Question: This question is based on a supply chain case study on LEGO company 1. How well did Moller Nielsen's plan address the seven types of

This question is based on a supply chain case study on LEGO company

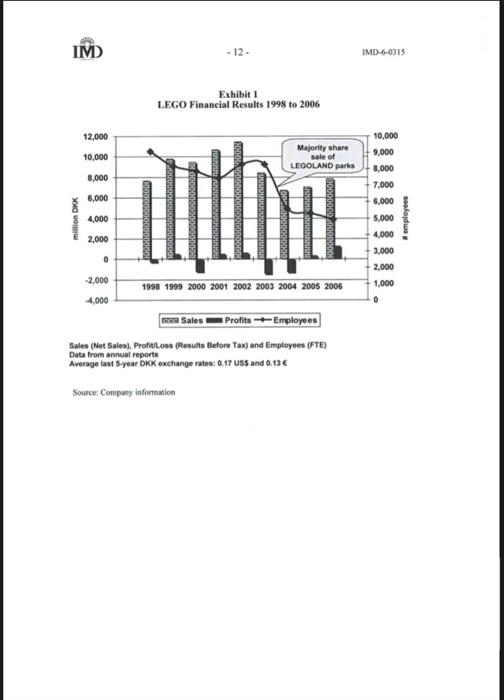

1. How well did Moller Nielsen's plan address the seven types of complexity? 2. How might these changes affect Lego's supply chain risk profile? 3. What are the major weaknesses in the new strategy and how have they contributed to the current problems? 4. Advise Lego on what actions they should take to resolve these problems. 5. What the lessons that can be learned from this case about logistics out-sourcing specifically and change management generally? LEGO: CONSOLIDATING DISTRIBUTION (A) Rrivarh Amonlate Edein It was Neveraber 2006 and Egal Moller Niclach, sernior directoe under the apenieion of tendertaking a very challenging logiscics transformation. Fartier derithouse handing of a company. Genimere simation This had been a stressful year for Mailer Nichen and his tean The implementation had not goee sabocilly and there was sizil much left to do. Fortunately, the "high season" was over, giving Moller Nieises scme time to breathe and plan las nest move. The next phase - the thansfer of the tcmaining eperations to shill the right thing to do? Showld he revise his strancgy? Moller Niclsen had just come out of a mecting with scrive executives for a goino-ge decision on the neat foase. He was sold: slow down further cimaclidetion - what de you recen sent? The cane serien won alle 1. Continue as planned. 2. Kecp the status quo - operale with several DCs for a few more years. 3. Explore other alternatives. Whatever the decision, he wonld have to miove cuickly to be ready before the start of the next peak period in about half a year from now, 2 Frnancial Crisis at the LEGO Group The L.EGO Group was estahlishod in 1912 by Ole Kiek. Kristiansen in bis carpenter The LEGO Group was established in 1932 by Ole Kirk Kristiansen in his carpenter shop in Billund, Denmark. For almost 70 years it saw steady growth in both sales and profits until, in 1998 , this successful streak came to an abrupt end and the company started losing money. Staff reductions followed for the first time in its history, and L.EGO set out on a path of innovative new product development. By the end of 2002 the company appeared to have turned the comer - net cash flow was positive once again and sales reached record highs. But inventory and receivables were also up, and when retailers'. Christmas sales proved to be disappointing - especially in its largest markets - L.EGO braced itself for another difficult year. What happened next exceeded even the company's own worst-case scenario: Sales dropped 26% in 2003 alone and another 20% in 2004 . This resulted in the largest losses in the company's history over two successive years (refer to Exlribit I for a financial overview). calling into question the effectiveness of the measures taken in response to the 1998 loss. 2004: A Costly and Complex Supply Chain The company's leadership knew that the supply chain posed the most immediate opportunity for significant improvements. It was selling creative toy products in a competitive and highly seasonal global marketplace. But it did not have a flexible enough supply chain to deal with these great fluctuations. The company's focus on creativity, innovation and superior quality had, over time, created high complexity in the supply chain. L.FGO's motto - "Only the best is good enough" - had contributed to an emphasis on creating, selling and delivering toys at any cost, without regard for practicalities. To rebuild profitability, the company had to reengineer its supply chain. Bottlenecks in the Supply Chain The company ran one of the largest injection-molding operations in the world, with its own production sites in Denmark and Switzerland, and packing and other facilities in the Crech Republic, the US and Korea. The fully automated factory in Denmark alone had more than 800 machines. Its production people would proudly tell you that L.EGO was the largest producer of (toy) tires in the world! The factories produced a staggering 20 billion bricks per year; separate packing facilities assembled them into finished LEGO sets. The logisties flow between each factory and packing location was managed through a complex structure of multiple DCs and warehouses. "Soure; 1.1.GO annsal refort 2002 . "New products generated 75% of total sales; 45% of sales took place in the theee months before Christmas. Planning remained a constant challenge for LEGO, even after 50 years of experience molding bricks. Salcs forccasting was so inaccurate that capacity utilization was just 70 e. The company also had to manage a supply chain of over 11,000 suppliers that had grown over time as LEGO sets had hecome more claborate. with multiple combinations for the face. body and less of the main action figures - adding up to a total of 12500 SKUs in ower 100 different colon. LEGO tricu to establish itself as a just-in-time delivery company, but at a cost to itself. It accepted customer orders with immediate or next day delivery. Of these orders, 67% were for less than a full carton and only 62 en could actually he delivered "on tiane. t+ A Comples Three-Level DC Structure in Europe As Exhibit 2 shows, to be close to the customer. LEGO used four regional DCs: two in France, operated by a third-party logistics provider and serving primarily the UK and southern European markets; one is Germany for the Central and East European markets; and one in Denmark for Scandinavia and the Benelux. The last two, also the largest, were operated by LEGO and employed just over 200 people. Almost 14,000 customers received direct deliveries from these four DCk. The finished LEGO products were stored in a 30,000m2 central warchouse in Germany, operated by a third party. Products from this warehouse were delivered on demand to the four regional DCs, two dedicated assortment product lines 2 and LEGO's Shopaliome operation in Denmark as well as DCs located outside Earope. The factories in Denmark and Switzerland operated their own logintics and distribution centers, storing and consolidating goods from their own production sites as well as from the packing facility in the Crech Republic and other thirdparty suppliers. From Denmark and Switacrland, finished and complete sets were delivered to the central warehouse in Germany. Including a separate warehouse and operation for its "assortment pocks., 5 L.ECO used 11 different European logisties operatiens to manage the flow of products, with more than 60 suppliers of logistics and transport services. Shared Vrsion LEGO needed a turnaround. In 2003 and 2004, Kjeld Kirk Kristiansen, CEO and majority shareholder, brought in outsiders and some recent recruits to evecute the company's transformation. Jesper Ovesen, from Danske Bank, became the new CFO: Bali Padda, who joined LEGO in 2002, was promoted to VP Glotal The average sales forccasting errar was 4Th4. 4 Assortments af branded nan-LECO products, educational grodocts and loose L.FGO hricks. "Marketing materialk, ectail displays, value pecks, bundles, cene-time prodoch, afw SKU"k, esc. Logistics; and Jorgen Vig Knudstoep, who joined 1.EGO in 2001 as a director of strategic development, was tasked with developing a rescue plan. Vig Kinudstorp gathered a diverse group of senior exceutives io develop the stratecy and set up a "war rocm." The war rooen was decorated with process charts, performance data and other project tracking shects, where scnior manapement and specialists analyzed the company's product development, sotarcing, manufacturing and logistics process. It was here that 1.FGO's new "Shared Vision" strategic plan took shape. In October 2004. Vig Knudstorp seplaced Kirk Kristiansen as president and CFO of LEGO, recciving a clear mandate from the company's board to execule this plan. Kirk Kristiansea injected soctie more of his own cash into the group "for the last time, "but otherwise took a backseat role. Action Plan for Sarvival The first phase of Shared Vision - "Stabilize for Survival" - focused on reducing costs, eliminating debt and returning the coenpany to profitability. 1.EGO sold a 70 . share of its four L.EGOL.AND theme parks to the Blackstone Group in 2004, clearing its debt and reducing direct headcount by approximately 30%. Oeber assets were also sold or oeltsourced, sach as buildings, fand, its own mold-making factory, the Korean packing facility and the corporate jet. The first phase of Shared Vision was achieved in 2005 , a year in which L.EOO returned to profit. Sales increased also, but this was largely driven by the success of the sixth and final Star Wars'M movie: Revenee of the Sirh." The second phase - "Profit from the Core" - would focus on sustainably improving the coenpany's profitability and growth. Reducing Complexity: Breaking with the Past Egil Moller Nielsen had joined I.FGO in January 2004 as logistics strategy directot, tasked with developing a strategic turnaround plan for the global distribution process. Initially he was given a full ycar "away from the frontline" to develop a plan, but this selative period of peace was disturbed afler four months. when, LGO made him also responsable for all logistics headcount in Farope and Asia. Managing the scasonality of L.EGO jroducts would be his key challenge. Demand roughly doubled between September and November and so he had to manage almost twice the number of blue-collar workers for a short period of time. His main job would be to find a way to get the thght jroduct to the righe place, in tame something LEGO had been struggling with for a while. As Padia put it: Too moch sime wat spent finding oot where a peoduct was at any given tiene. "Total sales of Star Wars prodocts were DKk 936 millioe in 2005 . This was a Hohs increase an the grevices year. The secoed las Star Wars morie was in 2004 . "In 2005 Meller Nielsen was promoted to senior logisties director, Farve and Asia. Defining Cost Drivers and Establishing a Cost Bascline One of Meller Nielsen's first tasks was to establish a solid logistics cost baseline. It took almost four months to do so and to define key cost drivers and cost ownership. Total yearly costs were estimated at DKK 650 million, of more than 10% of sales. Transportation costs were more than half of total costs. Understanding the Real Custemer Requirements Another challenge was to convince the people in sales that any cost-cutting changes in the logistics process would not automatically lead to customer dissatisfaction or loss of business. Moller Nielven knew that be had to establish a direct communication link with LEGO's key customer base, to understand their real - not perceived - requirements. He had a questionnaire sent to the top 20 companies, representing 70 he of LEGO's total business, followed by interviews and personal visits. Meller Nielsen learned one very important thing: Most customers did not require daily or next-day deliveries. This was contrary to what he had been told by some of his colleagues. Arguments in favor of immediate delivery were used to justify higher inventory levels and having DCs close to the customer. The direct customer feedback would give Molier Nielsen more credibilify in designing the ideal process. Defining Key Objectives and Targets and Developing a High Level Strategy One of the key corporate drivers - to build a sestainable profitable platform - was to make the company more asset light. This was to be achieved through outsourcing and simplified processes. In 2004 LEGO had given its management team a farget to cut conts by 20% by the end of 2008 . To meet this objective and achieve the cost savings target, Meller Nichen proponed consolidating all logistics and distribution operations to a single central DC, managed by a thind party. This proposal was accepted by the managemeat feam at the end of 2004. For economic reasons, this central DC needed to be close to LECO'S main production facilities and largest single markets (Germany and the UK). Selecting New Partners: Glebal Tendering In carly 2005 a global tendering, process started with the company's existing logistics service providers, as well as some new ones. In total, LEGO invited 22 companies to bid on part or all of its global logintics process. The geal was to reduce its 35+ transportation companics to a maximum of 7 global supplicrs. bring all finished goods in Europe under one toof and to cut costs by DKK 130 miltion - including DKK 45 million on transportation. "I Danith krene DKK 1=60.13=99.17 "Within 16 is 18 hours' drive. "For Mailer Nietven, the focas was on distribution so cosonen in Farope and Aaia. Ia the Us and Canada, a central DC selutioe already cuissed asd was werking well. The central European IDC (EDC) would have to have an initial total capacity 11 of 51,000m2 - with an option 10 exicnd to 62,000m2 - and the provider would have to be able to manage the level of the workforce during peak and off scasons. A model created to calculate the ideal locatanon showed that Praguc in the Crech Republic was the most central place. However, a distribution center on such a scale "had never been done before" in an East European country. Moller Niclsen left the choice of final location open. cnabling him to evaluate different options. but he urged "preferred" providers to base their quotation on the assumption that the EDC would be in the Cach Republic. D1HL. won the tender. The deciding factor was that DHII. throagh its global relationship with Prologis - the world's largest developer of distribution facilities Was the only company that could quickly construct a facility of the required sire close io Prague. DHH. Exel in the Cach Republic, responsible for this BDC, had yearly revenucs in 2005 of approximatcly E30 milion (DKK 200 million). The L. ECO contract would almost double its annual revenues, so this was "a big fish" for the company. Building a central DC of this size in the Crech Republic would break new groand, not only for DHIL. but also for LEGO. The new DHH. building in Jimy was intended to be a malti-clicnt operation. with extra office space for Dtit.'s Crech opcrations. The contract with DHI. Was signed for five and a half years and was coammunicated to all I.FGO cmployecs worldwide and to thind partics on Augast 30,2005 . The contractual cost savings were considerable. Reducing the number of transportation companies 10 seven would restalt in DKK. 40 million savings per year and the consolidation of 10 operations into one another DKK. 75 million. Other Changes Impacting Distributien Also on August 30, 2005, L.EGO announced that it would outsource production from its factory in Switrerland to a contract manufacturer (CM). The same CM would also take over the management and control of LEGO's packing facility in Kladno, in the Czech Republic, which would further be expanded to meet roughly half of the total demand. The Swiss plant mainly produced L.EGO's Duplo products and employed 239 people. Production would be transferred to the CM's facility in Hungary during 2006. Other changes were also happening fast on different fronts in an attempt to reduce complexity: The number of different colors was cut by half and SKUs were reduced to 6,500 . Of course, the challenge was to reap the full benefit of these changes through excellent execution. 4i The calculatioa was based ce the assumption that a maximum space for 76.000 pallets would be requircd during peak seasons, with additional space for loading, assembly and offices. if The name changed from DAALDanras Solutions to DHH-Exel after Desasche Past World Net (ewner of DlH. \& Danzas) acquired Evel in December 2005. -7- IMD-6 6315 Building the Infrastructure Planning, Construction and 1T Changes Moller Nielsen and his team had developed a very detailed project plan, but this was tossed out of the window as soon as the team began facing the real day-to-day issues. The construction of the building in Jirny started at the end of 2005 , new transport suppliers were introduced, and system changes and transfer to a new SAP platform were in progress, enabling future electronic linkages to DHL"s warchouse system. Implementation was planned in a phased approach (refer to Exhibit 3). During 2006 , before the start of the peak season, responsibilify for the two DCs in France would be transferred to DHL in Jirny. This represented around half of the European sales volume, Goods and responsibilities from the central warchouse in Germany, the two logistics operations managed by the plants in Denmark and Switzerland, and the two Danish assembly lines would transfer the same year as weil. During 2007, the remaining two DCs in Billund and Hohenwestedt would follow, and the assortment pack facility in Billund 3 would be phased out completely. Organiration Changes Beyond the standard storage and pick services, DHL also managed the LEGO assortment packs, assembled customer value packs and prepared customized deliveries, described in the "customer brief." Having these services under one roof was unique for most large DCs, and to allow it to focus properly on each service. DHL split its organization into three parts: (1) standard orders, (2) value-add services and (3) customized orders. Not all specific customer requirements were known during 2004 and 2005 and thus could not be spelled out in the Group and DHA. that DHL. would have to be flexible in adapting to customers requirements as soon as they became known. Moller Nielsen created a new "customer logistics" team. It was his organization's direct link with the customers and responsible for reducing the complexity of customized orders, while also focusing on improving customer delivery satisfaction. The First Warning Signs: Cost Drivers or Cost Behaviors? To simplify the process of accurately allocating the total logistics costs to profit centers, LEGO used "costs per order" as the main cost driver for logistics. During the tendering process, providers had been asked to quote their prices at the order level. making it easier for LEGO to reallocate their total costs. What DHIL did not know at that time was that L.EGO was undergoing major changes in its customer " Partial trasofer would start in 2006 , with final cloware in 2007. "Information about special delivery requirensents was either not documented of not provided by the third-parfy logistics provider that managed the local DCs in France. ordering process. Large retailers, which had initially placed small daily orders, were requested to place larger orders, at least two months in advance. Most retailers were surprisingly cooperative and in favor of this changc, they were used to long lead times from other toy manufacturers, as most toy products arrived by sea from Asia. They preferred to wait for two months, knowing that the L.FO products would at least be delivered within the requested delivery date. Changes in the cost drivers also changed the behavior of some of the sales offices. With logisties costs allocated at order level, some of them saw this as a reason to shift their focus from smaller to larger retailers. Obviously, as DHL. had calculated all costs at the order level, it would lose out when the number of orders started to drop significantly. 2006 Implementation A Steep Learning Curve During the first transitions before the summer, there were mote than the assal start-up issues. The Crech DHIL. team had never managed an operation of this sire before. For starters, there were not enough trained people: We even had to seach them how to drive a fork.1ift - DHL.'s main IT system turned into a botileneck. It was not designed to handle so many different custoner delivery "rules" and also could not cope with the volume of transactions provided by L.EGO. The system ground to a halt more than once. and additional people had to be hired to produce and manually print the different customer labels and shipping instructions. Also, it took longer than expected 15 to find a big enough skilled sempocary workforce for only four or five months. Most of them had to be recruited from Ukraine, but not many spoke English, so they had to be taught how to read the information on the scanners and systems. LEGO sales teams, anticipating delays and shortages during the transition, had pushed their customers for advance orders. As a result, demand started increasing as carly as August, catching everyone "off-guard," includiag Moller Niefsen and his team. The first crises started to occur and from then on the teams were in constant firefighting mode. Soon after it became apparent that DHL. did not have the capalility to control the flow and communication with the carriers - "They were not aware that there was a truck-load waiting for 24 hours inside the warchouse" - LEGO decided to take back the management and control of the carricrs. To improve this process, it designed and implemented a new web-hased tool in less than three weeks. Misunderstandings and Cultural Issaes Cultural clashes played an important role, creating an atmosphere of mistrust between both parties. LEGO people blamed the "Crechs" for not taking enough responsibility, and the Crechs had problems with the Danes" direct approach and their constantly changing requiremetts. L.FGO then started bringing more of its own people into Jimy, something that DHIL at first perceived as "an intrusion on its own territory." Blame games would start whenever there were issues with deliveries, which were largely caused by the carriers. This situation further escalated when Moller Nielsen was briefly introduced to Leigh Pomlett, the new regional head of DHH-Excl, in Aupust 2006 . Pomlett had just come out of a meeting with his Cacch tcam, believing that every thing was going smoothly and was in good spirits. This changed abruptly when Moller Nielsen told him provocatively, "Your people have no clue how to run this warchouse." Perhaps it was blunt, but Pomlett took the criticism seriously; from then on key issues were addressed and resolved in a more constructive way and a new head of operations, from Pomlett"s old team in the UK, was transferred to Jirmy two months later. Misunderstandings 17 and disagrecracns oe the conmercial agrecment became the main otstacle to establishing a sustainable partnership. LEGO's perspective was that the contract had becn signed and it was up to DHl. so deliver as promised. In fact, frequently challenged by I.EGO on the validity of its quotation. DHL. European management coefirmed in writing in 2005 in that they were comfortable with their calculations and would deliver as promised. IA DHI.' s view, the contract Was very complex and not casy to underntand. long hours were spent arguing over the agrecment, as it started to become clear that DHI had underestimated the requirements - especially with regard to the high fluctuafioes between low and peak periods. For example, in its quotation. DHth. estimated a yearly average of 180 fulltime equivalent (FIt) employees for zo06, not really believing the projected volume provided by L.EGO. The actual averape number needed was closer to 500 FIE. DHH. was going to pay a high price for the eistra costs. which Maller Nielsen was not yet jrepared to share, given the initial cod pressure within L.EGO. Capacify Constraints In addition, the warchouse was getting full. It was supposed to be large enough to manage the total European capacity foe the next five years, so what had happened? " L.EO created the "carner rooen." I this room, togrescetatives of three different transport companies worked together. They had acces to a large moeiss showing the turnaround time of trucks being loaded and offloaded - color coded and in tral tine. "Aher the fxel acquisition, cieryone involved in the L.FCO deal bad either left DFLL or moved on. Irenically, the implcmentation was now being maned by ev-feel managers - who came secend in L.FGO's tender - and eairmal conialurts. Defl. and Exel wed to have a different vice on how cent calculations should be done. This expained some of this "lack of undernanding." In June 2006LEGO announced to employees that most of its production would be outsourced to the CMI that had already taken over the production from Switrerland and was also responsible for the packing facility in Kiadno. Production at the USbased plant would be phased out completely and relocated lo Mexico, affecting about 300 people. Production of the more technically demanding products, such as LEGO Bionicle and LEGO Technec, would stay in Billund, whereas jroduction of the more standard and high volume products would move to Hungary and the Crech Republic. Up to 900 of the 1,200 jobs in Billund would be affected. The relocation would take place between 2006 and 2010 . Related to this outsourcing, key changes were made. To mitigate the transition of production from Denmark to Hungary or the Cacch Republic, production was ramped up temporarily. Furthermore, the packaging for finished LEGO sets was changed, which decreased the number of sets that could fit on a pallet by almost 20% These changes - neither of which was communicated to logistics - created a significantly higher inventory level in terms of pallet positions, not only impacting space but also driving transport and storage costs higher. DHIL, quickly cxpanded to use the maximum of the available 62,000m2 space, but this was still not cnotgh. With the help of ProLogis, more space would ultimately be found in nine additional smaller depots in and around Jimy. The EDC had been built to store 76,000 pallets, but by November 155,000 pallets were being stored in 10 different locations. Once inventory dropped to normal levels again, Maller Nielsen estimated that space for 120,000 pallets - or almost double the size of the current EDC - would be needed. Assessing the Seale of the Problem Even with frequent delivery issues and the tracking of goods seemingly out of control, delivery delays were kept to a minimam. On average, they were limited to less than two days, but only through constant firefighting and long working hours. By November 2006 , it was clear that DHL. which expected to break even during the first year, would finish 2006 with a loss of approximately 3.5 million (DKK 25 million). Moller Nielsen knew that he could not let DHIL. pick up the whole tab and that he would ultimately have to change the cost drivers in the contract. But how would he explain these increased costs to his management? Perhaps the changes in production and consequent increase in warchouse space would create the opportunity he nceded to break this deadlock situation. Fufure Challenges The sales organization in Germany was especially critical and vocal as their local DC in Hohenwestedt, managed by the L.FGO Group and serving their customers, was next in line to be closcd down. They played a large role in trying to convince Vig Knudstorp that this was a bad idea. Vig Knudstorp in return leaned hard on Moller Nielsen and his team, who had expected more support from managerment back in Billand, but often felt let down by their "unfair" behaviot. Yes, there were many issnies related to this transition, but the expected negative customer impact had becn marginal. DHL. was losing a lot of money. It was blaming L.EGO for a large part and was secking compensation. DHL and L.EGO, despite the fact that they both wanted to make this work, did not trust each other enough and were arguing constantly. The warehouse was full and the situation of tasing nine additional depots was obviously not an efficient short-term solution. Something had to be done quickly, but what? Build a new warchouse? Where? Of what sine and what about the current lease contract? For the L.EGO Group as a whole, sales were up again, and 2006 proenised to be the most profitable year of the last decade, so the pressure for massive cost reductions was temporarily off. It was now up to Moller Nielsen to make a decision. Either he should stick to the original concept - transfer the remaining two DCs as planned during 2007 and continue to work with DHL. as its main partner, while secking a larger warchouse, Or, stop further transitions and manage the distribution through three main centers operated by DHL and the L.EGO Group in Denmark (Scandinavia \& Benelux). Germany (Central Europe) and the Crech Renublic (rest of Europe and Asia). There were other altematives be could explore, like taking over the manacement from DHL at Jirmy or finding an altemative partner, but would this really solve anything? For Moller Nielsen the answer was clear, but what would you do? Sales (Net Sales), Protieloss (Results Before Tax) and Employees (FTE) Data from arnual reports Average last 5 year DKK exchange rates: 0.17 uSs and 0.13C Source: Company information -13- IMD-6-0315 Exhibit 2 Three-level Distribution Center Strueture Eurepe 2004-2005 Manswitures ( Cutsers Legend Source: Company information