Question: Thx for helping! Problem 5. (10pts) Let S = 70, K = 68, r = 0.05, 0 = 0.3,8 = 0.1 = 0.5, and pricing

Thx for helping!

Thx for helping!

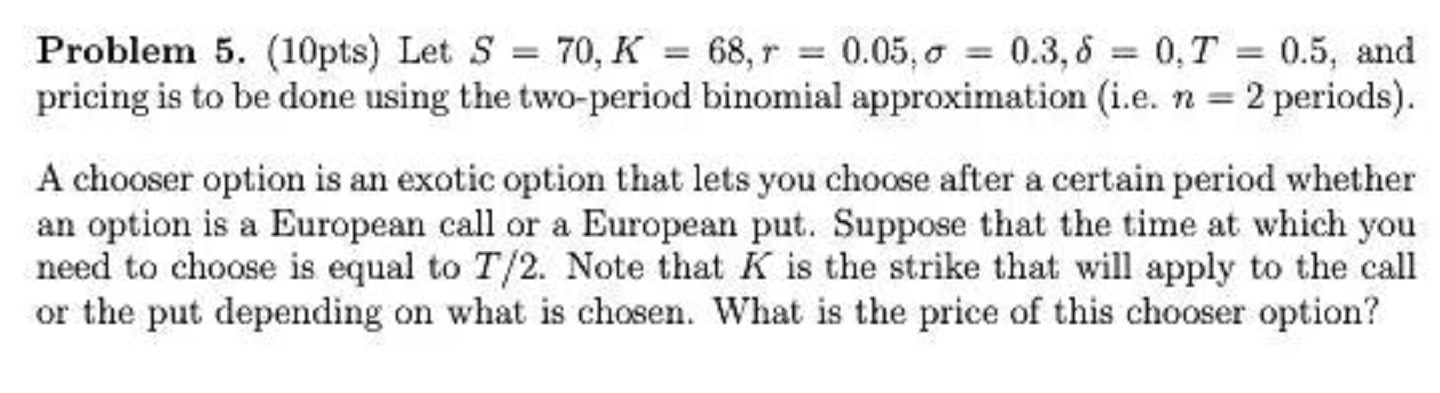

Problem 5. (10pts) Let S = 70, K = 68, r = 0.05, 0 = 0.3,8 = 0.1 = 0.5, and pricing is to be done using the two-period binomial approximation (i.e. n = 2 periods). A chooser option is an exotic option that lets you choose after a certain period whether an option is a European call or a European put. Suppose that the time at which you need to choose is equal to T/2. Note that K is the strike that will apply to the call or the put depending on what is chosen. What is the price of this chooser option? Problem 5. (10pts) Let S = 70, K = 68, r = 0.05, 0 = 0.3,8 = 0.1 = 0.5, and pricing is to be done using the two-period binomial approximation (i.e. n = 2 periods). A chooser option is an exotic option that lets you choose after a certain period whether an option is a European call or a European put. Suppose that the time at which you need to choose is equal to T/2. Note that K is the strike that will apply to the call or the put depending on what is chosen. What is the price of this chooser option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts