Question: (a) Given a European put option on a non-dividend-paying stock with current price $20, strike price $18, risk-free interest rate 15% per annum, volatility 40%

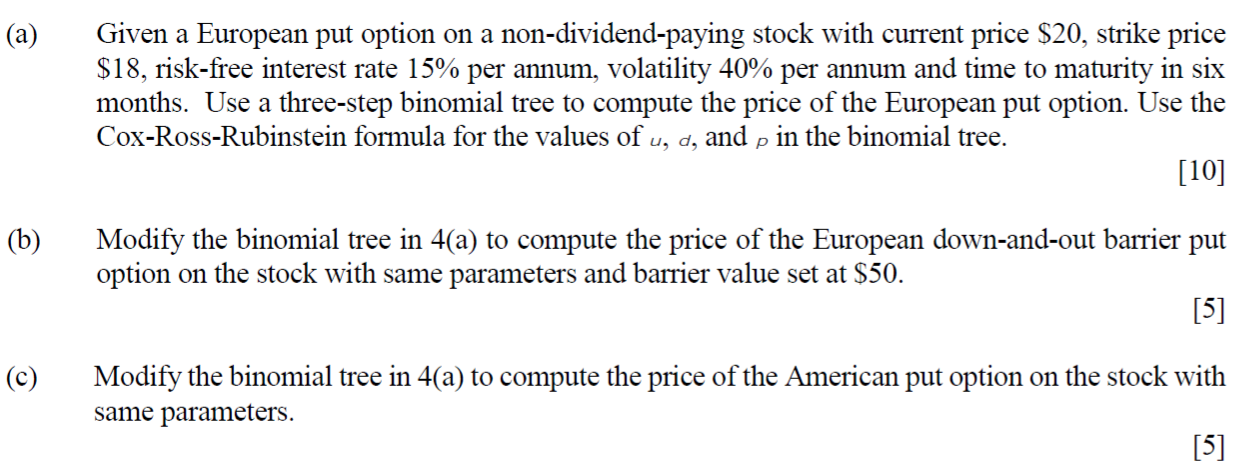

(a) Given a European put option on a non-dividend-paying stock with current price $20, strike price $18, risk-free interest rate 15% per annum, volatility 40% per annum and time to maturity in six months. Use a three-step binomial tree to compute the price of the European put option. Use the Cox-Ross-Rubinstein formula for the values of u, d, and p in the binomial tree. [10] (b) Modify the binomial tree in 4(a) to compute the price of the European down-and-out barrier put option on the stock with same parameters and barrier value set at $50. [5] (c) Modify the binomial tree in 4(a) to compute the price of the American put option on the stock with same parameters. [5] (a) Given a European put option on a non-dividend-paying stock with current price $20, strike price $18, risk-free interest rate 15% per annum, volatility 40% per annum and time to maturity in six months. Use a three-step binomial tree to compute the price of the European put option. Use the Cox-Ross-Rubinstein formula for the values of u, d, and p in the binomial tree. [10] (b) Modify the binomial tree in 4(a) to compute the price of the European down-and-out barrier put option on the stock with same parameters and barrier value set at $50. [5] (c) Modify the binomial tree in 4(a) to compute the price of the American put option on the stock with same parameters. [5]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts