Question: There is a task to find AC(1), explain non-stationaity, test integration, explain trend stationar, derive the mean, find order of integration. Deatils are the following:

There is a task to find AC(1), explain non-stationaity, test integration, explain trend stationar, derive the mean, find order of integration. Deatils are the following:

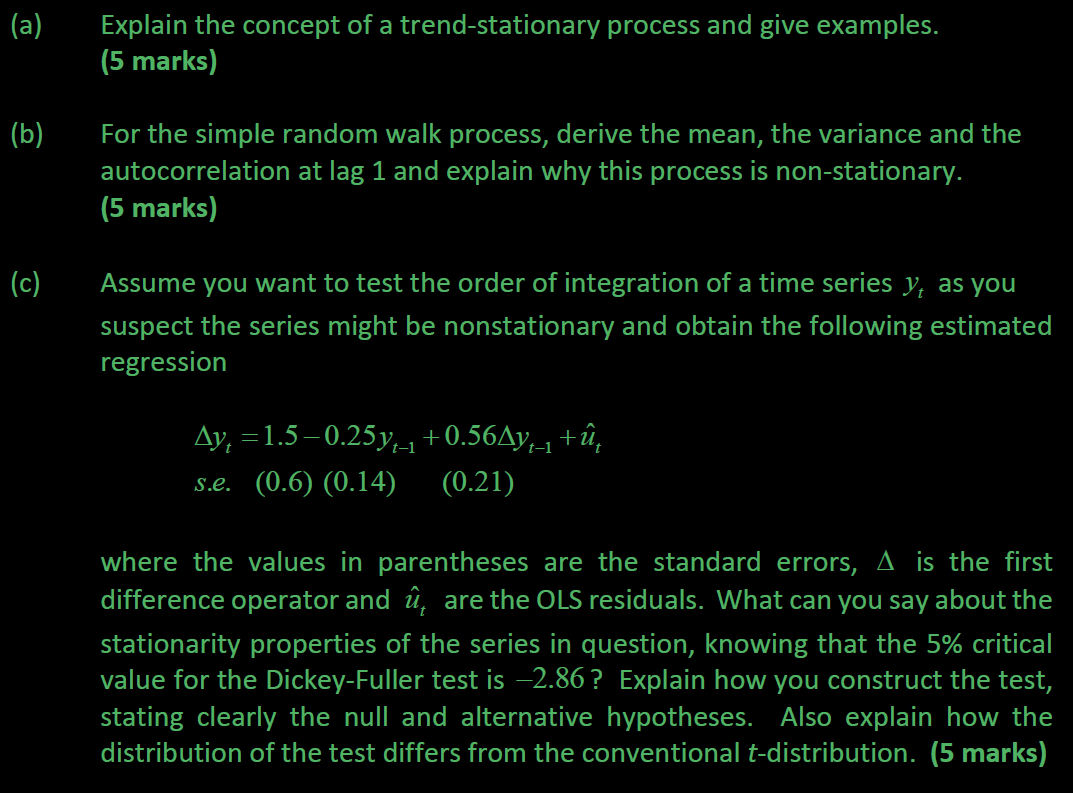

(a) Explain the concept of a trend-stationary process and give examples. (5 marks) (b) For the simple random walk process, derive the mean, the variance and the autocorrelation at lag 1 and explain why this process is non-stationary. (5 marks) (c) Assume you want to test the order of integration of a time series y, as you suspect the series might be nonstationary and obtain the following estimated regression Ay, =1.5-0.25y,_1 +0.56Ay,_1 + u, s.e. (0.6) (0.14) (0.21) where the values in parentheses are the standard errors, A is the first difference operator and u, are the OLS residuals. What can you say about the stationarity properties of the series in question, knowing that the 5% critical value for the Dickey-Fuller test is -2.86? Explain how you construct the test, stating clearly the null and alternative hypotheses. Also explain how the distribution of the test differs from the conventional t-distribution. (5 marks)(d) Based on your results in (c), how would you proceed to determine the order of integration of the series y, ? If this step involves another test, explain how you construct the test, stating clearly the null and alternative hypotheses

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts