Question: Time Series 4. (10 marks) For a process { Y}, the auto-covariance generating function is given by gy (2) = _ 7(j)2, J=-00 where v(j)

Time Series

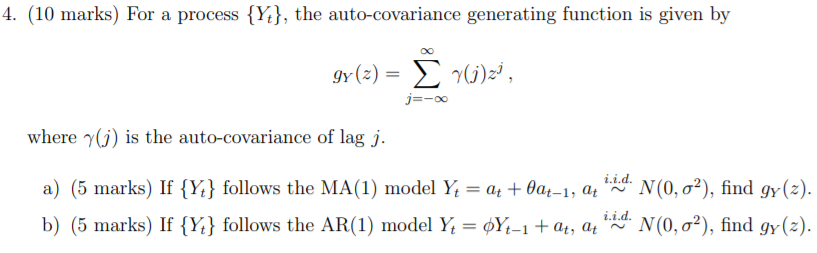

4. (10 marks) For a process { Y}, the auto-covariance generating function is given by gy (2) = _ 7(j)2, J=-00 where v(j) is the auto-covariance of lag j. a) (5 marks) If {Y} follows the MA(1) model Yt = at + 0at-1, at N(0, o?), find gy(z). b) (5 marks) If {Y} follows the AR(1) model Yt = oft-1 + at, at ~ N(0, o?), find gy(z)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock