Question: TO HAND IN Some practice with It's formula Let (Bt, t > 0) be a standard Brownian motion. For each of the processes (Xt,

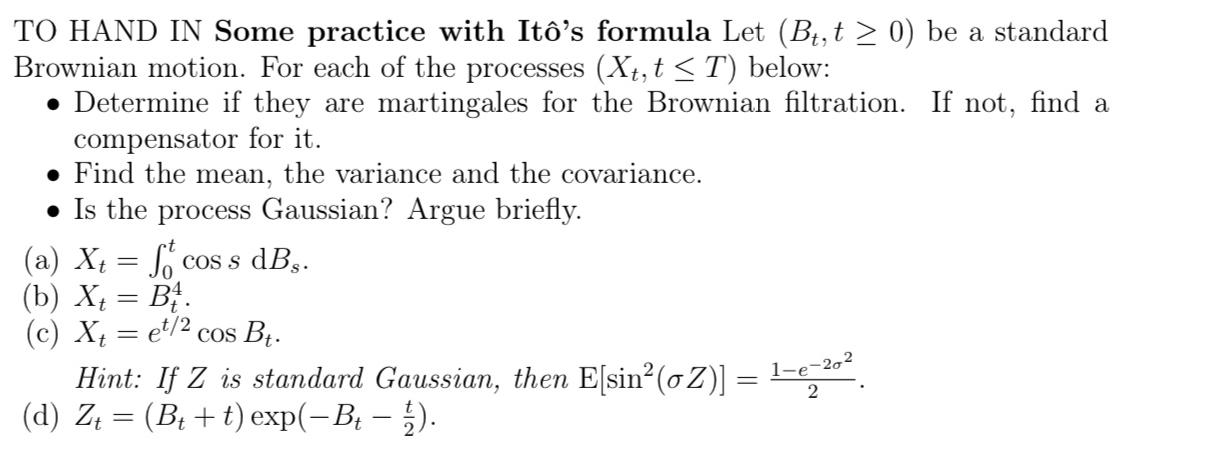

TO HAND IN Some practice with It's formula Let (Bt, t > 0) be a standard Brownian motion. For each of the processes (Xt, tT) below: Determine if they are martingales for the Brownian filtration. If not, find a compensator for it. Find the mean, the variance and the covariance. Is the process Gaussian? Argue briefly. (a) X = ft cos s dB. (b) X = B. (c) Xt=et/2 cos Bt. Hint: If Z is standard Gaussian, then E[sin (Z)] = 1-e-202 (d) Zt = (B +t) exp(B ). 2

Step by Step Solution

★★★★★

3.52 Rating (155 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock