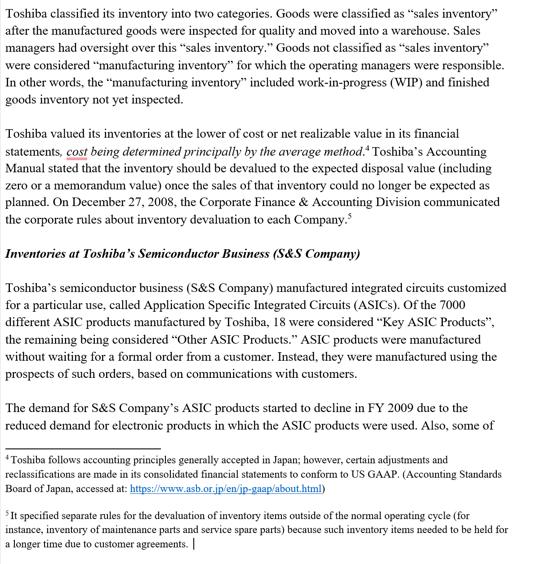

Toshiba classified its inventory into two categories. Goods were classified as sales inventory after the manufactured...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

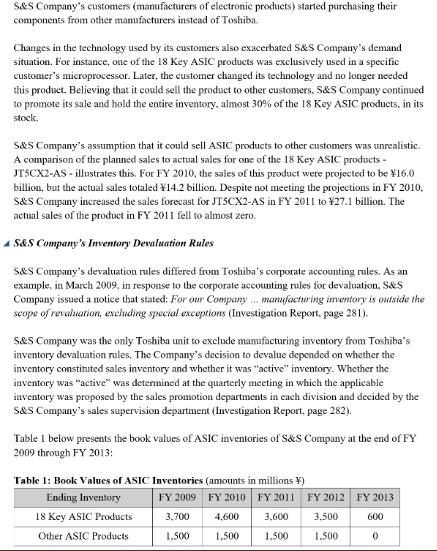

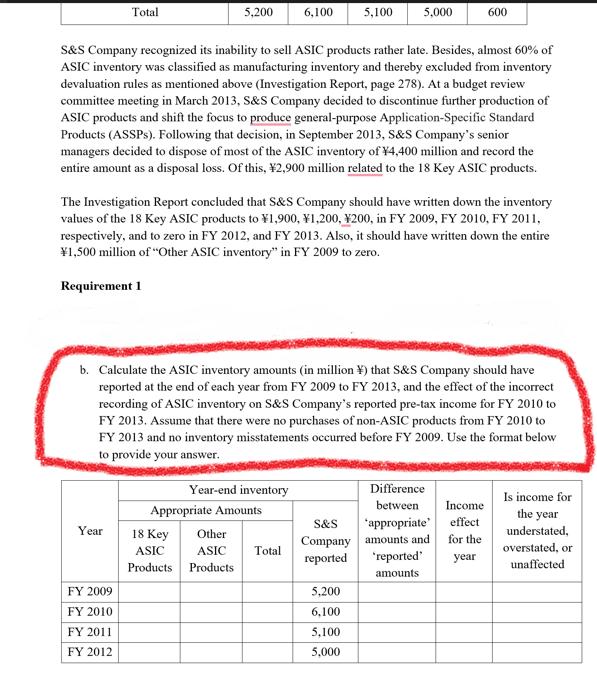

Toshiba classified its inventory into two categories. Goods were classified as "sales inventory" after the manufactured goods were inspected for quality and moved into a warehouse. Sales managers had oversight over this "sales inventory." Goods not classified as "sales inventory" were considered "manufacturing inventory" for which the operating managers were responsible. In other words, the "manufacturing inventory" included work-in-progress (WIP) and finished goods inventory not yet inspected. Toshiba valued its inventories at the lower of cost or net realizable value in its financial statements, cost being determined principally by the average method.* Toshiba's Accounting Manual stated that the inventory should be devalued to the expected disposal value (including zero or a memorandum value) once the sales of that inventory could no longer be expected as planned. On December 27, 2008, the Corporate Finance & Accounting Division communicated the corporate rules about inventory devaluation to each Company. Inventories at Toshiba's Semiconductor Business (S&S Company) Toshiba's semiconductor business (S&S Company) manufactured integrated circuits customized for a particular use, called Application Specific Integrated Circuits (ASICs). Of the 7000 different ASIC products manufactured by Toshiba, 18 were considered "Key ASIC Products", the remaining being considered "Other ASIC Products." ASIC products were manufactured without waiting for a formal order from a customer. Instead, they were manufactured using the prospects of such orders, based on communications with customers. The demand for S&S Company's ASIC products started to decline in FY 2009 due to the reduced demand for electronic products in which the ASIC products were used. Also, some of *Toshiba follows accounting principles generally accepted in Japan; however, certain adjustments and reclassifications are made in its consolidated financial statements to conform to US GAAP. (Accounting Standards Board of Japan, accessed at: https://www.asb.or.jp/en/ip-gaap/about.html) It specified separate rules for the devaluation of inventory items outside of the normal operating cycle (for instance, inventory of maintenance parts and service spare parts) because such inventory items needed to be held for a longer time due to customer agreements. | S&S Company's customers (manufacturers of electronic products) started purchasing their components from other manufacturers instead of Toshiba. Changes in the technology used by its customers also exacerbated S&S Company's demand situation. For instance, one of the 18 Key ASIC products was exclusively used in a specific customer's microprocessor. Later, the customer changed its technology and no longer needed this product. Believing that it could sell the product to other customers, S&S Company continued to promote its sale and hold the entire inventory, almost 30% of the 18 Key ASIC products, in its stock. S&S Company's assumption that it could sell ASIC products to other customers was unrealistic. A comparison of the planned sales to actual sales for one of the 18 Key ASIC products - JTSCX2-AS - illustrates this. For FY 2010, the sales of this product were projected to be ¥16.0 billion, but the actual sales totaled ¥14.2 billion. Despite not meeting the projections in FY 2010. S&S Company increased the sales forecast for JT5CX2-AS in FY 2011 to 27.1 billion. The actual sales of the product in FY 2011 fell to almost zero. 4 S&S Company's Inventory Devaluation Rules S&S Company's devaluation rules differed from Toshiba's corporate accounting rules. As an example, in March 2009, in response to the corporate accounting rules for devaluation, S&S Company issued a notice that stated: For our Company... manufacturing inventory is outside the scope of revaluation, excluding special exceptions (Investigation Report, page 281). S&S Company was the only Toshiba unit to exclude manufacturing inventory from Toshiba's inventory devaluation rules. The Company's decision to devalue depended on whether the inventory constituted sales inventory and whether it was "active" inventory. Whether the inventory was "active" was determined at the quarterly meeting in which the applicable inventory was proposed by the sales promotion departments in each division and decided by the S&S Company's sales supervision department (Investigation Report, page 282). Table I below presents the book values of ASIC inventories of S&S Company at the end of FY 2009 through FY 2013: Table 1: Book Values of ASIC Inventories (amounts in millions ¥) Ending Inventory 18 Key ASIC Products Other ASIC Products FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 3,700 4,600 3,600 3,500 600 1,500 1,500 1,500 1,500 0 Total Year 5,200 FY 2009 FY 2010 FY 2011 FY 2012 S&S Company recognized its inability to sell ASIC products rather late. Besides, almost 60% of ASIC inventory was classified as manufacturing inventory and thereby excluded from inventory devaluation rules as mentioned above (Investigation Report, page 278). At a budget review committee meeting in March 2013, S&S Company decided to discontinue further production of ASIC products and shift the focus to produce general-purpose Application-Specific Standard Products (ASSPs). Following that decision, in September 2013, S&S Company's senior managers decided to dispose of most of the ASIC inventory of ¥4,400 million and record the entire amount as a disposal loss. Of this, ¥2,900 million related to the 18 Key ASIC products. The Investigation Report concluded that S&S Company should have written down the inventory values of the 18 Key ASIC products to ¥1,900, ¥1,200, 200, in FY 2009, FY 2010, FY 2011, respectively, and to zero in FY 2012, and FY 2013. Also, it should have written down the entire ¥1,500 million of "Other ASIC inventory" in FY 2009 to zero. Requirement 1 b. Calculate the ASIC inventory amounts (in million) that S&S Company should have reported at the end of each year from FY 2009 to FY 2013, and the effect of the incorrect recording of ASIC inventory on S&S Company's reported pre-tax income for FY 2010 to FY 2013. Assume that there were no purchases of non-ASIC products from FY 2010 to FY 2013 and no inventory misstatements occurred before FY 2009. Use the format below to provide your answer. Year-end inventory 6,100 5,100 Appropriate Amounts 18 Key Other ASIC ASIC Products Products Total 5,000 5,200 6,100 5,100 5,000 600 Difference between Income 'appropriate' effect for the year S&S Company amounts and reported "reported' amounts Is income for the year understated, overstated, or unaffected. Toshiba classified its inventory into two categories. Goods were classified as "sales inventory" after the manufactured goods were inspected for quality and moved into a warehouse. Sales managers had oversight over this "sales inventory." Goods not classified as "sales inventory" were considered "manufacturing inventory" for which the operating managers were responsible. In other words, the "manufacturing inventory" included work-in-progress (WIP) and finished goods inventory not yet inspected. Toshiba valued its inventories at the lower of cost or net realizable value in its financial statements, cost being determined principally by the average method.* Toshiba's Accounting Manual stated that the inventory should be devalued to the expected disposal value (including zero or a memorandum value) once the sales of that inventory could no longer be expected as planned. On December 27, 2008, the Corporate Finance & Accounting Division communicated the corporate rules about inventory devaluation to each Company. Inventories at Toshiba's Semiconductor Business (S&S Company) Toshiba's semiconductor business (S&S Company) manufactured integrated circuits customized for a particular use, called Application Specific Integrated Circuits (ASICs). Of the 7000 different ASIC products manufactured by Toshiba, 18 were considered "Key ASIC Products", the remaining being considered "Other ASIC Products." ASIC products were manufactured without waiting for a formal order from a customer. Instead, they were manufactured using the prospects of such orders, based on communications with customers. The demand for S&S Company's ASIC products started to decline in FY 2009 due to the reduced demand for electronic products in which the ASIC products were used. Also, some of *Toshiba follows accounting principles generally accepted in Japan; however, certain adjustments and reclassifications are made in its consolidated financial statements to conform to US GAAP. (Accounting Standards Board of Japan, accessed at: https://www.asb.or.jp/en/ip-gaap/about.html) It specified separate rules for the devaluation of inventory items outside of the normal operating cycle (for instance, inventory of maintenance parts and service spare parts) because such inventory items needed to be held for a longer time due to customer agreements. | S&S Company's customers (manufacturers of electronic products) started purchasing their components from other manufacturers instead of Toshiba. Changes in the technology used by its customers also exacerbated S&S Company's demand situation. For instance, one of the 18 Key ASIC products was exclusively used in a specific customer's microprocessor. Later, the customer changed its technology and no longer needed this product. Believing that it could sell the product to other customers, S&S Company continued to promote its sale and hold the entire inventory, almost 30% of the 18 Key ASIC products, in its stock. S&S Company's assumption that it could sell ASIC products to other customers was unrealistic. A comparison of the planned sales to actual sales for one of the 18 Key ASIC products - JTSCX2-AS - illustrates this. For FY 2010, the sales of this product were projected to be ¥16.0 billion, but the actual sales totaled ¥14.2 billion. Despite not meeting the projections in FY 2010. S&S Company increased the sales forecast for JT5CX2-AS in FY 2011 to 27.1 billion. The actual sales of the product in FY 2011 fell to almost zero. 4 S&S Company's Inventory Devaluation Rules S&S Company's devaluation rules differed from Toshiba's corporate accounting rules. As an example, in March 2009, in response to the corporate accounting rules for devaluation, S&S Company issued a notice that stated: For our Company... manufacturing inventory is outside the scope of revaluation, excluding special exceptions (Investigation Report, page 281). S&S Company was the only Toshiba unit to exclude manufacturing inventory from Toshiba's inventory devaluation rules. The Company's decision to devalue depended on whether the inventory constituted sales inventory and whether it was "active" inventory. Whether the inventory was "active" was determined at the quarterly meeting in which the applicable inventory was proposed by the sales promotion departments in each division and decided by the S&S Company's sales supervision department (Investigation Report, page 282). Table I below presents the book values of ASIC inventories of S&S Company at the end of FY 2009 through FY 2013: Table 1: Book Values of ASIC Inventories (amounts in millions ¥) Ending Inventory 18 Key ASIC Products Other ASIC Products FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 3,700 4,600 3,600 3,500 600 1,500 1,500 1,500 1,500 0 Total Year 5,200 FY 2009 FY 2010 FY 2011 FY 2012 S&S Company recognized its inability to sell ASIC products rather late. Besides, almost 60% of ASIC inventory was classified as manufacturing inventory and thereby excluded from inventory devaluation rules as mentioned above (Investigation Report, page 278). At a budget review committee meeting in March 2013, S&S Company decided to discontinue further production of ASIC products and shift the focus to produce general-purpose Application-Specific Standard Products (ASSPs). Following that decision, in September 2013, S&S Company's senior managers decided to dispose of most of the ASIC inventory of ¥4,400 million and record the entire amount as a disposal loss. Of this, ¥2,900 million related to the 18 Key ASIC products. The Investigation Report concluded that S&S Company should have written down the inventory values of the 18 Key ASIC products to ¥1,900, ¥1,200, 200, in FY 2009, FY 2010, FY 2011, respectively, and to zero in FY 2012, and FY 2013. Also, it should have written down the entire ¥1,500 million of "Other ASIC inventory" in FY 2009 to zero. Requirement 1 b. Calculate the ASIC inventory amounts (in million) that S&S Company should have reported at the end of each year from FY 2009 to FY 2013, and the effect of the incorrect recording of ASIC inventory on S&S Company's reported pre-tax income for FY 2010 to FY 2013. Assume that there were no purchases of non-ASIC products from FY 2010 to FY 2013 and no inventory misstatements occurred before FY 2009. Use the format below to provide your answer. Year-end inventory 6,100 5,100 Appropriate Amounts 18 Key Other ASIC ASIC Products Products Total 5,000 5,200 6,100 5,100 5,000 600 Difference between Income 'appropriate' effect for the year S&S Company amounts and reported "reported' amounts Is income for the year understated, overstated, or unaffected.

Expert Answer:

Answer rating: 100% (QA)

Answer To calculate the ASIC inventory amounts that SS Company shoul... View the full answer

Related Book For

Auditing A Practical Approach with Data Analytics

ISBN: 978-1119401742

1st edition

Authors: Raymond N. Johnson, Laura Davis Wiley, Robyn Moroney, Fiona Campbell, Jane Hamilton

Posted Date:

Students also viewed these accounting questions

-

Explain the (a) lower of cost or net realizable value (LCNRV) approach and the (b) lower of cost or market (LCM) approach to valuing inventory.

-

Explain how the lower of cost or net realizable value method is applied on a group basis.

-

Lower of Cost or Market Frost Companys inventory records for the years 2016 and 2017 reveal the cost and market of the January 1, 2016, inventory to be $125,000. On December 31, 2016, the cast of...

-

If a particular glucose fermentation process is 87.0% efficient, how many grams of glucose would be required for the production of 51.0 g of ethyl alcohol (C 2 H 5 OH)? C 6 H 12 O 6 2C 2 H 5 OH +...

-

City Technology began the year with inventory of $244,000 and purchased $1,540,000 of goods during the year. Sales for the year are $4,000,000, and City's gross profit percentage is 60% of sales....

-

At the end of 2017, Solar Power had total assets of $17.8 billion and total liabilities of $9.1 billion. Included among the assets were property, plant, and equipment with a cost of $4.5 billion and...

-

In Exercises 1 to 4, it may be helpful to draw a figure such as Figure 5.5. Figure 5.5. Using the normal curve table, determine the area of the standard normal distribution that is between the mean...

-

The wearever Shoe Company is going to open a new branch at a mall, and company manager are attempting to determine how many sales-people to hire Based on an analysis of mall traffic. The company...

-

The following year-end information is taken from the December 31 adjusted trial balance and other records of Leone Company. Advertising expense Depreciation expense-Office equipment $ 28,750 7,250...

-

You receive the following letter. Quark Pty Ltd. 500 Mowbray ROAD LANE COVE, NSW 2066 8 Sept 2018 Greetings, Quark Pty Ltd is a trader of machine parts. Its annual turnover in the last five years...

-

The analogy in the picture depicts: Select one: a. A trapdoor function encryption b. A Public Key encryption c. A Symmetric encryption d. None of the above Sender's padlock Sender 1. Sender secures...

-

Give three examples of objects that belong to the String class. Give an example of an object that belongs to the PrintStream class. Name two methods that belong to the String class but not the...

-

What side effect, if any, do the following three methods have? public class Coin: { } public public void print () System.out.println(name + } } public void print (PrintStream stream) {...

-

Declare and initialize variables for holding the price and the description of an article that is available for sale.

-

Find the errors in the following statements: a. b. c. d. Rectangle r= (5, 10, 15, 20);

-

For faster sorting of letters, the U.S. Postal Service encourages companies that send large volumes of mail to use a bar code denoting the ZIP code (see Figure 8). The encoding scheme for a...

-

1. Find the solution to the following IVP using the method of integrating factors (i.e., the form below is linear) tyl - 2y = t5sin(2t) t + 4t4 3 Y() = 374

-

1. Below is depicted a graph G constructed by joining two opposite vertices of C12. Some authors call this a "theta graph" because it resembles the Greek letter 0. a. What is the total degree of this...

-

Identify and briefly describe the five steps of performing ADA and place them in the proper order.

-

A detailed listing of the specific audit procedures to be used to gather evidence for an account is called the: a. Permanent file. b. Audit strategy. c. Audit program. d. Accounting records.

-

Columbia Metal Fabricators (CMF) makes steel components for the construction industry. It specializes in extreme precision manufacturing where tolerances are measured in distances of less than one...

-

Consider the situation illustrated in Figure 25. 11. A positively charged particle is lifted against the uniform electric field of a negatively charged plate. Ignoring any gravitational interactions,...

-

A positively charged particle is moved from point A to point B in the electric field of the massive, stationary, positively charged object in Figure 25. 12. (a) Is the electrostatic work done on the...

-

Two metallic spheres A and B are placed on nonconducting stands. Sphere A carries a positive charge, and sphere B is electrically neutral. The two spheres are connected to each other via a wire, and...

Study smarter with the SolutionInn App