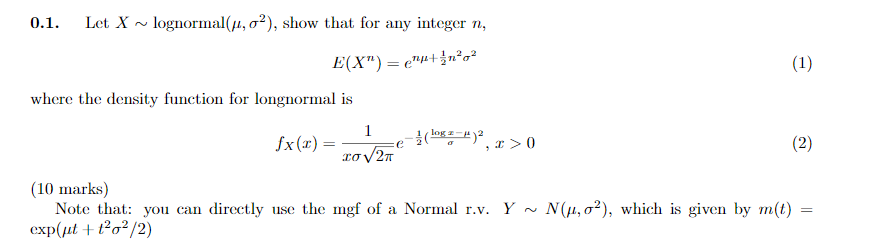

Question: This question is from Intro to stochastic processes 0.1. Let X ~ lognormal(/, o'), show that for any integer n, E(X) = nutin202 (1) where

This question is from Intro to stochastic processes

0.1. Let X ~ lognormal(/, o'), show that for any integer n, E(X") = nutin202 (1) where the density function for longnormal is fx(x) = 1 log : - 4)2 CO V 2AT e (2) (10 marks) exp(ut + 1202/2) Note that: you can directly use the mgf of a Normal r.v. Y ~ N(p, o'), which is given by m(t) =

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock