Question: this the whole question. give methe solution for question for question 3 and 4 [Table 1] Semi-annually compounded yield curve Maturity (year) 0.50 1.00 1.50

this the whole question.

give methe solution for question for question 3 and 4

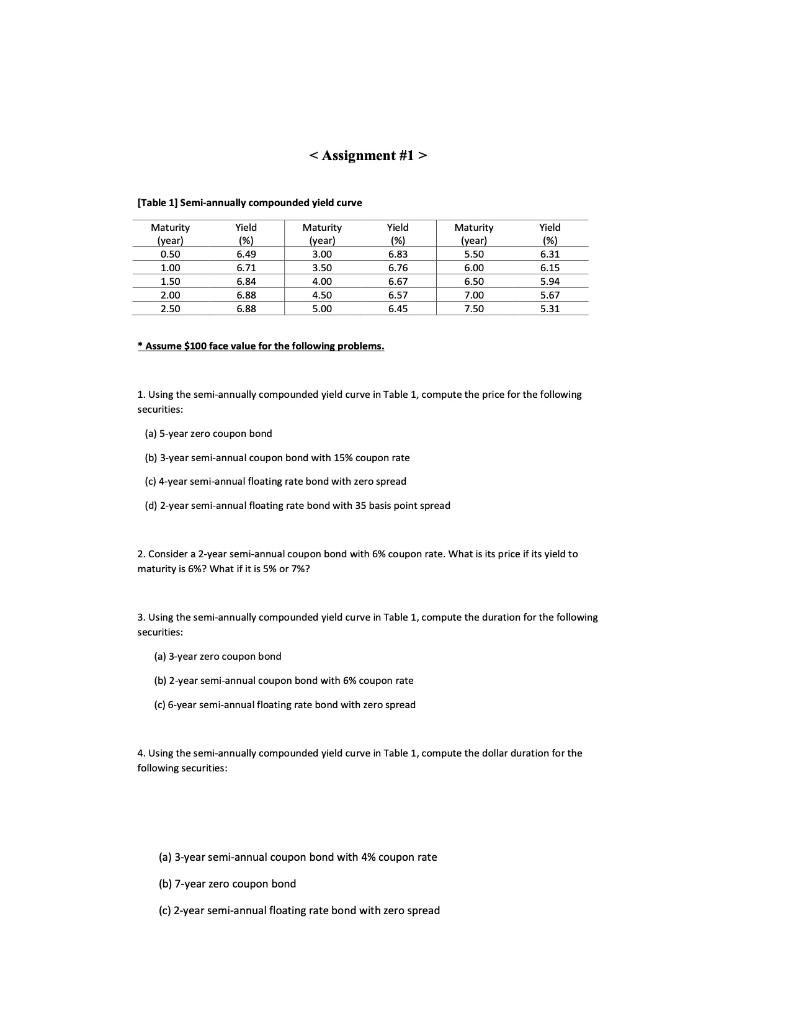

[Table 1] Semi-annually compounded yield curve Maturity (year) 0.50 1.00 1.50 2.00 2.50 Yield (%) 6.49 6.71 6.84 6.88 6.88 Maturity (year) 3.00 3.50 4.00 4.50 5.00 Yield (%) 6.83 6.76 6.67 6.57 6.45 Maturity [year) 5.50 6.00 6.50 7.00 7.50 Yield (%) 6.31 6.15 5.94 5.67 5.31 Assume $100 face value for the following problems. 1. Using the semi-annually compounded yield curve in Table 1, compute the price for the following securities: (a) 5-year zero coupon bond (b) 3-year semi-annual coupon bond with 15% coupon rate (c) 4-year semi-annual floating rate bond with zero spread (d) 2-year semi-annual floating rate bond with 35 basis point spread 2. Consider a 2-year semi-annual coupon bond with 6% coupon rate. What is its price if its yield to a % . maturity is 6%? What if it is 5% or 7%? 3. Using the semi-annually compounded yield curve in Table 1, compute the duration for the following securities: (a) 3-year zero coupon bond b) 2 (b) 2-year semi-annual coupon bond with 6% coupon rate (c) 6-year semi-annual floating rate bond with zero spread 4. Using the semi-annually compounded yield curve in Table 1, compute the dollar duration for the following securities: (a) 3-year semi-annual coupon bond with 4% coupon rate (b) 7-year zero coupon bond (7 (c) 2-year semi-annual floating rate bond with zero spread [Table 1] Semi-annually compounded yield curve Maturity (year) 0.50 1.00 1.50 2.00 2.50 Yield (%) 6.49 6.71 6.84 6.88 6.88 Maturity (year) 3.00 3.50 4.00 4.50 5.00 Yield (%) 6.83 6.76 6.67 6.57 6.45 Maturity [year) 5.50 6.00 6.50 7.00 7.50 Yield (%) 6.31 6.15 5.94 5.67 5.31 Assume $100 face value for the following problems. 1. Using the semi-annually compounded yield curve in Table 1, compute the price for the following securities: (a) 5-year zero coupon bond (b) 3-year semi-annual coupon bond with 15% coupon rate (c) 4-year semi-annual floating rate bond with zero spread (d) 2-year semi-annual floating rate bond with 35 basis point spread 2. Consider a 2-year semi-annual coupon bond with 6% coupon rate. What is its price if its yield to a % . maturity is 6%? What if it is 5% or 7%? 3. Using the semi-annually compounded yield curve in Table 1, compute the duration for the following securities: (a) 3-year zero coupon bond b) 2 (b) 2-year semi-annual coupon bond with 6% coupon rate (c) 6-year semi-annual floating rate bond with zero spread 4. Using the semi-annually compounded yield curve in Table 1, compute the dollar duration for the following securities: (a) 3-year semi-annual coupon bond with 4% coupon rate (b) 7-year zero coupon bond (7 (c) 2-year semi-annual floating rate bond with zero spread

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts