Question: This question from Financial statistics I need the manual solution . i need solution with show all steps plz plz write all steps in solution

This question from Financial statistics

I need the manual solution .

i need solution with show all steps plz

plz write all steps in solution

show all steps plz and how you conclude the result

I need the manual solution .

Please write and clarify all the steps and laws used in the solution, in addition to writing a description or explanation of the final result.

i need solve for all questions

write all steps and rules you use

please explain your answer

_____________________________________________________________________________________________________________________

If you need similar examples to solve the question

I will attach two examples with the solution to clarify and give more information to the question

I need to solve both questions in a similar way to solve the examples I added

Thank you

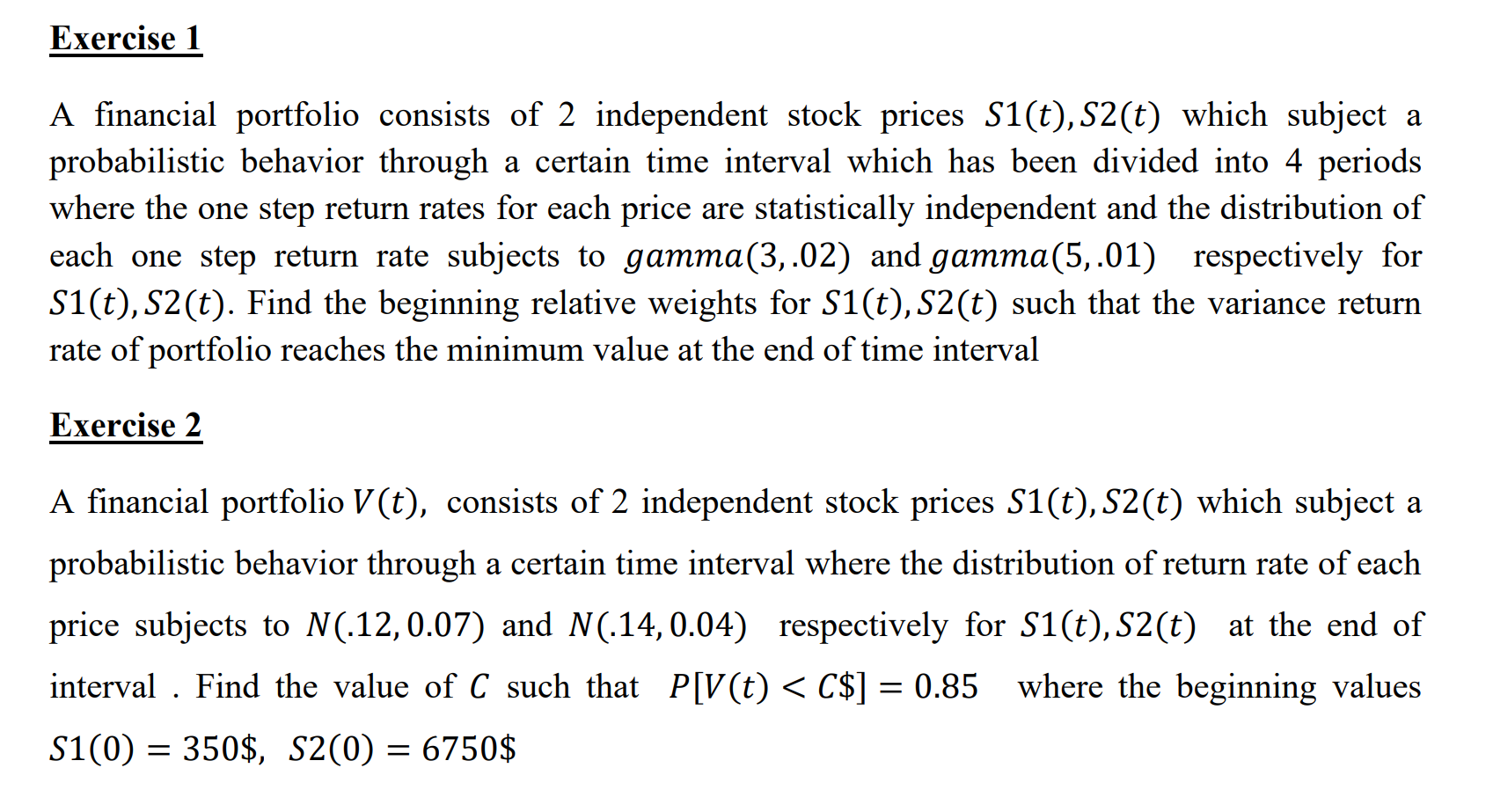

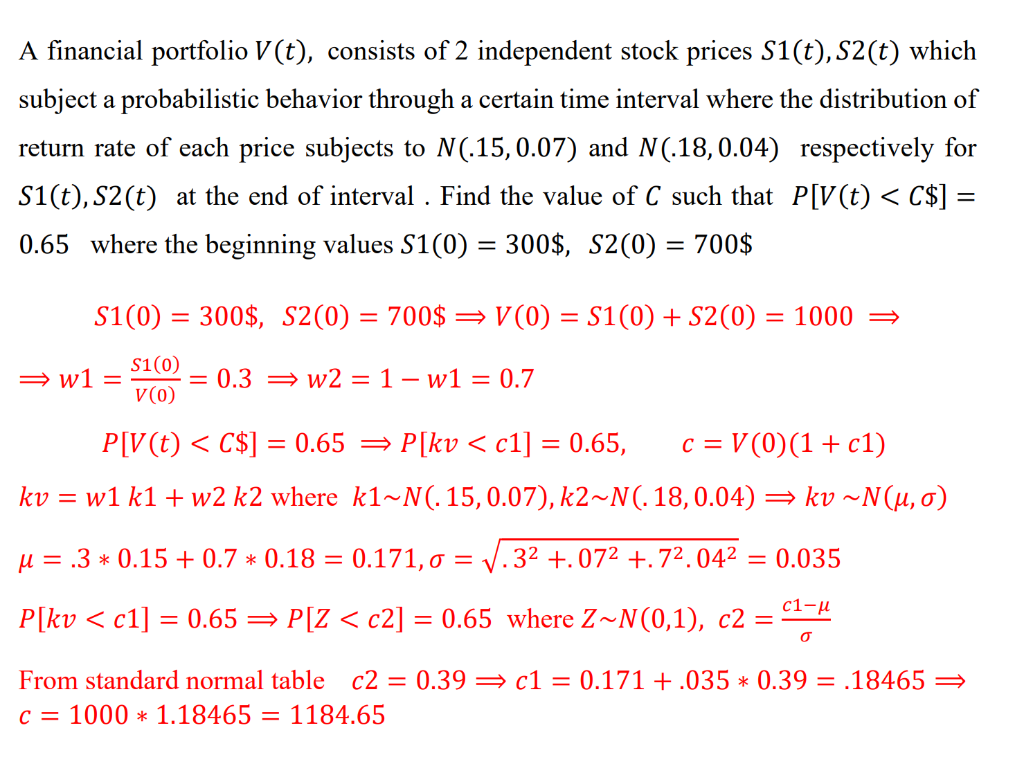

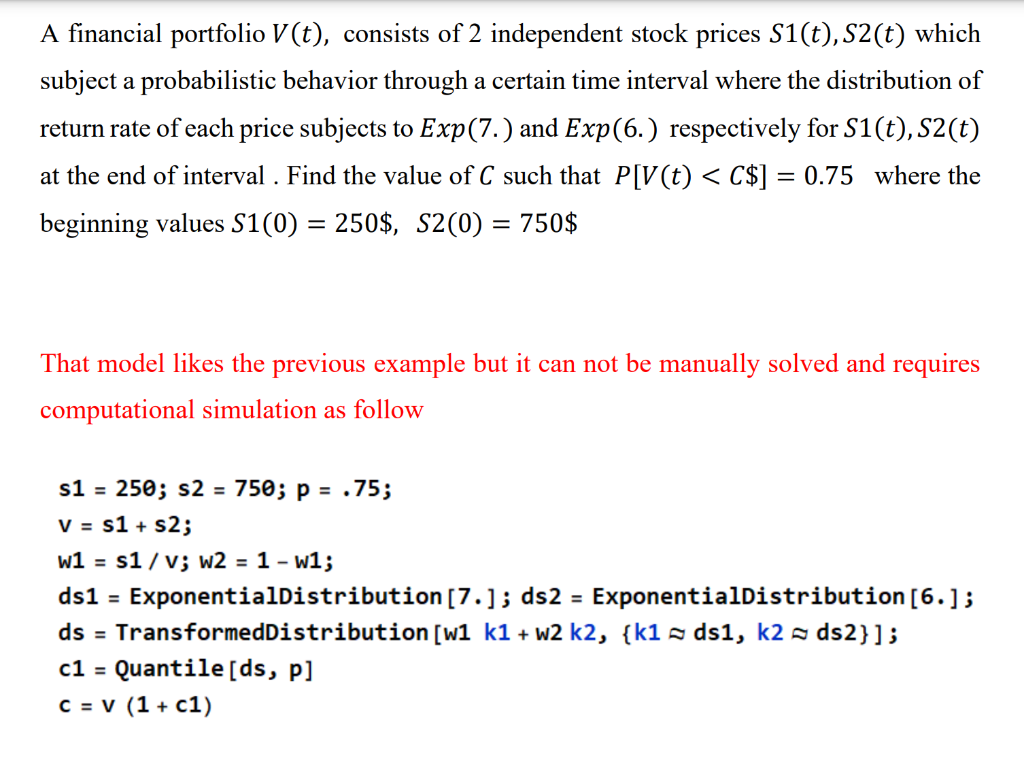

Exercise 1 A financial portfolio consists of 2 independent stock prices S1(t), S2(t) which subject a probabilistic behavior through a certain time interval which has been divided into 4 periods where the one step return rates for each price are statistically independent and the distribution of each one step return rate subjects to gamma(3,.02) and gamma(5,.01) respectively for S1(t), S2(t). Find the beginning relative weights for S1(t), S2(t) such that the variance return rate of portfolio reaches the minimum value at the end of time interval Exercise 2 A financial portfolio V(t), consists of 2 independent stock prices $1(t), S2(t) which subject a probabilistic behavior through a certain time interval where the distribution of return rate of each price subjects to N(.12, 0.07) and N(.14, 0.04) respectively for $1(c), S2(t) at the end of interval . Find the value of C such that P[V(t) kv ~(u, o) kv = u = .3 * 0.15 +0.7 * 0.18 = 0.171,0 = 1.32 +.072 +. 72.042 = 0.035 = = = c1-u P[kv kv ~(u, o) kv = u = .3 * 0.15 +0.7 * 0.18 = 0.171,0 = 1.32 +.072 +. 72.042 = 0.035 = = = c1-u P[kv

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts