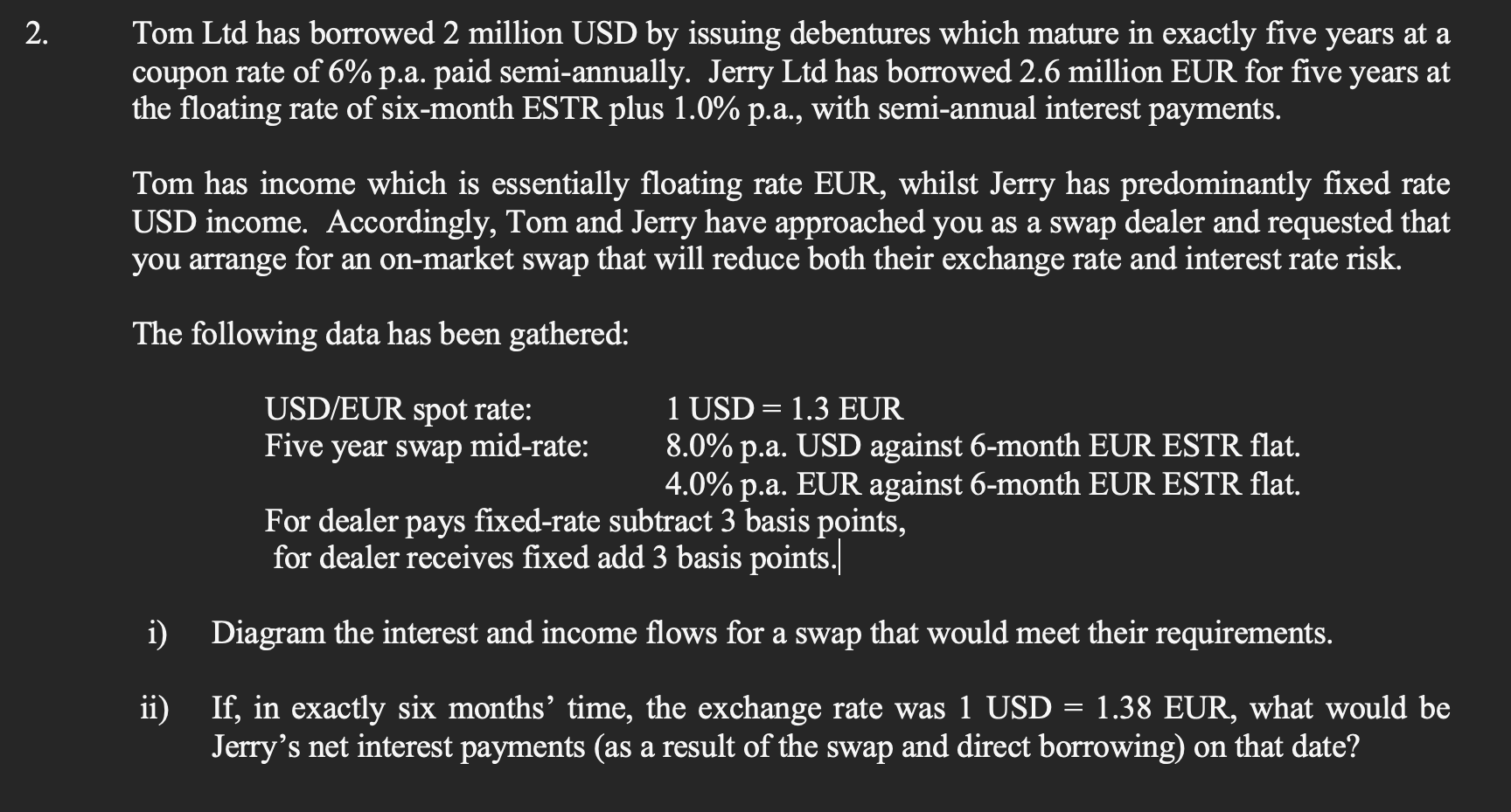

Question: Tom Ltd has borrowed 2 million USD by issuing debentures which mature in exactly five years at a coupon rate of 6 % p .

Tom Ltd has borrowed million USD by issuing debentures which mature in exactly five years at a

coupon rate of pa paid semiannually. Jerry Ltd has borrowed million EUR for five years at

the floating rate of sixmonth ESTR plus pa with semiannual interest payments.

Tom has income which is essentially floating rate EUR, whilst Jerry has predominantly fixed rate

USD income. Accordingly, Tom and Jerry have approached you as a swap dealer and requested that

you arrange for an onmarket swap that will reduce both their exchange rate and interest rate risk.

The following data has been gathered:

USDEUR spot rate:

Five year swap midrate:

USD EUR

pa USD against month EUR ESTR flat.

pa EUR against month EUR ESTR flat.

For dealer pays fixedrate subtract basis points,

for dealer receives fixed add basis points.

i Diagram the interest and income flows for a swap that would meet their requirements.

ii If in exactly six months' time, the exchange rate was USD EUR, what would be

Jerry's net interest payments as a result of the swap and direct borrowing on that date?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock