Question: This is a question that I got, also I did my best effort myself So please check my work is on the right track if

This is a question that I got, also I did my best effort myself

So please check my work is on the right track if not would you give me a correct answer?

thank you

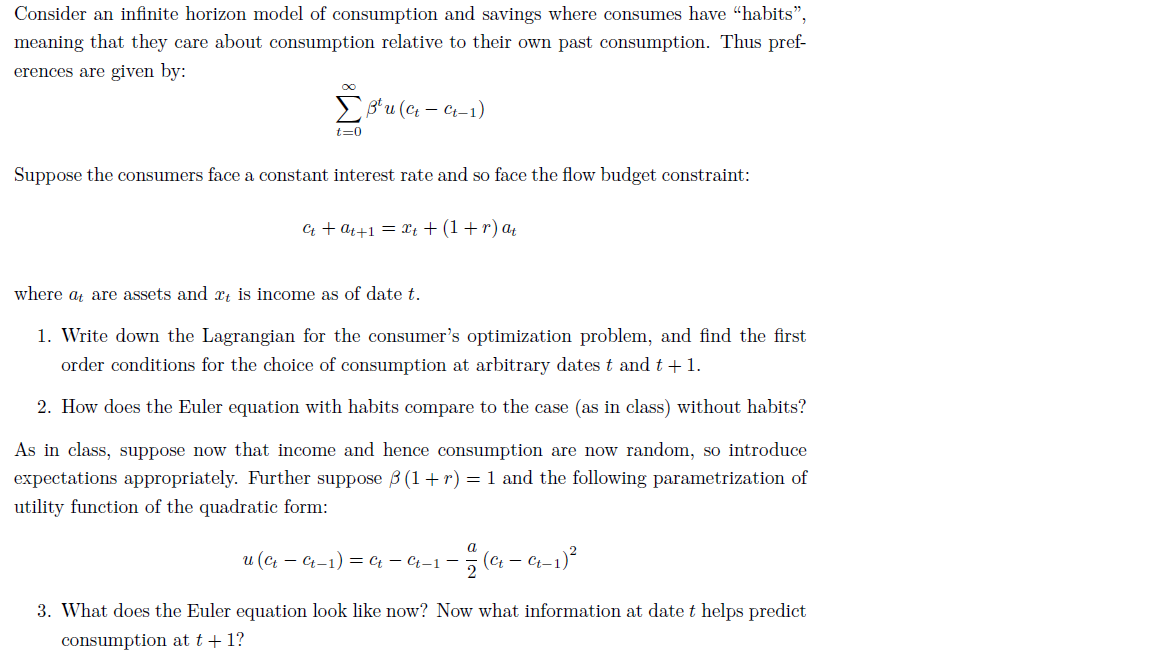

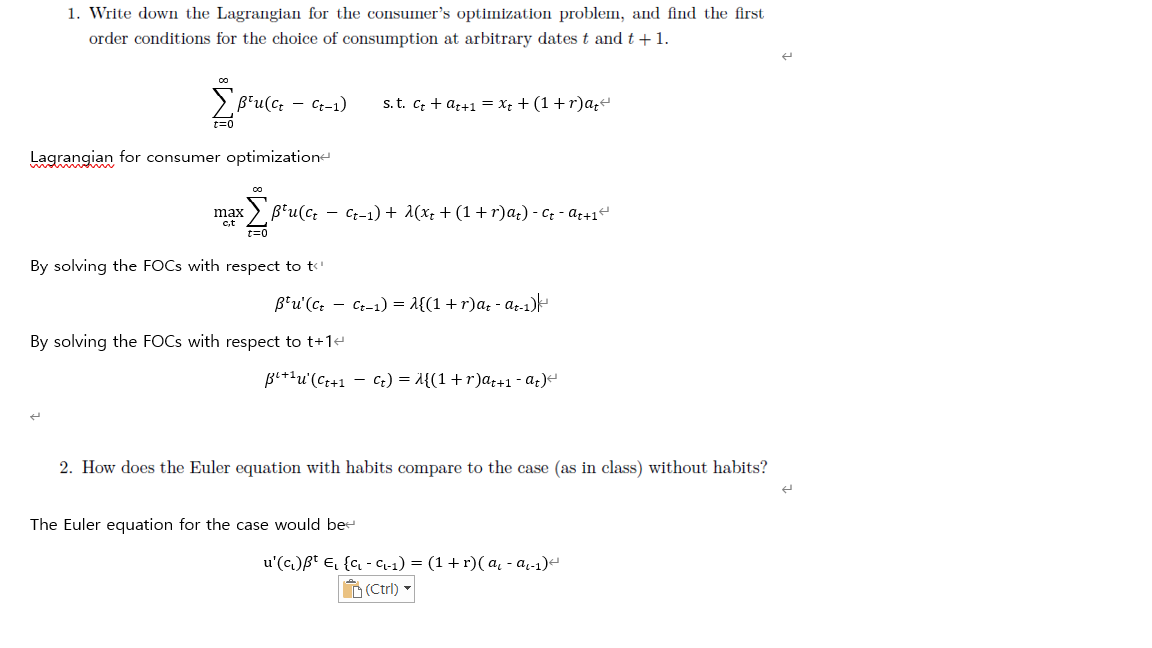

Consider an innite horizon model of consumption and savings where consumes have \"habits\As in class, suppose now that income and hence consumption are now random, so introduce expectations appropriately. Further suppose B (1 + r) = 1 and the following parametrization of utility function of the quadratic form: u ( c - C-1 ) = 0 - 0-1 -5 ( 0 - 0-1)2 3. What does the Euler equation look like now? Now what information at date t helps predict consumption at t + 1? The Euler equation needs to care parametrization of the utility functions u (c) = Et tu (ct - ct-1) * {- a(ct - ct-1) } Also accounted for B(1 + r) = 1. The discount factor and interest rate to predict consumption at t+ 1+ L = Btu(Ct - Ct- 1 ) + 1 (xpu. Ct Is=o(1+Is) Btu' ( ct ) = = T5=0(1 + Is) Bitlu'(Ct+1) = 15=0(1 + Is) u'(ct) = 15=0(1 + Is) Btu(ct - Ct-1) + A(xt + (1 + r)at) - Ct - at+1 By solving the FOCs with respect to to Bu'(ct - Ct-1) = M(1+ r)at - at-1)k By solving the FOCs with respect to t+1+ pittu'(Ct+1 - Ct) = M((1 + r)at+1 - at)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts