Question: TOPIC: Financial Time Series (Statistics) *PLEASE show all work/steps and fully explain* 5. (10 pts) Suppose that we observe n 100 observations from a stationary

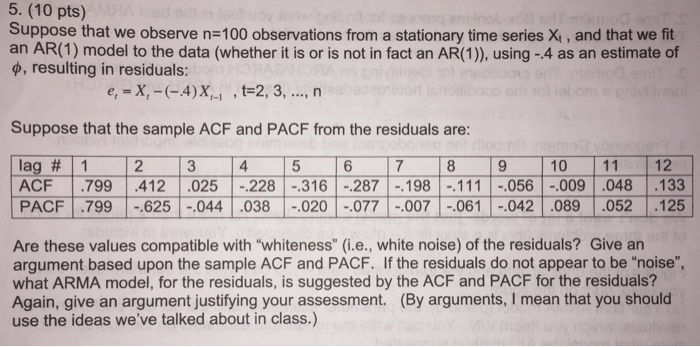

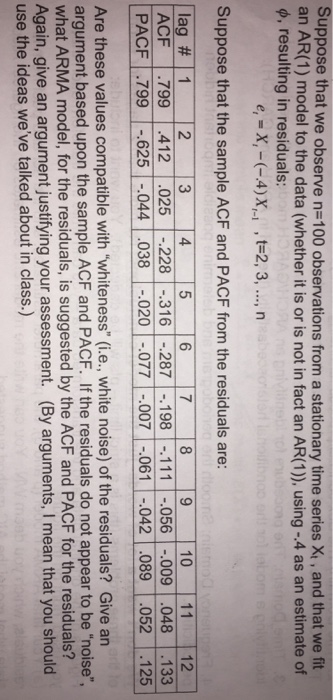

5. (10 pts) Suppose that we observe n 100 observations from a stationary time series X and that we fit an AR(1) model to the data (whether it is or is not in fact an AR(1)), using 4 as an estimate of p, resulting in residuals: e, X, -(-4)X t-2, 3 n t-1 Suppose that the sample ACF and PACF from the residuals are: lag 1 2 3 4 5 6 7 8 9 10 11 12 ACF .799 .412 .025 228 316 -.287 -198 -111 -.056 -.009 .048 .133 PACF .799 -625 -044 .038 020 -.077 -.007 061 042 .089 .052 .125 Are these values compatible with "whiteness" (i.e., white noise) of the residuals? Give an argument based upon the sample ACF and PACF. If the residuals do not appear to be "noise" what ARMA model, for the residuals, is suggested by the ACF and PACF for the residuals? Again, give an argument justifying your assessment. (By arguments, l mean that you should use the ideas we've talked about in class.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts