Question: This question is all about understanding!! P Ltd is the parent of S Ltd. On 1 January 2021 P sold inventory to Sfor $21,000. The

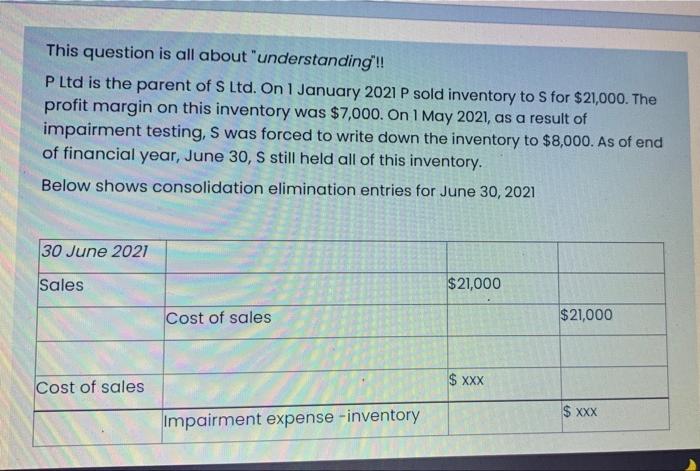

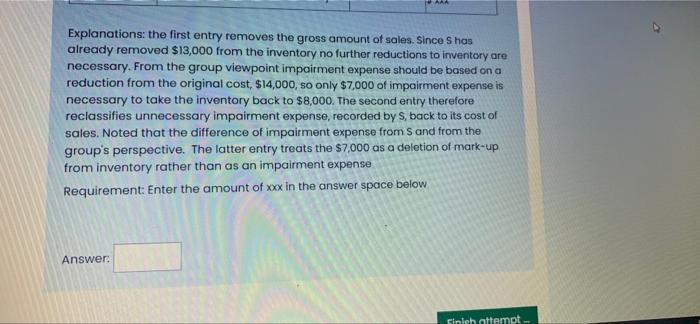

This question is all about "understanding!! P Ltd is the parent of S Ltd. On 1 January 2021 P sold inventory to Sfor $21,000. The profit margin on this inventory was $7,000. On 1 May 2021, as a result of impairment testing, S was forced to write down the inventory to $8,000. As of end of financial year, June 30, S still held all of this inventory. Below shows consolidation elimination entries for June 30, 2021 30 June 2021 Sales $21,000 Cost of sales $21,000 $ XXX Cost of sales $ xxx Impairment expense -inventory AAA Explanations: the first entry removes the gross amount of sales. Since S has already removed $13,000 from the inventory no further reductions to inventory are necessary. From the group viewpoint impairment expense should be based on a reduction from the original cost, $14,000, so only $7,000 of impairment expense is necessary to take the inventory back to $8,000. The second entry therefore reclassifies unnecessary impairment expense, recorded by S, back to its cost of sales. Noted that the difference of impairment expense from S and from the group's perspective. The latter entry treats the $7,000 as a deletion of mark-up from inventory rather than as an impairment expense Requirement: Enter the amount of xxx in the answer space below Answer: Sinish attempt

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts