Question: They leveraged portfolio return is PRACTICE PROBLEM: Ccile Perreaux is a junior analyst for an international wealth management firm. Her supervis, The following information relates

They leveraged portfolio return is

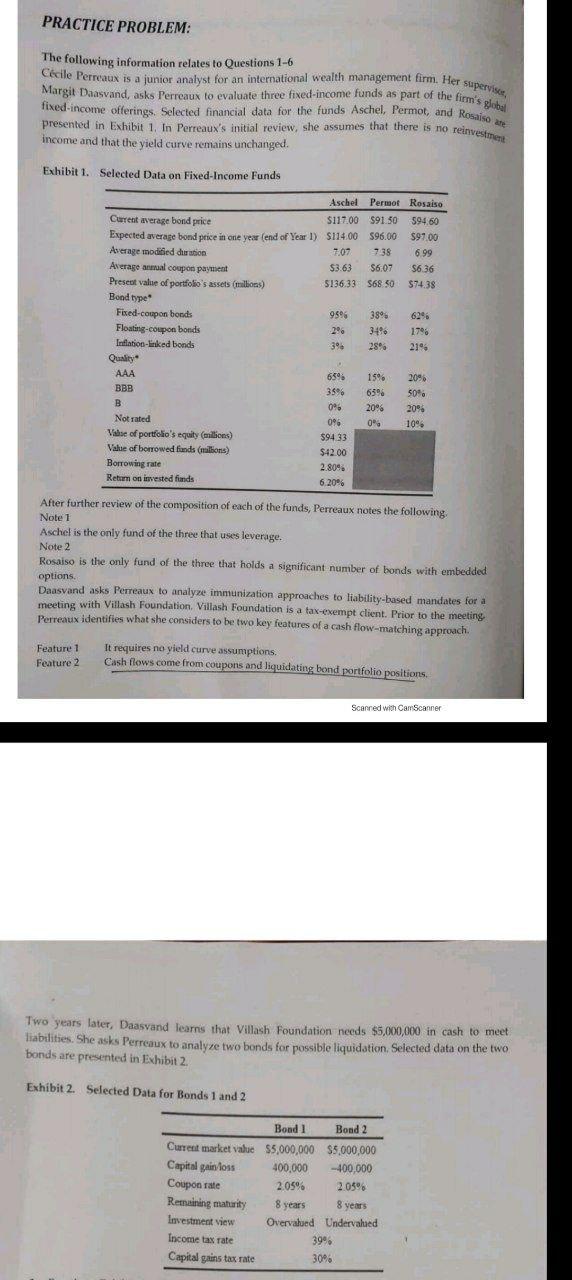

PRACTICE PROBLEM: Ccile Perreaux is a junior analyst for an international wealth management firm. Her supervis, The following information relates to Questions 1-6 Margit Daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds Aschel, Permot, and Rosalso a presented in Exhibit 1. In Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged. Exhibit 1. Selected Data on Fixed-Income Funds Aschel Permof Rosaiso Current average bond price $117.00 $91.50 $94.60 Expected average bond price in one year (end of Year 1) 5114.00 596.00 $97.00 Average modified duration 7.07 738 6.99 Average mal coupon payment $3.63 $6.07 S6.36 Presest value of portfolio's assets (milions) 5136.33 568 50 $74.38 Bond type Fixed-coupon bonds 9596 389 Floating-coupon bonds 29 3490 178 Inflation-linked bonds 396 28% 21% Quality AAA 659 15 20% BBB 356 65% 50% B 0% 20% 20% Not rated 06 0" 10% Vase of portfolio's equity (erillions) $94 33 Value of borrowed funds (millions) $42.00 Borrowing rate 2 809 Return on invested finds 6,20% After further review of the composition of each of the funds, Perreaux notes the following Note 1 Aschel is the only fund of the three that uses leverage. Note 2 Rosaiso is the only fund of the three that holds a significant number of bonds with embedded options, Daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with Villash Foundation. Villash Foundation is a tax-exempt client. Prior to the meeting Perreaux identifies what she considers to be two key features of a cash flow-matching approach. Feature 1 It requires no yield curve assumptions. Feature 2 Cash flows come from coupons and liquidating bond portfolio positions. Scanned with CamScanner Two years later, Daasvand learns that Villash Foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation Selected data on the two bonds are presented in Exhibit 2. Exhibit 2. Selected Data for Bonds 1 and 2 Bond 1 Bond 2 Current market value $5,000,000 $5,000,000 Capital gain loss 400.000 -400,000 Coupon rate 2.05% 2.05% Remaining maturity 8 years 8 years Investment view Overvalued Undervalued Income tax rate 39% Capital gains tax rate 30% PRACTICE PROBLEM: Ccile Perreaux is a junior analyst for an international wealth management firm. Her supervis, The following information relates to Questions 1-6 Margit Daasvand, asks Perreaux to evaluate three fixed-income funds as part of the firm's global fixed-income offerings. Selected financial data for the funds Aschel, Permot, and Rosalso a presented in Exhibit 1. In Perreaux's initial review, she assumes that there is no reinvestment income and that the yield curve remains unchanged. Exhibit 1. Selected Data on Fixed-Income Funds Aschel Permof Rosaiso Current average bond price $117.00 $91.50 $94.60 Expected average bond price in one year (end of Year 1) 5114.00 596.00 $97.00 Average modified duration 7.07 738 6.99 Average mal coupon payment $3.63 $6.07 S6.36 Presest value of portfolio's assets (milions) 5136.33 568 50 $74.38 Bond type Fixed-coupon bonds 9596 389 Floating-coupon bonds 29 3490 178 Inflation-linked bonds 396 28% 21% Quality AAA 659 15 20% BBB 356 65% 50% B 0% 20% 20% Not rated 06 0" 10% Vase of portfolio's equity (erillions) $94 33 Value of borrowed funds (millions) $42.00 Borrowing rate 2 809 Return on invested finds 6,20% After further review of the composition of each of the funds, Perreaux notes the following Note 1 Aschel is the only fund of the three that uses leverage. Note 2 Rosaiso is the only fund of the three that holds a significant number of bonds with embedded options, Daasvand asks Perreaux to analyze immunization approaches to liability-based mandates for a meeting with Villash Foundation. Villash Foundation is a tax-exempt client. Prior to the meeting Perreaux identifies what she considers to be two key features of a cash flow-matching approach. Feature 1 It requires no yield curve assumptions. Feature 2 Cash flows come from coupons and liquidating bond portfolio positions. Scanned with CamScanner Two years later, Daasvand learns that Villash Foundation needs $5,000,000 in cash to meet liabilities. She asks Perreaux to analyze two bonds for possible liquidation Selected data on the two bonds are presented in Exhibit 2. Exhibit 2. Selected Data for Bonds 1 and 2 Bond 1 Bond 2 Current market value $5,000,000 $5,000,000 Capital gain loss 400.000 -400,000 Coupon rate 2.05% 2.05% Remaining maturity 8 years 8 years Investment view Overvalued Undervalued Income tax rate 39% Capital gains tax rate 30%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts