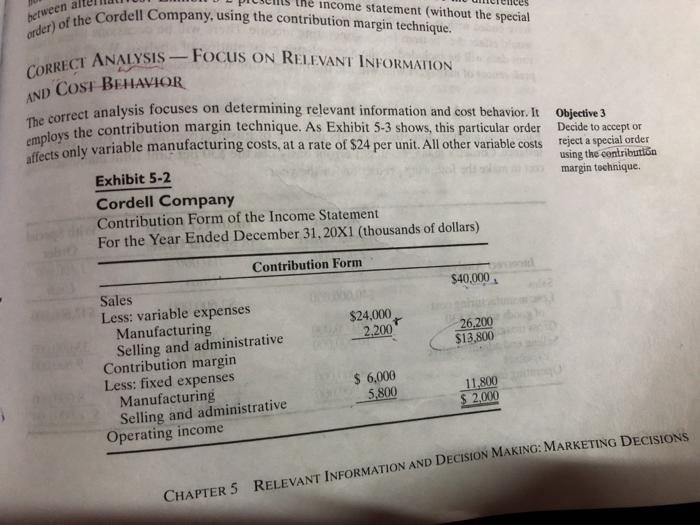

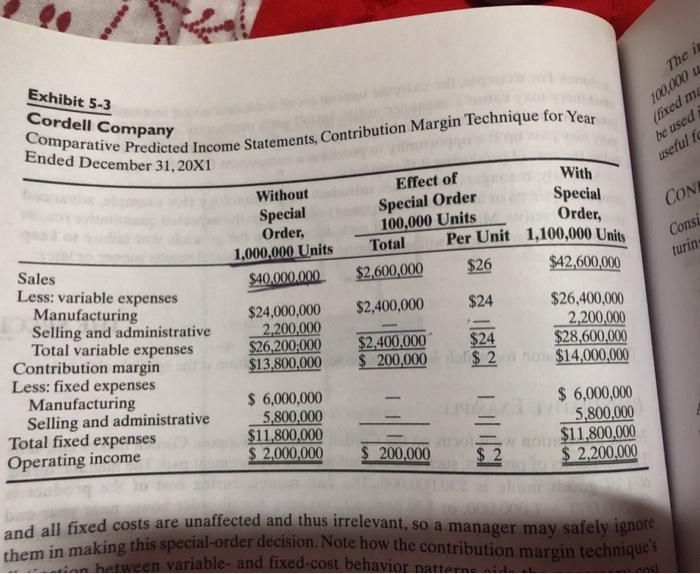

Fundamental Assignment Material 5-A1 Special Order Consider the following details of the income statement of the Manteray Pen Company (MPC) for the year ended December 31, 20X1. Sales Less cost of goods sold Gross margin or gross profit Less selling and administrative expenses Operating income $10,000,000 6,000,000 $ 4,000,000 3,300,000 $ 700,000 MPC's fixed manufacturing costs were $2.4 million and its fixed selling and administrative costs were $2.5 million. Sales commissions of 3% of sales are included in selling and administrative expenses The division had sold 2 million pens. Near the end of the year, Pizza Hut offered to buy 150.000 pens on a special order. To fill the order, a special Pizza Hut logo would have to be added to each pen. Pizza Hut intended to use the pens in special promotions in an eastern city during early 20X2. Even though MPC had some idle plant capacity, the president rejected the Pizza Hut offer of $660,000 for the 150,000 pens. He said The Pizza Hut offer is too low. We'd avoid paying sales commissions, but we'd have to incur an extra cost of $20 per pen to add the logo. If MPC sells below its regular selling prices, it will begin a chain reaction of com- petitors' price cutting and of customers wanting special deals. I believe in pricing at no lower than 8% above our full costs of $9,300,000 + 2,000,000 units $4.65 per unit plus he extra $.20 per pen less the savings in com- missions Required 1. Using the contribution margin technique, prepare an analysis similar to that in Exhibit 5.3. page 186. Use four columns without the special order, the effect of the special order (total and per unit), and totals with the special order. By what percentage would operating income increase or decrease if the order had been accepted? Do you agree with the president's decision? Why? 2. Comparative Predicted Income Statements, Contribution Margin Technique for Year Exhibit 5-3 Cordell Company 100 Ended December 31, 20X1 0 Without Special Order, 1,000,000 Units $40.000.000 Effect of With Special Order Special 100,000 Units Order, Total Per Unit 1,100,000 Units $2,600,000 $26 $42,600,000 $2,400,000 $24 Sales Less: variable expenses Manufacturing Selling and administrative Total variable expenses Contribution margin Less: fixed expenses Manufacturing $24,000,000 2,200,000 $26,200,000 $13,800,000 $26,400,000 2.200,000 $28,600,000 $14,000,000 $24 $2,400,000 $ 200,000 Selling and administrative Total fixed expenses Operating income $ 6,000,000 5,800,000 $11.800.000 $ 2.000.000 $ 6,000,000 5,800,000 $11,800,000 $ 2.200.000 $ 200,000 $ 2 and all fixed costs are unaffected and thus irrelevant, so a manager may safely ignore them in making this special orden decisione e showithe contribution margin technique's The tinction between variable and fixed-cost behavior patterns aids the necessary cost he income statement (without the special between al AND order) of the Cordell Company, using the contribution margin technique. CORRECT ANALYSIS FOCUS ON RELEVANT INFORMATION employs the contribution margin technique. As Exhibit 5-3 shows, this particular order Decide to accept or COST BEHAVIOR affects only variable manufacturing costs, at a rate of $24 per unit. All other variable costs reject a special order Exhibit 5-2 margin technique Cordell Company Contribution Form of the Income Statement For the Year Ended December 31, 20X1 (thousands of dollars) $40.000 26,200 $13,800 Contribution Form Sales Less: variable expenses Manufacturing $24,000 Selling and administrative 2,200 Contribution margin Less: fixed expenses Manufacturing $ 6,000 5,800 Selling and administrative Operating income 11.800 $ 2,000 CHAPTER 5 RELEVANT INFORMATION AND DECISION MAKING: MARKETING DECISIONS Comparative Predicted Income Statements, Contribution Margin Technique for Year Exhibit 5-3 Cordell Company The 100,000 44 (fixed me be used useful to Ended December 31, 20X1 With Special Order, Effect of Special Order 100,000 Units Total Without Special Order, 1.000.000 Units $40,000,000 CON Consi Per Unit 1,100,000 Units $26 $42,600,000 turin $2,600,000 Sales Less: variable expenses Manufacturing Selling and administrative Total variable expenses Contribution margin Less: fixed expenses Manufacturing Selling and administrative Total fixed expenses $24,000,000 2,200,000 $26,200.000 $13.800,000 $2,400,000 $24 $26,400,000 2,200,000 $2,400,000 $24 $28,600,000 $ 200,000 $ 20 $14,000,000 $ 6,000,000 5,800,000 $11,800,000 $ 2,000,000 $ 6,000,000 5,800,000 $11,800,000 $ 2.200.000 $ 200,000 $ 2 Operating income and all fixed costs are unaffected and thus irrelevant, so a manager may safely ignore them in making this special-order decision. Note how the contribution margin technique's in hetween variable and fixed-cost behavior natt

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts