Question: This the question: Here are the guidelines/keypoints that the answer have to fulfill: could you cite appropriate references beside the ones given (ball,2006)/(Jof,1998)/(Sloan,1996)? Thanks! (c)

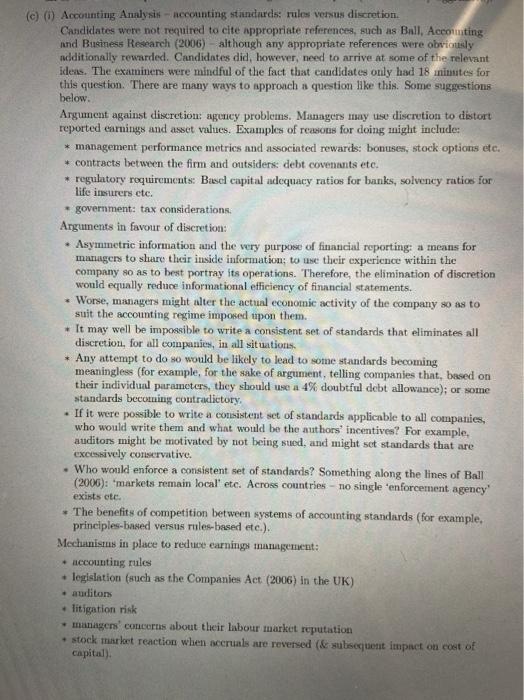

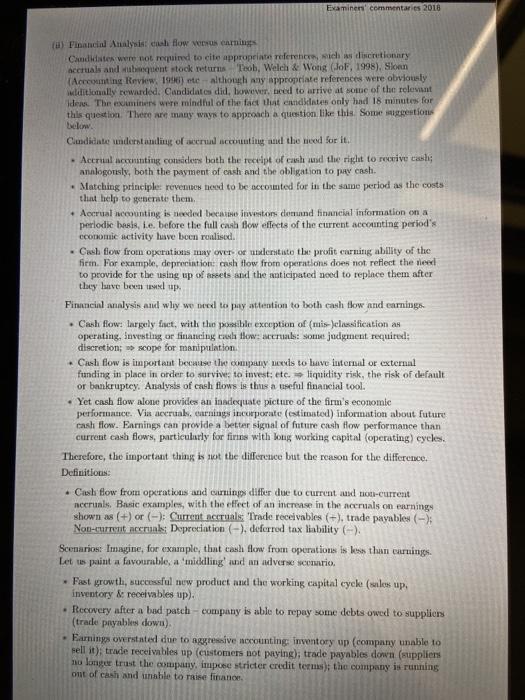

(c) Provide an analytical discussion of one of the following two questions. Either: (i) Would it be possible to the improve comparability of financial statements within an industry, and hence to improve the informational efficiency of equity markets, by reducing management discretion in financial reporting? Or: (ii) When undertaking financial analysis, should we pay more attention to cash flow information or to earnings information? (10 marks) (0) (0) Accounting Analysis - accounting standards: rules versus discretion Candidates were not required to cite appropriate references, such as Ball, Accounting and Business Research (2006) although any appropriate references were obviously additionally rewarded. Candidates did, however, need to arrive at some of the relevant idens. The examiners were mindful of the fact that candidates only had 18 inimites for this question. There are many ways to approach a question like this. Some suggestions below. Argument against discretion: agency problems. Managers may use discretion to distort reported earnings and asset values. Examples of reasons for doing Inight include: * management performance metrics and associated rewards: bonuses, stock options etc. * contracts between the firm and outsiders: debt covenants etc. * regulatory roquirements: Basel capital adequacy ratios for banks, solvency ratios for life insurers etc. * government: tax considerations. Arguments in favour of discretion: Asymmetric information and the very purpose of financial reporting: a means for managers to share their inside information; to use their experience within the company so as to best portray its operations. Therefore, the elimination of discretion would equally reduce informational efficiency of financial statements. Worse, managers might alter the actual economic activity of the company so as to suit the accounting regime imposed upon them. It may well be impossible to write a consistent set of standards that eliminates all discretion, for all companies, in all situations. Any attempt to do so would be likely to lead to some standards becoming meaningless (for example, for the sake of argument, telling companies that, based on their individual parameters, they should use a 4% doubtful debt allowance); or some standards becoming contradictory If it were possible to write a consistent set of standards applicable to all companies, who would write them and what would be the authors' incentives? For example, auditors might be motivated by not being sued, and might set standards that are excessively conservative. Who would enforce a consistent set of standards? Something along the lines of Ball (2006): 'markets remain local etc. Across countries - To single enforcement agency exists cte. The benefits of competition between systems of accounting standards (for example, principles-based versus rules-based etc.). Mechanisms in place to reduce earningsmanagement: accounting rules legislation (such as the Companies Act (2006) in the UK) auditors litigation risk * managers concerns about their labour market reputation stock market reaction when accruals are reversed (& subsequent impact on cost of capital) Emines commentaries 2016 (a) Financial Analysis cal flow venserning Candidates were not mined to cite appropriate references ich discretionary accruals and equent stock returns Toob, Welch & Wong (JoF, 1998), Sloan (Accounting Review, 1996) tealthough any appropriate references were obviously wilditionally rewarded. Candidates did, however, teed to arrive at some of the relevant Idens. The miners were mindful of the fact that candidates only had 18 minutes for this question. There are many ways to approach a question like this. Some suggestions below Cimdidate understanding of meer accounting and the need for it. Acerul aceinting considers both the receipt of cash and the right to receive cash analogously, both the payment of cash and the obligation to pray cash. Matching principles revenues need to be accounted for in the same period as the costs that help to generate them, + Accrual counting is needed became investor comund financial information on a periodic basis, i.e. before the full cash flow effects of the current accounting period's conomic activity have been realised. . Cash flow from operations may over or utlerstate the profit earning ability of the firm. For example, depreciation cash flow from operations does not reflect the need to provide for the using up of assets and the anticipated need to replace them after they love been tol up. Financial analysis and why we need to pay attention to both cash flow and earnings Cash flow: largely fact, with the possible exception of (mis)lassification as operating, Suvesting or financing coola flow accrual: some judgment required: discretion scope for manipulation Cash flow is important because the company needs to have internal or external funding in place in order to survive: to invest: etc. liquidity risk, the risk of default or bankruptey. Analysis of cash flows is thus a useful financial tool. Yet cash flow alone provides an inadequate picture of the firm's economie performance. Vir accruals, earnings in deporte (estimated) information about future cash flow. Earnings can provide a better signal of future cash flow performance than cash flows, particularly for firins with long working capital operating) cycles. Therefore, the important thing is not the difference but the reason for the difference. Definition Cash flow from operations and cruin differ due to current and non-current neeruns. Basic examples, with the effect of an increase in the accruals on earnings shown as (+) or (-): Current actuals Trade receivables (+), trade payables (-); Nou-current accruals: Depreciation (-). deferred tax liability ) Scenarios Imagine, for example, that cash flow from operations is less than cruing Let us paint a favourable, a midklling and an adverse scuri. Fast growth, successful new product and the working capital cycle (suilos up, inventory & receivables up). Recovery after a bad patch - company is able to repay some debts owed to suppliers (trade payables down) - Earnings overstated due to aggressive arounting inventory up (company unable to sell it) trade receivables up (customers not paying); trade payables down (suppliers no longer trust the company, impobe stricter credit ters) the company is running ont of cash and unable to raise finance curre

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts