Question: This is the fourth time posting this question. God damm give me the right answer!!! Suppose that the Index model for stocks A and B

This is the fourth time posting this question. God damm give me the right answer!!!

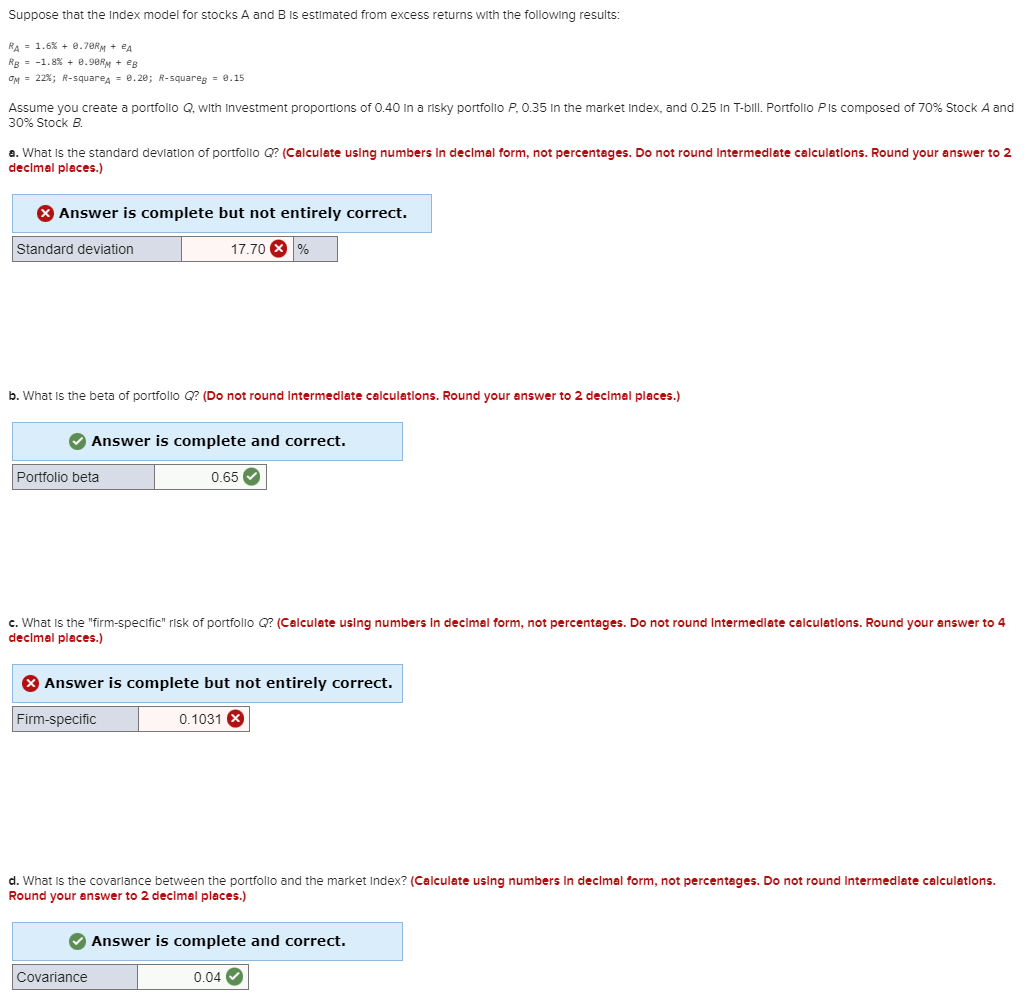

Suppose that the Index model for stocks A and B is estimated from excess returns with the following results: RA=1.6%+.7RM+eA RB=1.8%+.90RM+eB M=22%;R-square eA=0.20; R-square eB=0.15 Assume you create a portfolio Q, with Investment proportions of 0.40 in a risky portfolio P,0.35 in the market index, and 0.25 in T-bill. Portfolio P is composed of 70% Stock A and 30% Stock B. a. What is the standard devlation of portfolio Q ? (Calculate using numbers In decimal form, not percentages. Do not round Intermedlate calculations. Round your answer to 2 decimal places.) X Answer is complete but not entirely correct. b. What is the beta of portfolio Q ? (Do not round Intermedlate calculations. Round your answer to 2 decimal places.) Answer is complete and correct. c. What Is the "firm-specific" risk of portfolio Q? (Calculate using numbers in decimal form, not percentages. Do not round Intermedlate calculations. Round your answer to 4 decimal places.) Answer is complete but not entirely correct. d. What is the covarlance between the portfollo and the market index? (Calculate using numbers In decimal form, not percentages. Do not round Intermedlate calculations. Round your answer to 2 decimal places.) Suppose that the Index model for stocks A and B is estimated from excess returns with the following results: RA=1.6%+.7RM+eA RB=1.8%+.90RM+eB M=22%;R-square eA=0.20; R-square eB=0.15 Assume you create a portfolio Q, with Investment proportions of 0.40 in a risky portfolio P,0.35 in the market index, and 0.25 in T-bill. Portfolio P is composed of 70% Stock A and 30% Stock B. a. What is the standard devlation of portfolio Q ? (Calculate using numbers In decimal form, not percentages. Do not round Intermedlate calculations. Round your answer to 2 decimal places.) X Answer is complete but not entirely correct. b. What is the beta of portfolio Q ? (Do not round Intermedlate calculations. Round your answer to 2 decimal places.) Answer is complete and correct. c. What Is the "firm-specific" risk of portfolio Q? (Calculate using numbers in decimal form, not percentages. Do not round Intermedlate calculations. Round your answer to 4 decimal places.) Answer is complete but not entirely correct. d. What is the covarlance between the portfollo and the market index? (Calculate using numbers In decimal form, not percentages. Do not round Intermedlate calculations. Round your answer to 2 decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts