Question: This questions is based on the same data for a single period binomial model as the previous question. . The stock's price is $50. After

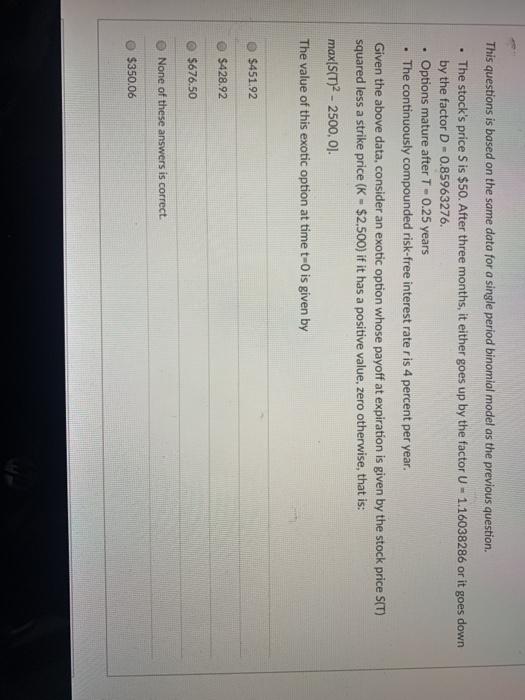

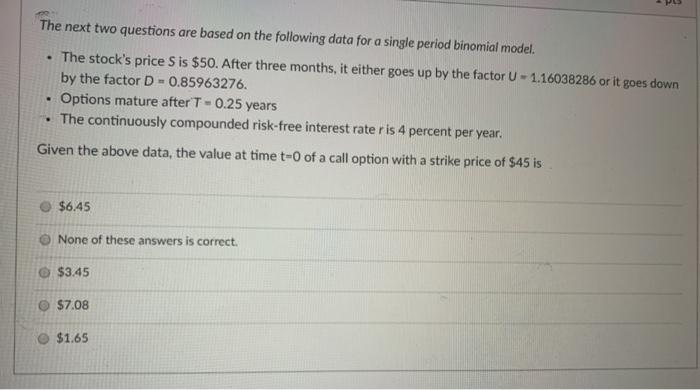

This questions is based on the same data for a single period binomial model as the previous question. . The stock's price is $50. After three months, it either goes up by the factor U - 1.16038286 or it goes down by the factor D - 0.85963276. Options mature after T-0.25 years The continuously compounded risk-free interest rate ris 4 percent per year. Given the above data, consider an exotic option whose payoff at expiration is given by the stock price SIT) squared less a strike price (K - $2,500) if it has a positive value, zero otherwise, that is: max[S(T)2 - 2500, 0. The value of this exotic option at time t-o is given by $451.92 $428.92 $676.50 None of these answers is correct. $350.06 The next two questions are based on the following data for a single period binomial model. . The stock's price S is $50. After three months, it either goes up by the factor U - 1.16038286 or it goes down by the factor D - 0.85963276. Options mature after T-0.25 years The continuously compounded risk-free interest rate ris 4 percent per year. Given the above data, the value at time t-O of a call option with a strike price of $45 is $6,45 None of these answers is correct. $3.45 $7.08 $1.65

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts