Question: There are some formula right here. If you need it, please use it. Morrison Medical Inc., an all-equity firm, has earnings before interest and taxes

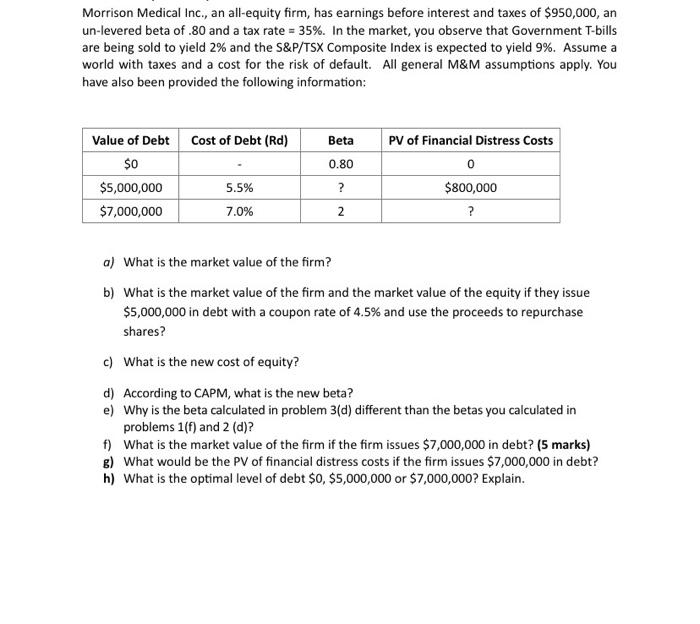

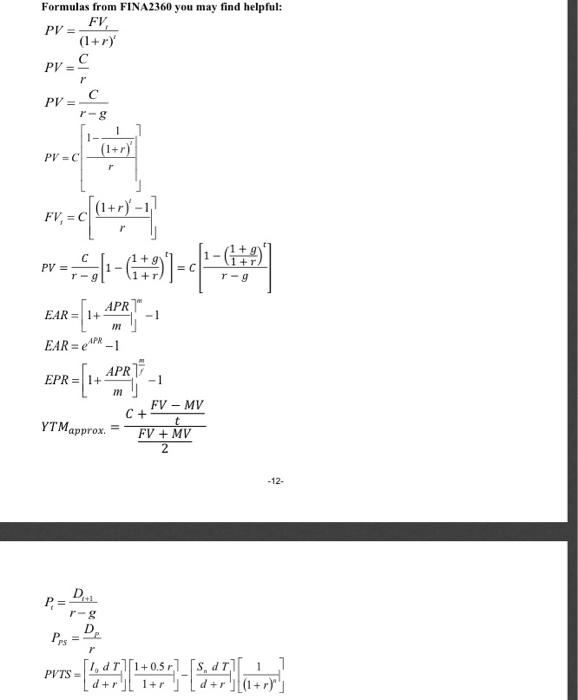

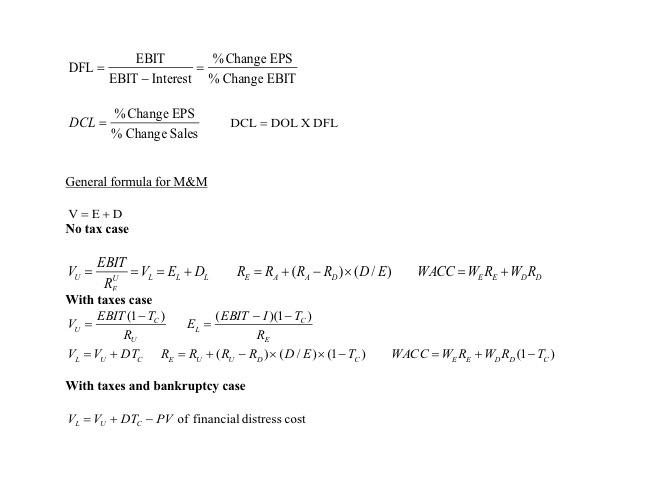

Morrison Medical Inc., an all-equity firm, has earnings before interest and taxes of $950,000, an un-levered beta of.80 and a tax rate = 35%. In the market, you observe that Government T-bills are being sold to yield 2% and the S&P/TSX Composite Index is expected to yield 9%. Assume a world with taxes and a cost for the risk of default. All general M&M assumptions apply. You have also been provided the following information: Beta 0.80 Value of Debt Cost of Debt (Rd) $0 $5,000,000 5.5% $7,000,000 7.0% PV of Financial Distress Costs 0 $800,000 ? ? 2 a) What is the market value of the firm? b) What is the market value of the firm and the market value of the equity if they issue $5,000,000 in debt with a coupon rate of 4.5% and use the proceeds to repurchase shares? c) What is the new cost of equity? d) According to CAPM, what is the new beta? e) Why is the beta calculated in problem 3(d) different than the betas you calculated in problems 1(f) and 2 (d)? f) What is the market value of the firm if the firm issues $7,000,000 in debt? (5 marks) g) What would be the PV of financial distress costs if the firm issues $7,000,000 in debt? h) What is the optimal level of debt $0, $5,000,000 or $7,000,000? Explain. Formulas from FINA2360 you may find helpful: FV. PV = = (1+r) C PV =- -S 1 1 - PV = FV, NC (+) C T-9 r-9 w- |--491-4 EAR R=[" APR EAR=1+ m EAR = APR-1 APR 17 EPR= 1+ m FV - MV C + t YTMapprox. FV + MV 2 -12- DA P = -& D Pros 1,011+0.5 r1 [S, dT] 1 PVTS De P = D. Pps 1 ] PVTS d111+0. d+r) 1+r Chapter 12: Var (R)=(1/(T-1){(2, -R) +...+(2,- R$*] Geometric average retum-((1+R)(1+R, )* .*(1+R) - 1 Chapter 13: E(R) -,

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts