Question: This is about financial time series. Please write down in details. Thanks. The following is the code for this problem Consider analyze the transaction data

This is about financial time series. Please write down in details. Thanks.

The following is the code for this problem

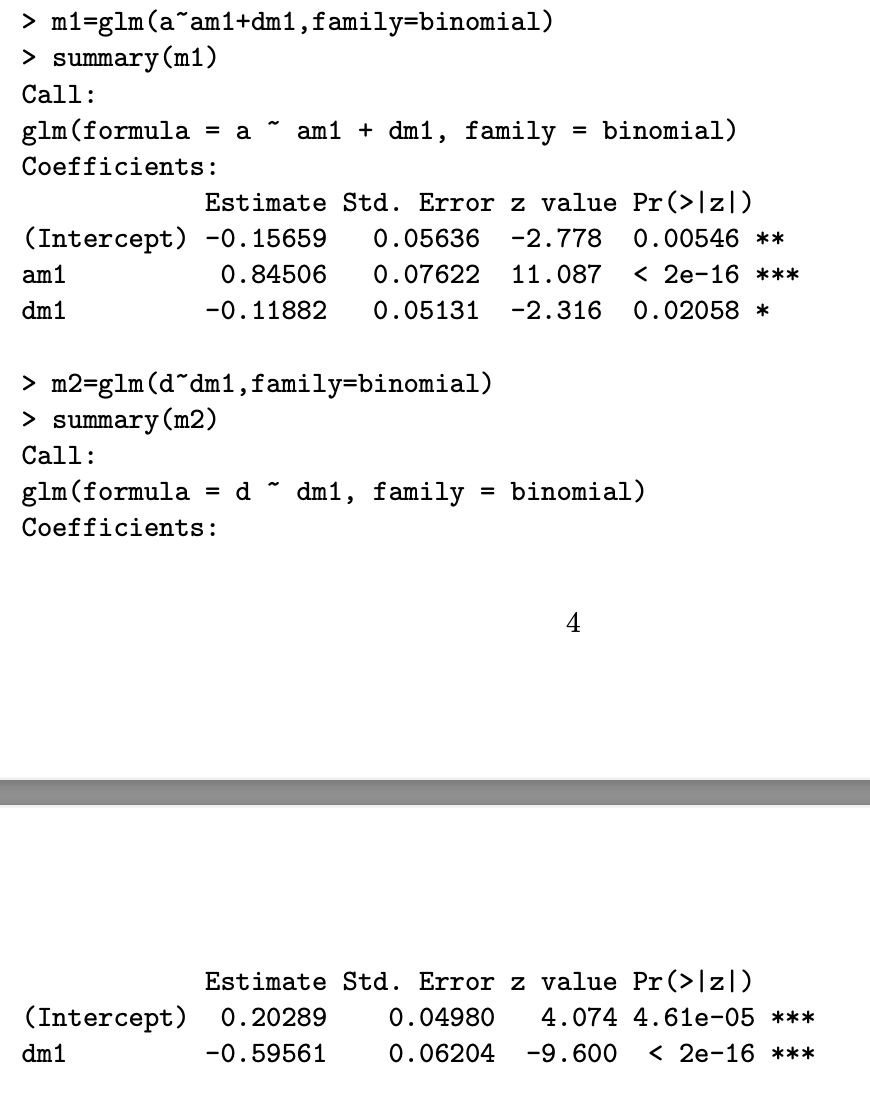

Consider analyze the transaction data using the decomposition model for the price change. In particular, we use logistic regression to estimate the following models logit(Pi) = Bo + B1A;1 + B2 Di-1, = = logit(di) = 40 + 71 Di-1, where Pi P(A; = 1|Fi-1), di = P(D; = 1|A; = 1, Fi-1), and Fi-1 denotes the information available at the 1th transaction. The outputs are attached. (a) What is the probability pi if Ai-1 = 0? What is the probability pi if Ai-1 = 1 and Di-1 = -1? Show computations. (4 points) = -1 =- = = (b) What is the probability di when Ai-1 = Di-1 1? What is the probability P(Di -1|A; = 1, Fi-1) when Ai-1 = 1 and Di-1 computations. (4 points) = = = -1? Show N = a > m1=glm(a^am1+dm1, family=binomial) > summary (m1) Call: glm (formula am 1 + dm1, family = binomial) Coefficients: Estimate Std. Error z value Pr(>[z]) (Intercept) -0.15659 0.05636 -2.778 0.00546 ** am1 0.84506 0.07622 11.087 m2=glm (ddm1, family=binomial) > summary (m2) Call: glm (formula = d dm1, family Coefficients: = binomial) 4 (Intercept) dm 1 Estimate Std. Error z value Pr(>[z]) 0.20289 0.04980 4.074 4.61e-05 *** -0.59561 0.06204 -9.600 m1=glm(a^am1+dm1, family=binomial) > summary (m1) Call: glm (formula am 1 + dm1, family = binomial) Coefficients: Estimate Std. Error z value Pr(>[z]) (Intercept) -0.15659 0.05636 -2.778 0.00546 ** am1 0.84506 0.07622 11.087 m2=glm (ddm1, family=binomial) > summary (m2) Call: glm (formula = d dm1, family Coefficients: = binomial) 4 (Intercept) dm 1 Estimate Std. Error z value Pr(>[z]) 0.20289 0.04980 4.074 4.61e-05 *** -0.59561 0.06204 -9.600

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts