Question: Transactions 1. 2. 3. 4. 5. 6. 7. 8. An insurance policy was purchased on February 28 for $1,620. The insurance policy was for one

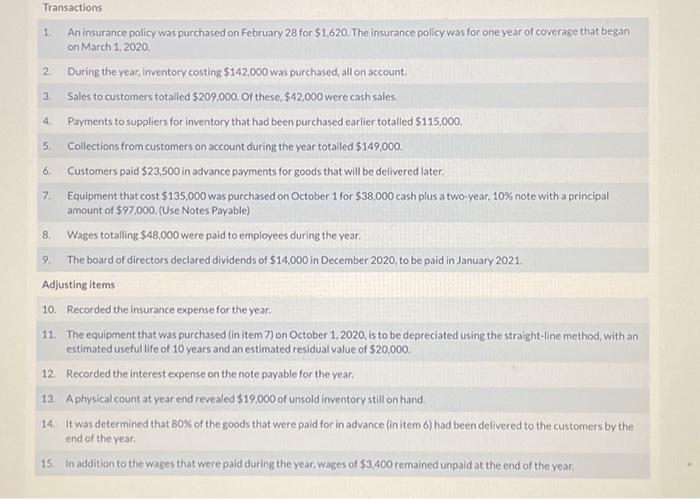

Transactions 1. An insurance policy was purchased on February 28 for $1,620. The insurance policy was for one year of coverage that began on March 1,2020 2. During the year, inventory costing $142,000 was purchased, all on account. 3. Sales to customers totalled $209,000. Of these, $42,000 were cash sales. 4. Payments to suppliers for inventory that had been purchased earlier totalled $115,000. 5. Collections from customers on account during the year totalled $149,000. 6. Customers paid $23,500 in advance payments for goods that will be delivered later. 7. Equipment that cost $135,000 was purchased on October 1 for $38,000 cash plus a two-year, 10% note with a principal amount of $97,000. (Use Notes Payable) 8. Wages totalling $48,000 were paid to employees during the year. 9. The board of directors declared dividends of $14,000 in December 2020 , to be paid in January 2021. Adjusting items 10. Recorded the insurance expense for the year. 11. The equipment that was purchased (in item 7) on October 1,2020 , is to be depreciated using the straight-line method, with an estimated useful life of 10 years and an estimated residual value of $20,000. 12. Recorded the interest expense on the note payable for the year. 13. A physical count at year end revealed $19,000 of unsold inventory still on hand 14. It was determined that 80% of the goods that were paid for in advance (in item 6 ) had been delivered to the customers by the end of the year. 15. In addition to the wages that were paid during the year, wages of $3.400 remained unpaid at the end of the year. Transactions 1. An insurance policy was purchased on February 28 for $1,620. The insurance policy was for one year of coverage that began on March 1,2020 2. During the year, inventory costing $142,000 was purchased, all on account. 3. Sales to customers totalled $209,000. Of these, $42,000 were cash sales. 4. Payments to suppliers for inventory that had been purchased earlier totalled $115,000. 5. Collections from customers on account during the year totalled $149,000. 6. Customers paid $23,500 in advance payments for goods that will be delivered later. 7. Equipment that cost $135,000 was purchased on October 1 for $38,000 cash plus a two-year, 10% note with a principal amount of $97,000. (Use Notes Payable) 8. Wages totalling $48,000 were paid to employees during the year. 9. The board of directors declared dividends of $14,000 in December 2020 , to be paid in January 2021. Adjusting items 10. Recorded the insurance expense for the year. 11. The equipment that was purchased (in item 7) on October 1,2020 , is to be depreciated using the straight-line method, with an estimated useful life of 10 years and an estimated residual value of $20,000. 12. Recorded the interest expense on the note payable for the year. 13. A physical count at year end revealed $19,000 of unsold inventory still on hand 14. It was determined that 80% of the goods that were paid for in advance (in item 6 ) had been delivered to the customers by the end of the year. 15. In addition to the wages that were paid during the year, wages of $3.400 remained unpaid at the end of the year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts