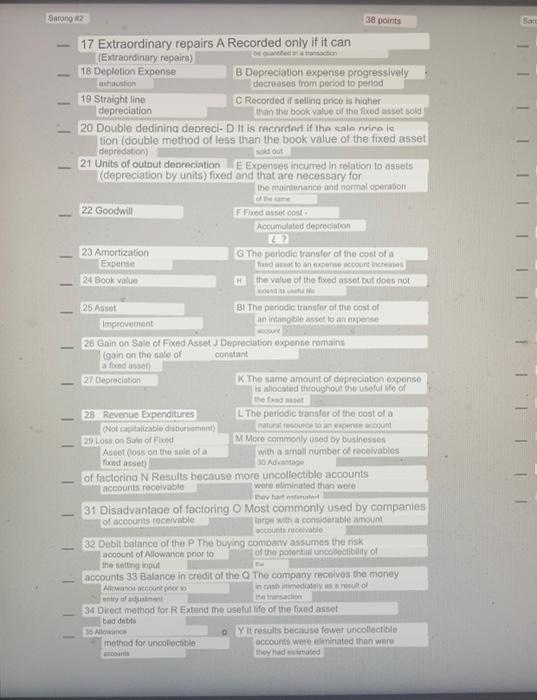

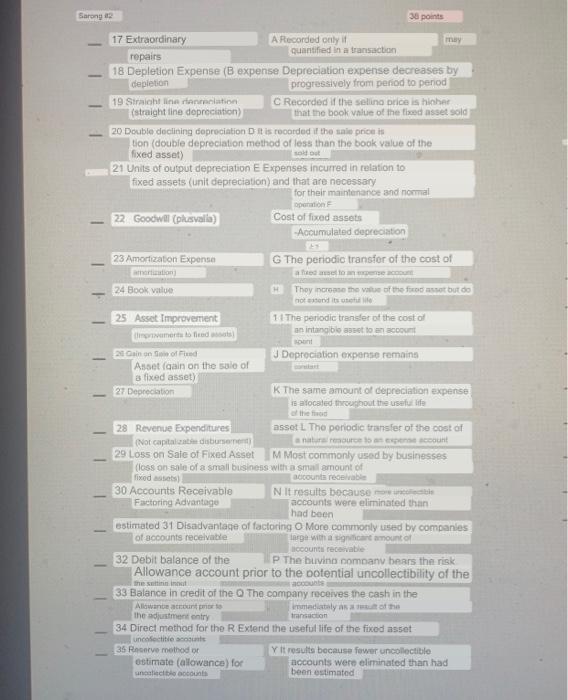

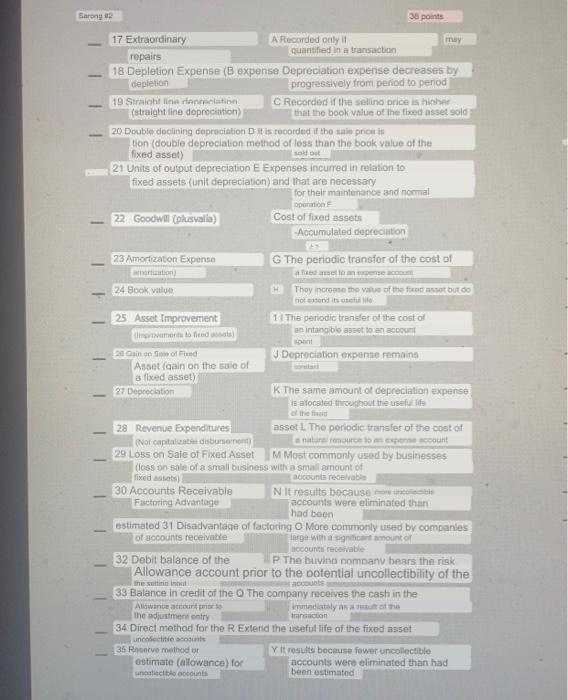

Question: to pair up colums Sarong 2 ||||||||||||| 38 points 17 Extraordinary repairs A Recorded only if it can (Extraordinary repairs) 18 Depletion Expense B Depreciation

Sarong 2 ||||||||||||| 38 points 17 Extraordinary repairs A Recorded only if it can (Extraordinary repairs) 18 Depletion Expense B Depreciation expense progressively decreases from period to period exhaustion 19 Straight line C Recorded if selling price is higher depreciation than the book value of the fixed asset sold 20 Double dedining depreci- D It is recorded if the sale price is tion (double method of less than the book value of the fixed asset sold out depredation) 21 Units of output depreciation E Expenses incurred in relation to assets (depreciation by units) fixed and that are necessary for the maintenance and normal operation 22 Goodwill FFixed asset cost- Accumulated depreciation 82 23 Amortization Expense G The periodic transfer of the cost of a fixed asset to an expense account increases 24 Book value the value of the fixed asset but does not 25 Asset BI The periodic transfer of the cost of an intangible asset to an expense Improvement WOODF 26 Gain on Sale of Fixed Asset J Depreciation expense remains (gain on the sale of constant fixed asset) 27 Depreciation K The same amount of depreciation expense is allocated throughout the useful life of the Exed asset 28 Revenue Expenditures L The periodic transfer of the cost of a natural resource to an expense account (Not capitalizable disbursement) 29 Loss on Sale of Fixed Asset (loss on the sale of a fixed asset) M More commonly used by businesses with a small number of receivables 30 Advantage of factorina N Results because more uncollectible accounts accounts receivable were eliminated than were they hart estimated 31 Disadvantage of factoring O Most commonly used by companies of accounts receivable targe with a considerable amount accounts receivable company assumes the risk 32 Debit balance of the P The buying account of Allowance prior to of the potential uncoboctibility of the setting input accounts 33 Balance in credit of the Q The company receives the money Allowano account prior to in cash immediately as a result of entry of adjustment the transaction 34 Direct method for R Extend the useful life of the fixed asset bad debts 35 Allowance oY It results because fewer uncollectible method for uncollectible accounts were eliminated than were they had estimated 3111|||||| Sarong 2 38 points 17 Extraordinary A Recorded only if may quantified in a transaction repairs 18 Depletion Expense (B expense Depreciation expense decreases by depletion progressively from period to period 19 Straight line riantelation C Recorded if the selling price is hihet (straight line depreciation) that the book value of the fixed asset sold 20 Double declining depreciation Dit is recorded if the uniw price is tion (double depreciation method of less than the book value of the fixed asset) 21 Units of output depreciation E Expenses incurred in relation to fixed assets (unit depreciation) and that are necessary for their maintenance and normal Donation 22 Goodwill (plusvalia) Cost of fixed assets Accumulated depreciation 1 TL 11 II III 23 Amortization Expense The periodic transfer of the cost of antion af stone 24 Book Value They increase the value of the front but do otterdit 25 Asset Improvement il This periodic transfer of the cost of mert to find an intangible asset to com 20 Gain one of Depreciation expense remains Asset gain on the sale of a fixed asset) 27 Depreciation K The same amount of depreciation expense is afocaled throughout the useful life the two 28 Revenue Expenditures asset L The periodic transfer of the cost of (Not capital disbursement natur aut scount 29 Loss on Sale of Fixed Asset M Most commonly used by businesses (loss on sale of a small business with a small amount of fixed assets) accounts receivable 30 Accounts Receivable Nit results because Factoring Advantage accounts were eliminated than had been estimated 31 Disadvantage of factoring o More commonly used by companies of accounts receivable nga with a significant amount of lccounts receivable 32 Debit balance of the P The buving company bears the risk Allowance account prior to the potential uncollectibility of the the stat 33 Balance in credit of the The company receives the cash in the Allowance account mediately to the the adjustment entry transaction 34 Direct method for the R Extend the useful life of the fixed asset uncoctite 35 Receive method or Yit results because fewer uncollectible estimate (allowance) for accounts were eliminated than had unable tout been estimated Sarong #2 - TIIIIII 38 points may 17 Extraordinary A Recorded only if quantified in a transaction. repairs 18 Depletion Expense (B expense Depreciation expense decreases by depletion progressively from period to period 19 Straight line danreciation C Recorded if the selling price is higher (straight line depreciation) that the book value of the fixed asset sold 20 Double declining depreciation D it is recorded if the sale price is tion (double depreciation method of less than the book value of the fixed asset) sold out 21 Units of output depreciation E Expenses incurred in relation to fixed assets (unit depreciation) and that are necessary for their maintenance and normal operation F 22 Goodwill (plusvalla) Cost of fixed assets -Accumulated depreciation 23 Amortization Expense amortization) G The periodic transfer of the cost of a fixed asset to an expense account 24 Book value HThey increase the value of the fixed asset but do not extend its useful life 11 The periodic transfer of the cost of 25 Asset Improvement (Improvements to fired assots) an intangible asset to an account spent J Depreciation expense remains 20 Gain on Sale of Fixed Asset (gain on the sale of a fixed asset) 27 Depreciation K The same amount of depreciation expense is allocated throughout the useful life of the food 28 Revenue Expenditures asset L The periodic transfer of the cost of a natural resource to an expense account (Not capitalizabile disbursement) 29 Loss on Sale of Fixed Asset M Most commonly used by businesses (loss on sale of a small business with a small amount of fixed assets) accounts receivable 30 Accounts Receivable Factoring Advantage N It results because nobis accounts were eliminated than had been estimated 31 Disadvantage of factoring O More commonly used by companies of accounts receivable large with a significant amount of accounts receivable 32 Debit balance of the P The buving company bears the risk Allowance account prior to the potential uncollectibility of the the setting incuti accounts 33 Balance in credit of the Q The company receives the cash in the Allowance account prior to immediately as a result of the transaction the adjustment entry 34 Direct method for the R Extend the useful life of the fixed asset uncofectitie accounts 35 Reserve method or estimate (allowance) for uncollectible accounts Y It results because fewer uncollectible accounts were eliminated than had been estimated Sarong 2 ||||||||||||| 38 points 17 Extraordinary repairs A Recorded only if it can (Extraordinary repairs) 18 Depletion Expense B Depreciation expense progressively decreases from period to period exhaustion 19 Straight line C Recorded if selling price is higher depreciation than the book value of the fixed asset sold 20 Double dedining depreci- D It is recorded if the sale price is tion (double method of less than the book value of the fixed asset sold out depredation) 21 Units of output depreciation E Expenses incurred in relation to assets (depreciation by units) fixed and that are necessary for the maintenance and normal operation 22 Goodwill FFixed asset cost- Accumulated depreciation 82 23 Amortization Expense G The periodic transfer of the cost of a fixed asset to an expense account increases 24 Book value the value of the fixed asset but does not 25 Asset BI The periodic transfer of the cost of an intangible asset to an expense Improvement WOODF 26 Gain on Sale of Fixed Asset J Depreciation expense remains (gain on the sale of constant fixed asset) 27 Depreciation K The same amount of depreciation expense is allocated throughout the useful life of the Exed asset 28 Revenue Expenditures L The periodic transfer of the cost of a natural resource to an expense account (Not capitalizable disbursement) 29 Loss on Sale of Fixed Asset (loss on the sale of a fixed asset) M More commonly used by businesses with a small number of receivables 30 Advantage of factorina N Results because more uncollectible accounts accounts receivable were eliminated than were they hart estimated 31 Disadvantage of factoring O Most commonly used by companies of accounts receivable targe with a considerable amount accounts receivable company assumes the risk 32 Debit balance of the P The buying account of Allowance prior to of the potential uncoboctibility of the setting input accounts 33 Balance in credit of the Q The company receives the money Allowano account prior to in cash immediately as a result of entry of adjustment the transaction 34 Direct method for R Extend the useful life of the fixed asset bad debts 35 Allowance oY It results because fewer uncollectible method for uncollectible accounts were eliminated than were they had estimated 3111|||||| Sarong 2 38 points 17 Extraordinary A Recorded only if may quantified in a transaction repairs 18 Depletion Expense (B expense Depreciation expense decreases by depletion progressively from period to period 19 Straight line riantelation C Recorded if the selling price is hihet (straight line depreciation) that the book value of the fixed asset sold 20 Double declining depreciation Dit is recorded if the uniw price is tion (double depreciation method of less than the book value of the fixed asset) 21 Units of output depreciation E Expenses incurred in relation to fixed assets (unit depreciation) and that are necessary for their maintenance and normal Donation 22 Goodwill (plusvalia) Cost of fixed assets Accumulated depreciation 1 TL 11 II III 23 Amortization Expense The periodic transfer of the cost of antion af stone 24 Book Value They increase the value of the front but do otterdit 25 Asset Improvement il This periodic transfer of the cost of mert to find an intangible asset to com 20 Gain one of Depreciation expense remains Asset gain on the sale of a fixed asset) 27 Depreciation K The same amount of depreciation expense is afocaled throughout the useful life the two 28 Revenue Expenditures asset L The periodic transfer of the cost of (Not capital disbursement natur aut scount 29 Loss on Sale of Fixed Asset M Most commonly used by businesses (loss on sale of a small business with a small amount of fixed assets) accounts receivable 30 Accounts Receivable Nit results because Factoring Advantage accounts were eliminated than had been estimated 31 Disadvantage of factoring o More commonly used by companies of accounts receivable nga with a significant amount of lccounts receivable 32 Debit balance of the P The buving company bears the risk Allowance account prior to the potential uncollectibility of the the stat 33 Balance in credit of the The company receives the cash in the Allowance account mediately to the the adjustment entry transaction 34 Direct method for the R Extend the useful life of the fixed asset uncoctite 35 Receive method or Yit results because fewer uncollectible estimate (allowance) for accounts were eliminated than had unable tout been estimated Sarong #2 - TIIIIII 38 points may 17 Extraordinary A Recorded only if quantified in a transaction. repairs 18 Depletion Expense (B expense Depreciation expense decreases by depletion progressively from period to period 19 Straight line danreciation C Recorded if the selling price is higher (straight line depreciation) that the book value of the fixed asset sold 20 Double declining depreciation D it is recorded if the sale price is tion (double depreciation method of less than the book value of the fixed asset) sold out 21 Units of output depreciation E Expenses incurred in relation to fixed assets (unit depreciation) and that are necessary for their maintenance and normal operation F 22 Goodwill (plusvalla) Cost of fixed assets -Accumulated depreciation 23 Amortization Expense amortization) G The periodic transfer of the cost of a fixed asset to an expense account 24 Book value HThey increase the value of the fixed asset but do not extend its useful life 11 The periodic transfer of the cost of 25 Asset Improvement (Improvements to fired assots) an intangible asset to an account spent J Depreciation expense remains 20 Gain on Sale of Fixed Asset (gain on the sale of a fixed asset) 27 Depreciation K The same amount of depreciation expense is allocated throughout the useful life of the food 28 Revenue Expenditures asset L The periodic transfer of the cost of a natural resource to an expense account (Not capitalizabile disbursement) 29 Loss on Sale of Fixed Asset M Most commonly used by businesses (loss on sale of a small business with a small amount of fixed assets) accounts receivable 30 Accounts Receivable Factoring Advantage N It results because nobis accounts were eliminated than had been estimated 31 Disadvantage of factoring O More commonly used by companies of accounts receivable large with a significant amount of accounts receivable 32 Debit balance of the P The buving company bears the risk Allowance account prior to the potential uncollectibility of the the setting incuti accounts 33 Balance in credit of the Q The company receives the cash in the Allowance account prior to immediately as a result of the transaction the adjustment entry 34 Direct method for the R Extend the useful life of the fixed asset uncofectitie accounts 35 Reserve method or estimate (allowance) for uncollectible accounts Y It results because fewer uncollectible accounts were eliminated than had been estimated

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts