Question: This is a question from 'capital market theory' course. Please help me how to solve this problem. 3. Today is June 30 2019, and you

This is a question from 'capital market theory' course.

Please help me how to solve this problem.

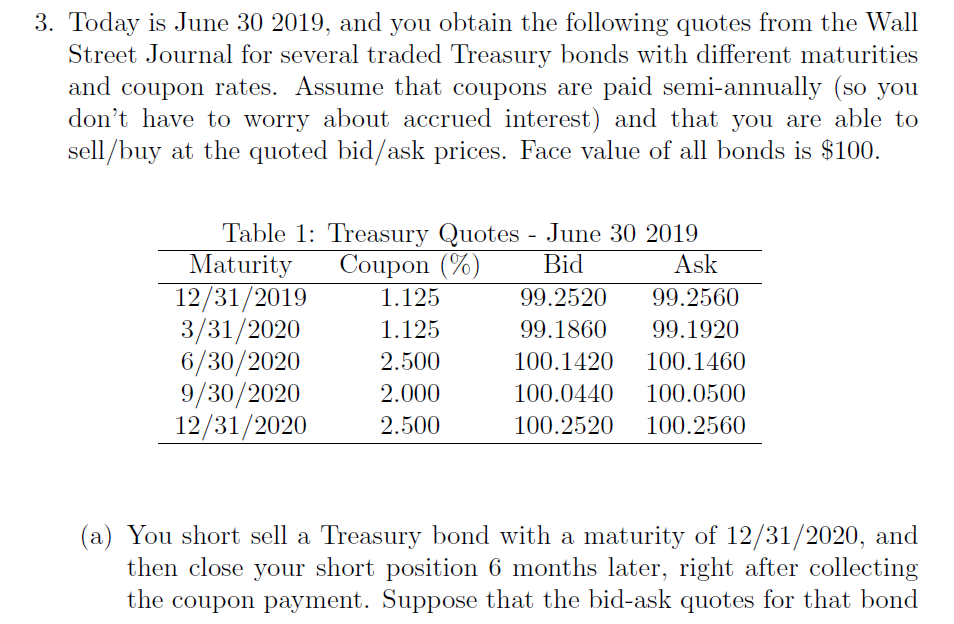

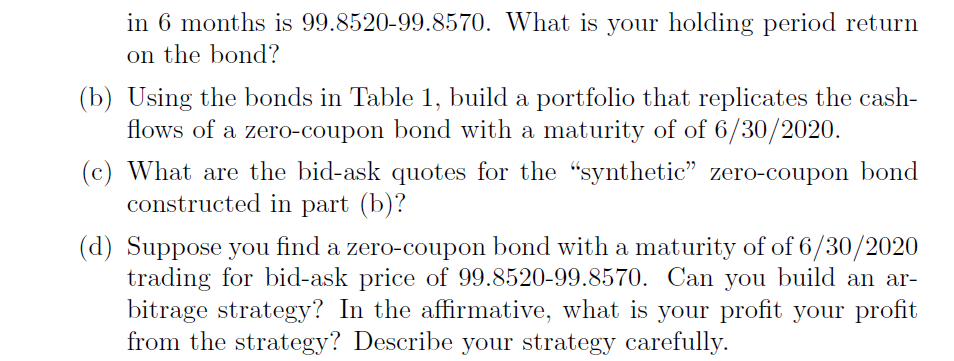

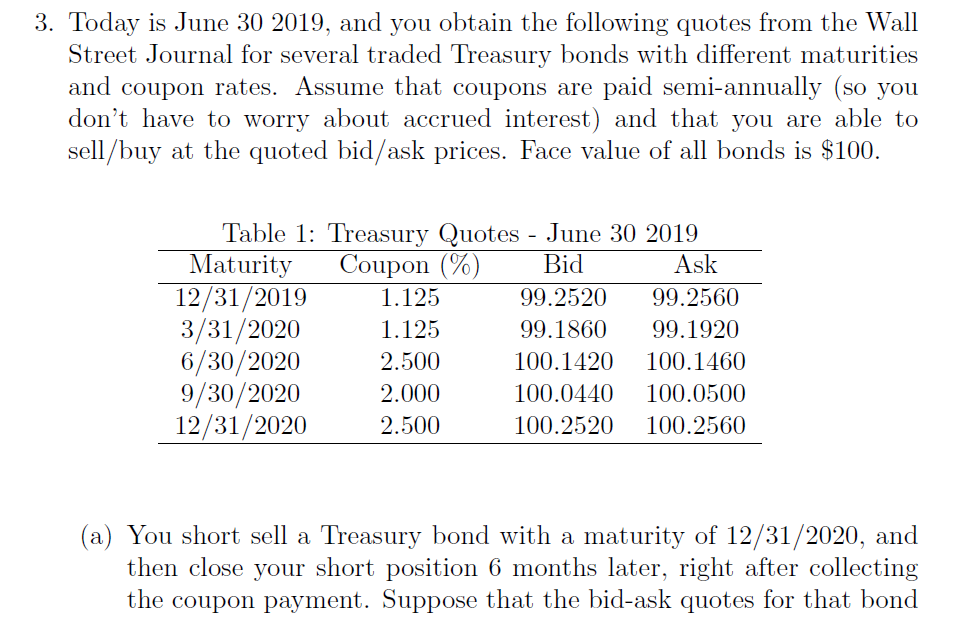

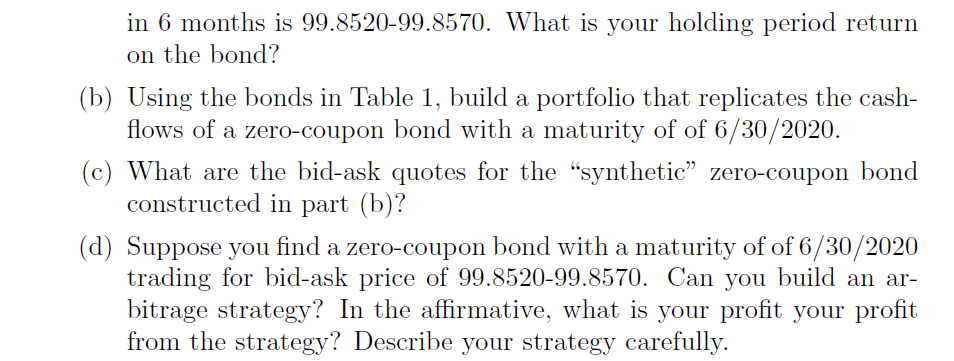

3. Today is June 30 2019, and you obtain the following quotes from the Wall Street Journal for several traded Treasury bonds with different maturities and coupon rates. Assume that coupons are paid semi-annually (so you don't have to worry about accrued interest) and that you are able to sell/buy at the quoted bid/ask prices. Face value of all bonds is $100. Table 1: rIi'easury Quotes June 30 2019 Maturity Coupon (%) Bid Ask 12/31/2019 1.125 99.2520 99.2560 3/31/2020 1.125 99.1860 99.1920 5/30/2020 2.500 100.1420 100.1460 9/30/2020 2.000 100.0440 100.0500 12/31/2020 2.500 100.2520 100.2560 (a) You short sell a Treasury bond with a maturity of 12/31/2020, and then close your short position 6 months later, right after collecting the coupon payment. Suppose that the bid-ask quotes for that bond in 6 months is 998520998570. What is your holding period return on the bond? Using the bonds in Table 1, build a portfolio that replicates the cash ows of a zerocoupon bond with a maturity of of 6/30/2020. What are the bidask quotes for the \"synthetic\" zero-coupon bond constructed in part (b)? Suppose you nd a zerocoupon bond with a maturity of of 6 / 30 / 2020 trading for bid-ask price of 99.8520-99.8570. Can you build an ar- bitrage strategy? In the airnlative, what is your prot your prot from the strategy? Describe your strategy carefully

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts