Question: This is a question with a negative beta So far, we have been silent about expected returns of assets with negative beta. You conjecture that

This is a question with a negative beta

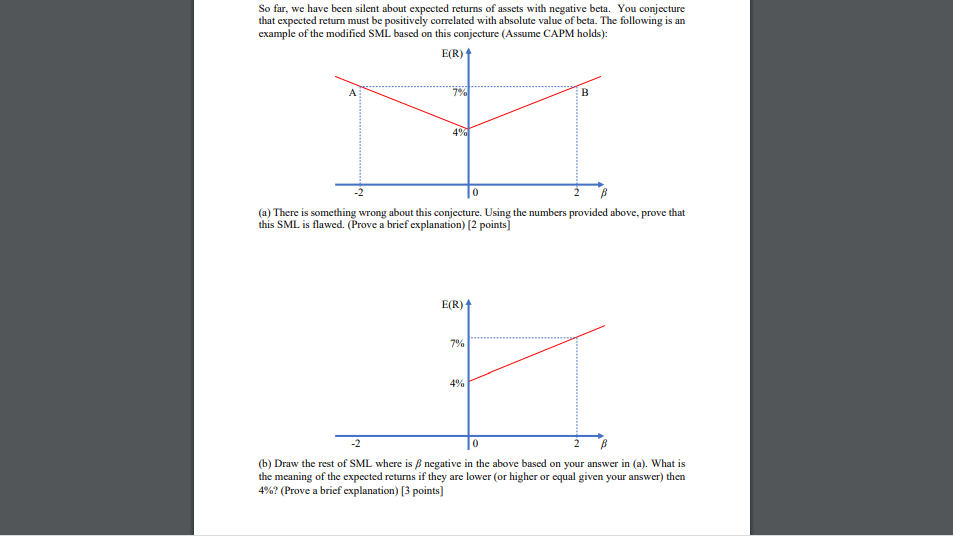

So far, we have been silent about expected returns of assets with negative beta. You conjecture that expected return must be positively correlated with absolute value of beta. The following is an example of the modified SML based on this conjecture (Assume CAPM holds): E(R) A B 49% -2 0 (a) There is something wrong about this conjecture. Using the numbers provided above, prove that this SML is flawed. (Prove a brief explanation) [2 points] E(R) + 7% 4% -2 0 (b) Draw the rest of SML where is & negative in the above based on your answer in (a). What is the meaning of the expected returns if they are lower (or higher or equal given your answer) then 4%? (Prove a brief explanation) [3 points]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts