Question: This is a problem asking you to find the arbitrage free settlement or deliv- ered price in futures markets. The second part of the problem

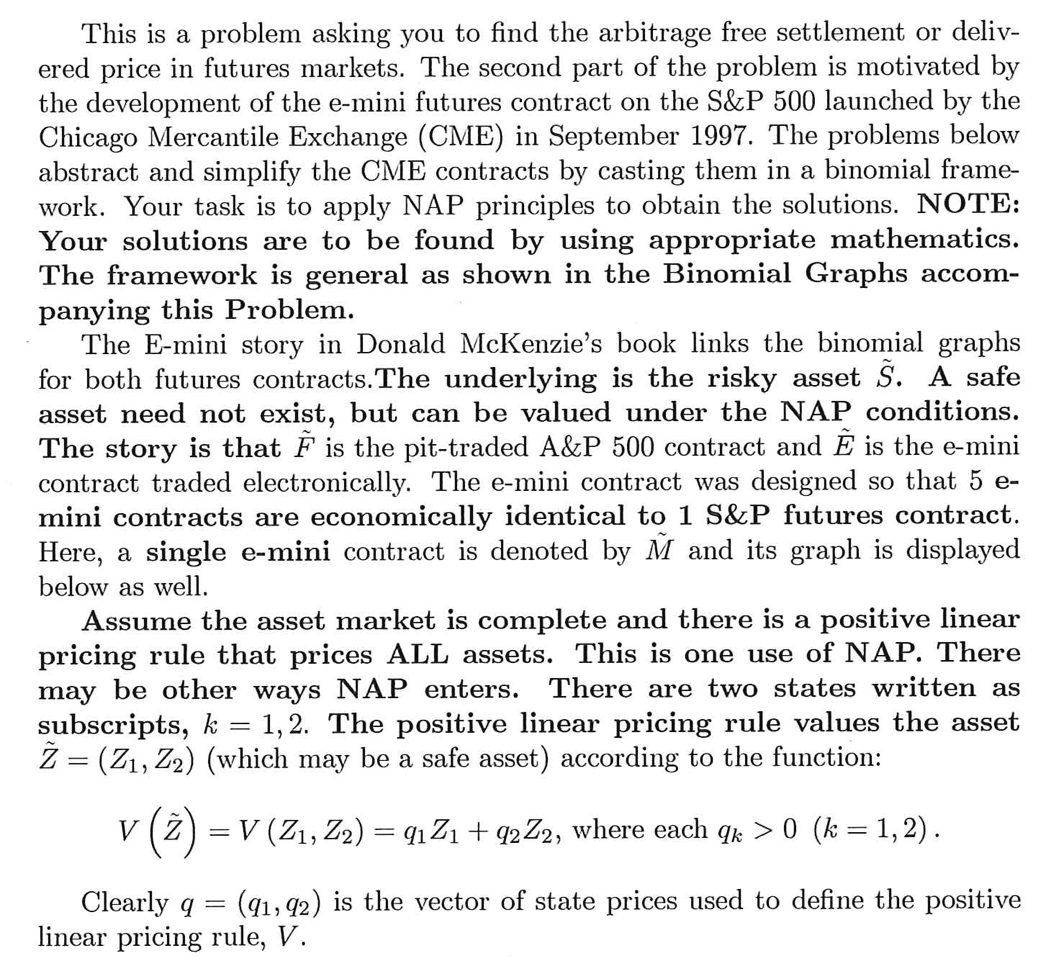

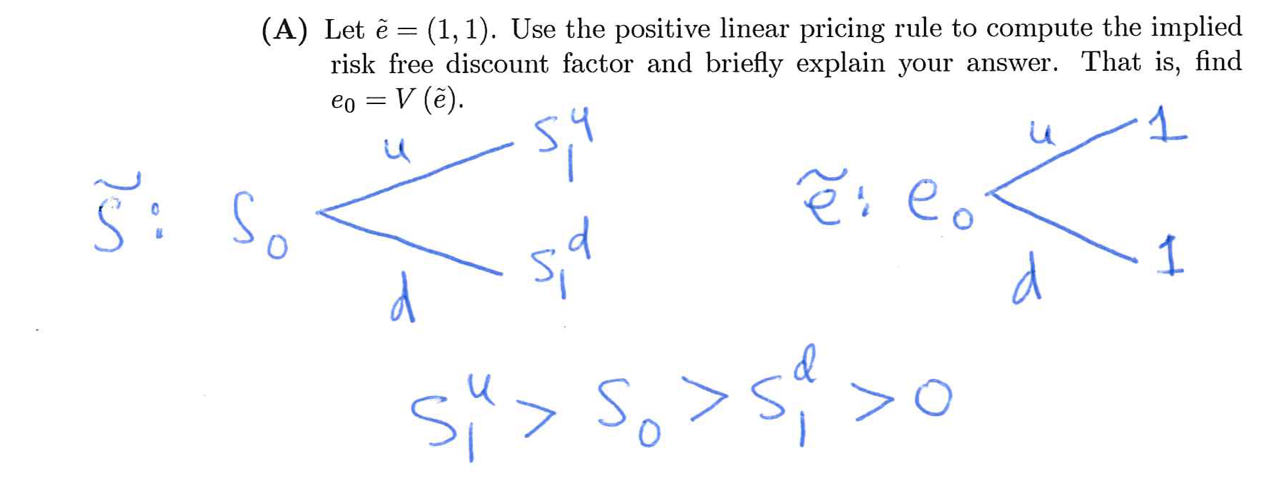

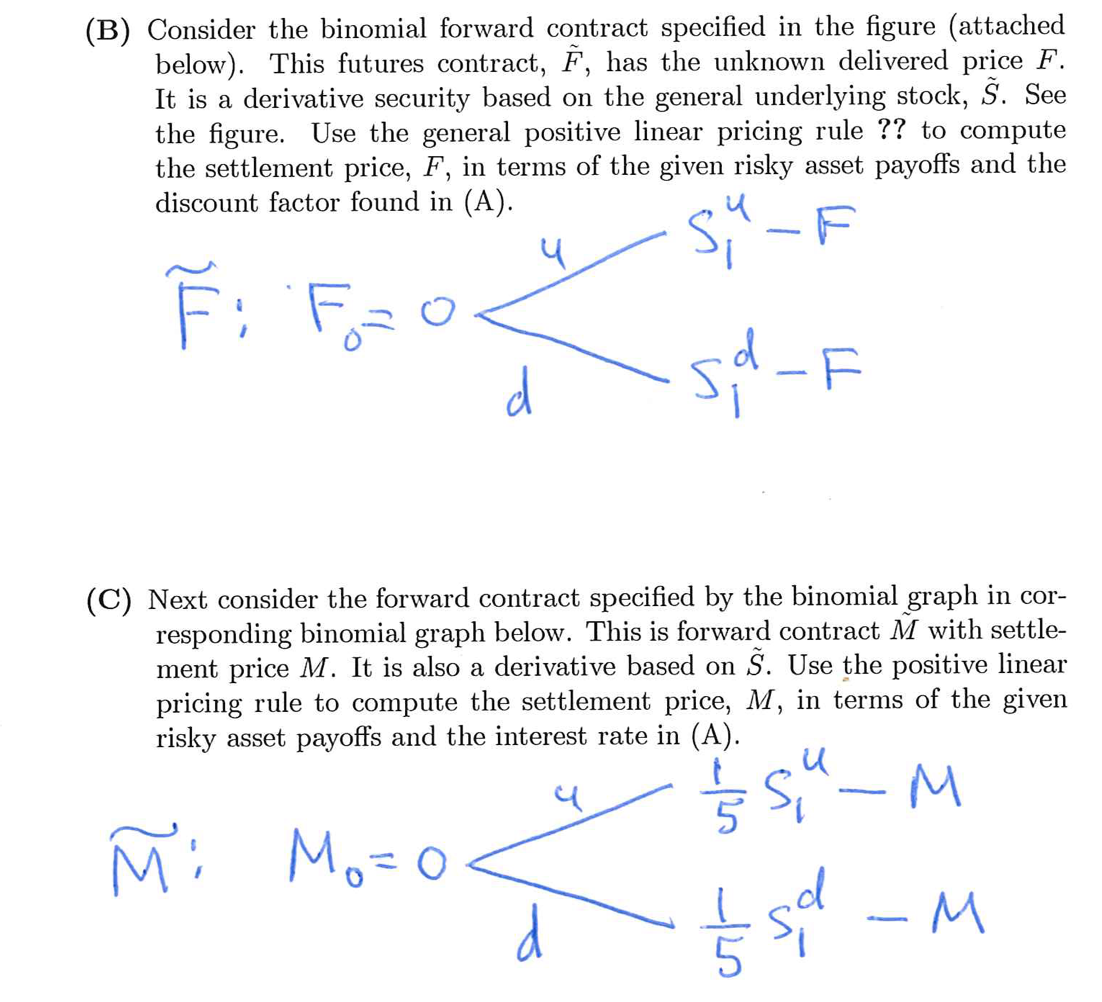

This is a problem asking you to find the arbitrage free settlement or deliv- ered price in futures markets. The second part of the problem is motivated by the development of the e-mini futures contract on the S&P 500 launched by the Chicago Mercantile Exchange (CME) in September 1997. The problems below abstract and simplify the CME contracts by casting them in a binomial frame- work. Your task is to apply NAP principles to obtain the solutions. NOTE: Your solutions are to be found by using appropriate mathematics. The framework is general as shown in the Binomial Graphs accom- panying this Problem. The E-mini story in Donald McKenzie's book links the binomial graphs for both futures contracts.The underlying is the risky asset S. A safe asset need not exist, but can be valued under the NAP conditions. The story is that F is the pit-traded A&P 500 contract and E is the e-mini contract traded electronically. The e-mini contract was designed so that 5 e- mini contracts are economically identical to 1 S&P futures contract. Here, a single e-mini contract is denoted by M and its graph is displayed below as well. Assume the asset market is complete and there is a positive linear pricing rule that prices ALL assets. This is one use of NAP. There may be other ways NAP enters. There are two states written as subscripts, = 1,2. The positive linear pricing rule values the asset Z = (21, Z5) (which may be a safe asset) according to the function: (2) =V (Z1,2Z2) = @1 Z1 + q2Z2, where each , >0 (k=1,2). Clearly = (q1,2) is the vector of state prices used to define the positive linear pricing rule, V. (A) Let = (1,1). Use the positive linear pricing rule to compute the implied risk free discount factor and briefly explain your answer. That is, find o=::()- SI\\'\\ " A St So>g| 0 (B) Consider the binomial forward contract specified in the figure (attached below). This futures contract, F, has the unknown delivered price F. It is a derivative security based on the general underlying stock, S. See the figure. Use the general positive linear pricing rule 77 to compute the settlement price, F, in terms of the given risky asset payoffs and the discount factor found in (A). % Y 2| ~" Fy Fa @ 9/ \\ A~ AN S. I T) (C) Next consider the forward contract specified by the binomial graph in cor- responding binomial graph below. This is forward contract M with settle- ment price M. It is also a derivative based on S. Use the positive linear pricing rule to compute the settlement price, M, in terms of the given risky asset payoffs and the interest rate in (A). N Lg M Mo Mo L A T2 M (D) Briefly explain the relationship between your answers in Parts (B) and (C) by a No Arbitrage argument. Put differently, what is the mathematical relationship between the delivered prices of the two contracts? What happens if that relation is violated in the marketplace? Comment: You may want to redraw the binomial graph for the e-mini contract to reflect its claim economic equivalence with the S&P pit trade contract

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!