Question: This assignment will be marked!!! Please email your solution before Monday 28 March 2022. Competitive equilibrium with CARA Bernoulli utility function Consider an asset exchange

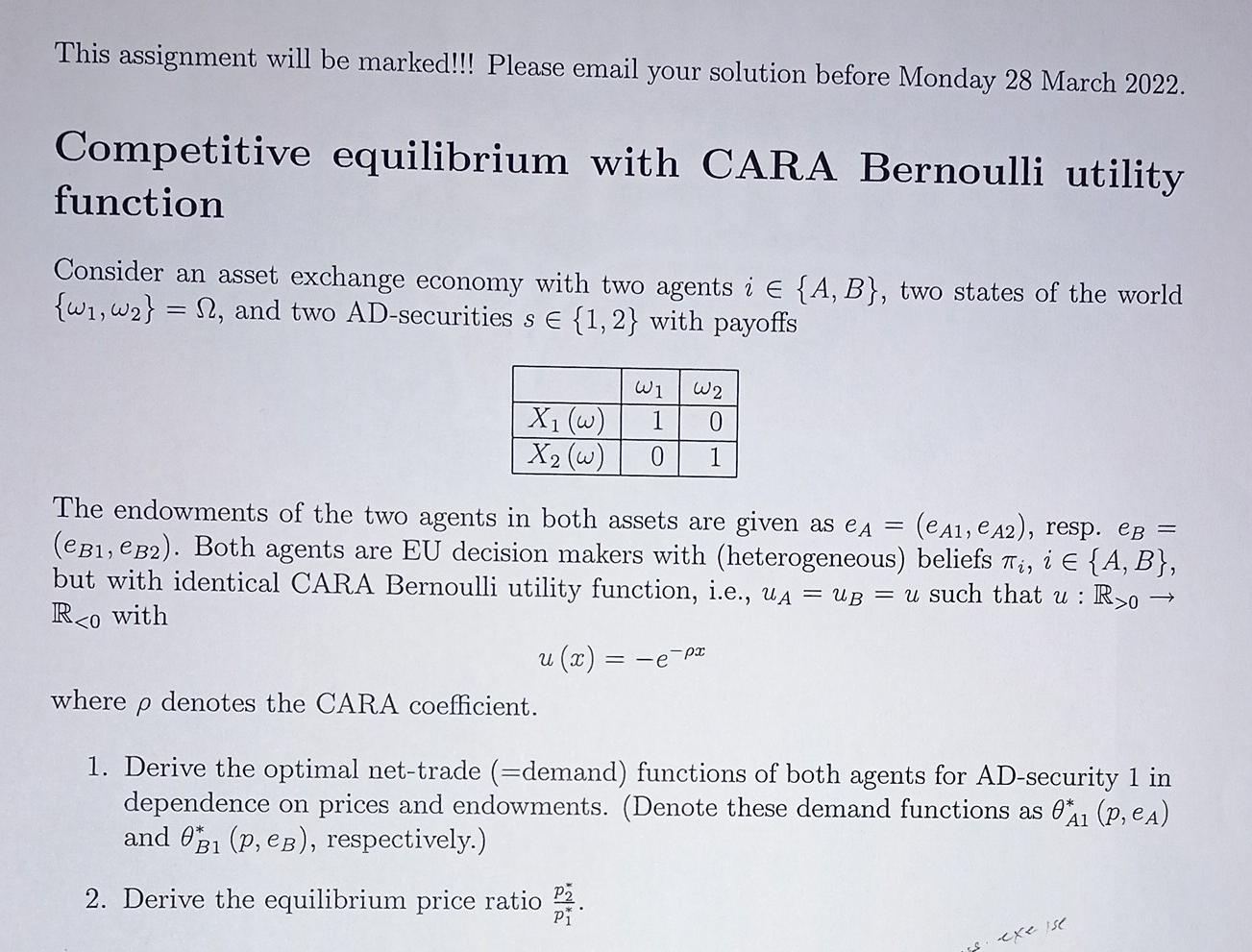

This assignment will be marked!!! Please email your solution before Monday 28 March 2022. Competitive equilibrium with CARA Bernoulli utility function Consider an asset exchange economy with two agents i E {A, B}, two states of the world {w1,w2} = 12, and two AD-securities s E {1, 2} with payoffs Wi 1 0 X, (W) X2 (W) 0 1 The endowments of the two agents in both assets are given as ea = (eai, e A2), resp. eB = (@B1, (B2). Both agents are EU decision makers with (heterogeneous) beliefs Ti, i E {A, B}, but with identical CARA Bernoulli utility function, i.e., UA = us = u such that u : R20 Rco with (a) where denotes the CARA coefficient. u =-epx 1. Derive the optimal net-trade (=demand) functions of both agents for AD-security 1 in dependence on prices and endowments. (Denote these demand functions as 0%1 (p, ea) and 0B1 (P, eb), respectively.) 2. Derive the equilibrium price ratio pa. Pi exe ise This assignment will be marked!!! Please email your solution before Monday 28 March 2022. Competitive equilibrium with CARA Bernoulli utility function Consider an asset exchange economy with two agents i E {A, B}, two states of the world {w1,w2} = 12, and two AD-securities s E {1, 2} with payoffs Wi 1 0 X, (W) X2 (W) 0 1 The endowments of the two agents in both assets are given as ea = (eai, e A2), resp. eB = (@B1, (B2). Both agents are EU decision makers with (heterogeneous) beliefs Ti, i E {A, B}, but with identical CARA Bernoulli utility function, i.e., UA = us = u such that u : R20 Rco with (a) where denotes the CARA coefficient. u =-epx 1. Derive the optimal net-trade (=demand) functions of both agents for AD-security 1 in dependence on prices and endowments. (Denote these demand functions as 0%1 (p, ea) and 0B1 (P, eb), respectively.) 2. Derive the equilibrium price ratio pa. Pi exe ise

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts