Question: Consider the following program. This program is designed to price specific types of options. The arguments are as follows: 50: current stock price, K: strike

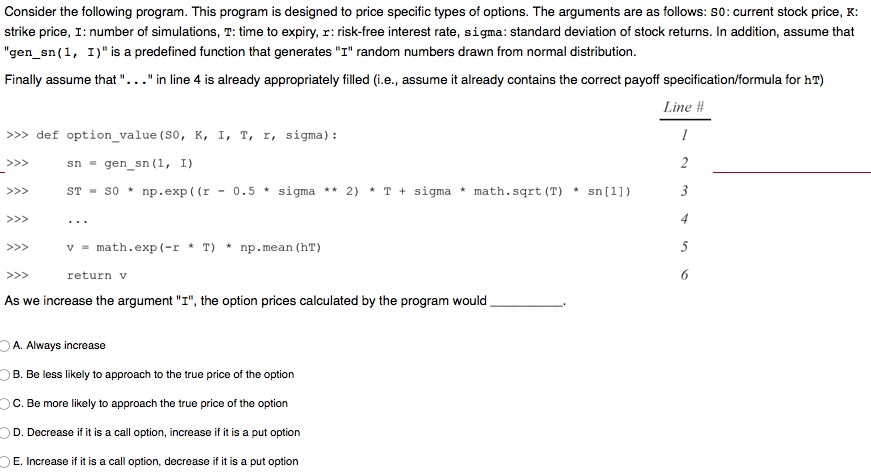

Consider the following program. This program is designed to price specific types of options. The arguments are as follows: 50: current stock price, K: strike price, I: number of simulations, T: time to expiry, r: risk-free interest rate, sigma: standard deviation of stock returns. In addition, assume that "gen_sn(1, 1)" is a predefined function that generates "I" random numbers drawn from normal distribution. Finally assume that "..." in line 4 is already appropriately filled (i.e., assume it already contains the correct payoff specification/formula for hT) Line # >>> def option_value (S0, K, I, T, I, sigma): 1 2 sn = gen_sn(1, I) ST - SO * np.exp ((r - 0.5 * sigma ** 2) * T + sigma * math.sqrt(T) * sn[1]) 3 4 v = math.exp(-r* T) np.mean (hr) 5 return v 6 As we increase the argument "I", the option prices calculated by the program would A. Always increase B. Be less likely to approach to the true price of the option C. Be more likely to approach the true price of the option D. Decrease if it is a call option, increase if it is a put option E. Increase if it is a call option, decrease if it is a put option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts