Question: This is a Financial Mathematics Problem. (American Options) Implement in Matlab the binOmial~tree based pricing algorithm discussed in class for the American put Option. Use

This is a Financial Mathematics Problem.

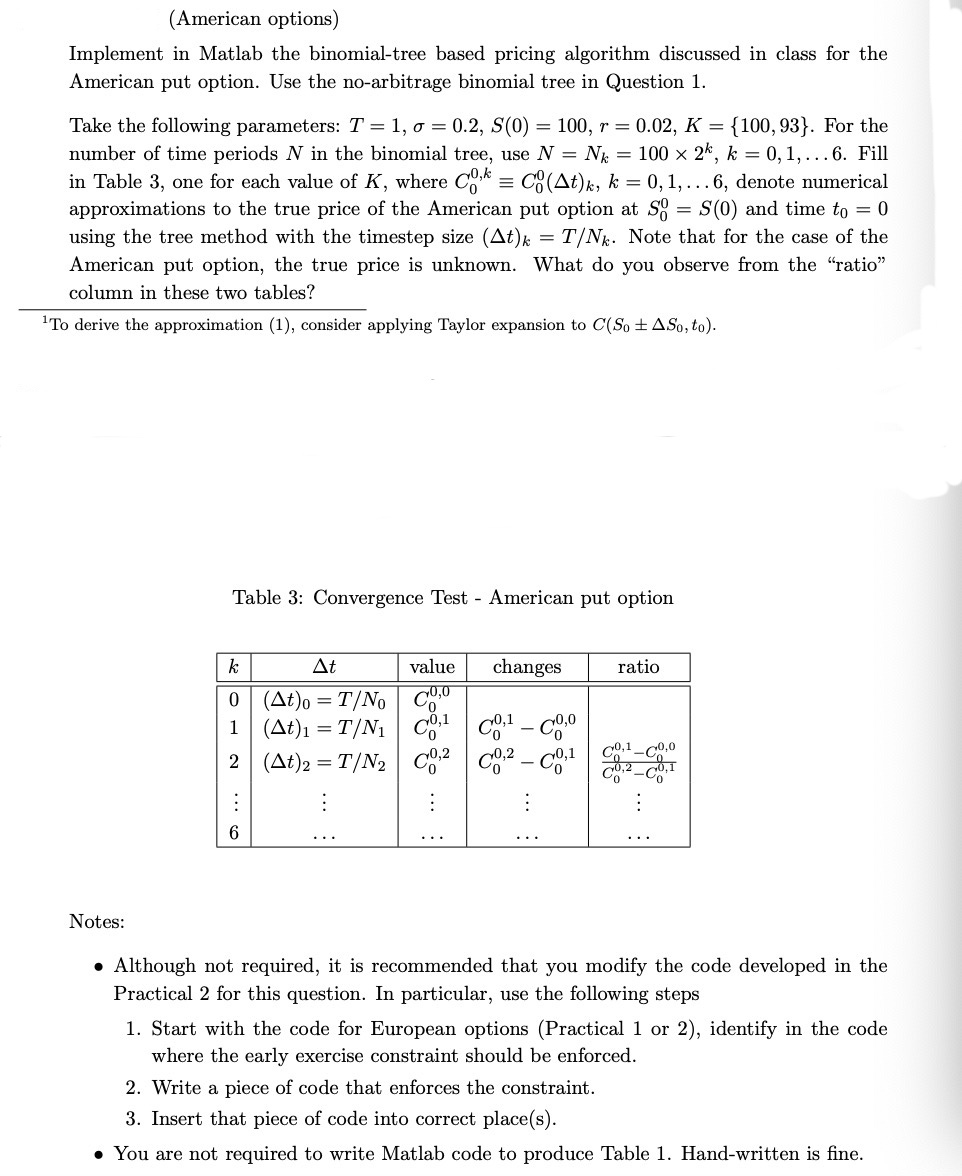

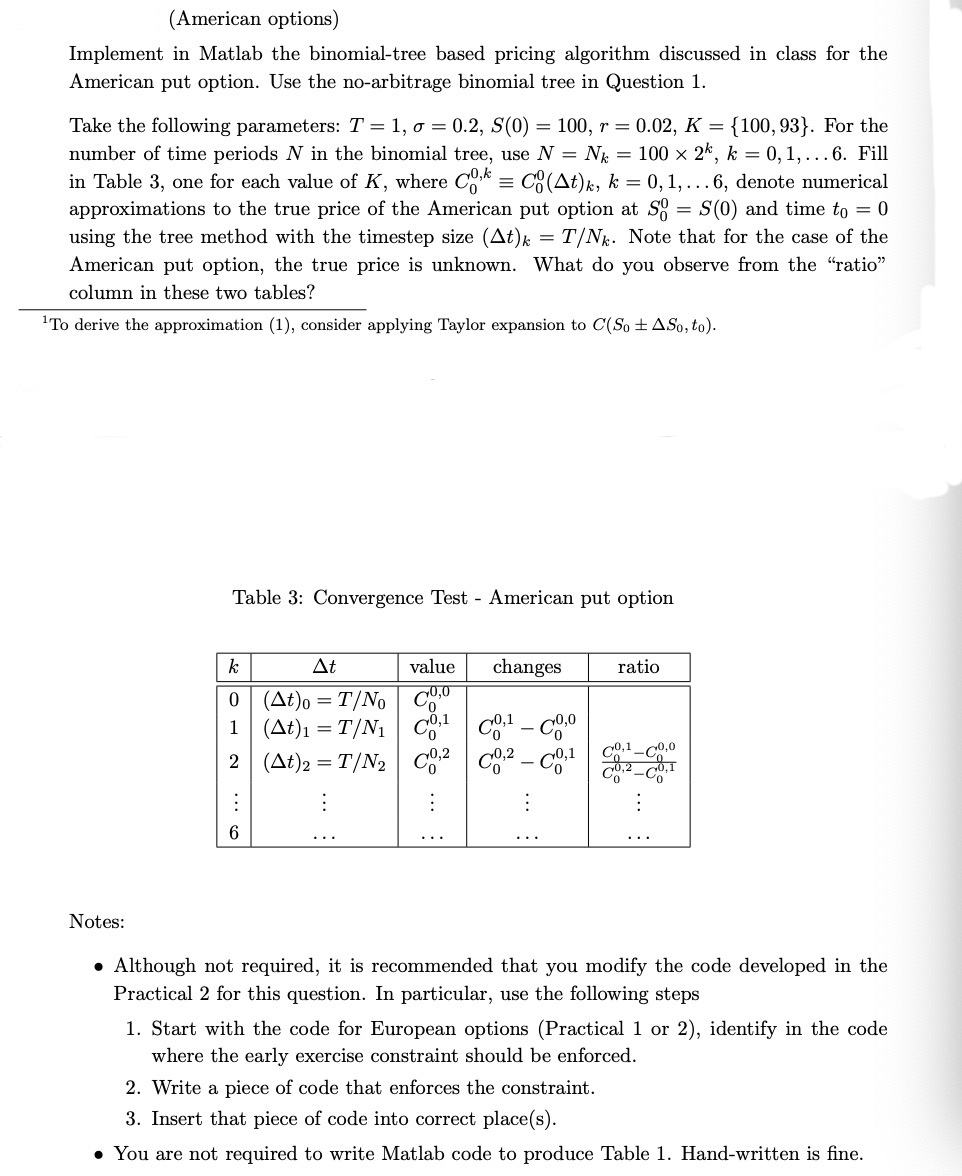

(American Options) Implement in Matlab the binOmial~tree based pricing algorithm discussed in class for the American put Option. Use the nowarbitrage binomial tree in Question 1. Take the following parameters: T = 1, or = 0.2, 3(0) = 100, r = 0.02, K = {100, 93}. For the number of time periods N in the binomial tree, use N = N}, = 100 X 2"", k = 0,1,. . .6. Fill in Table 3, one for each value of K, where 03"" E C'E(At)k, k = 0, 1,. . .6, denote numerical approximations to the true price Of the American put Option at SD" = 5(0) and time to = 0 using the tree method with the tiniestep size (At);, = T/Nk. Note that for the case Of the American put Option, the true price is unknown. What do you observe from the "ratio" column in these two tables? 1Tb derive the approximation (1), consider applying Taylor expansion to C(Sa :l: A39, to). Table 3: COnvergence Test American put OptiOn Notes: 9 Although not required, it is recommended that you modify the code developed in the Practical 2 for this questiOn. In particular, use the following steps 1. Start with the code for EurOpean Options (Practical 1 or 2), identify in the code where the early exercise constraint should be enforced. 2. Write a piece Of code that enforces the COnstraint. 3. Insert that piece Of code into correct place(s). o YOu are not required tO write Matlab code tO produce Table 1. Handrwritten is ne

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts