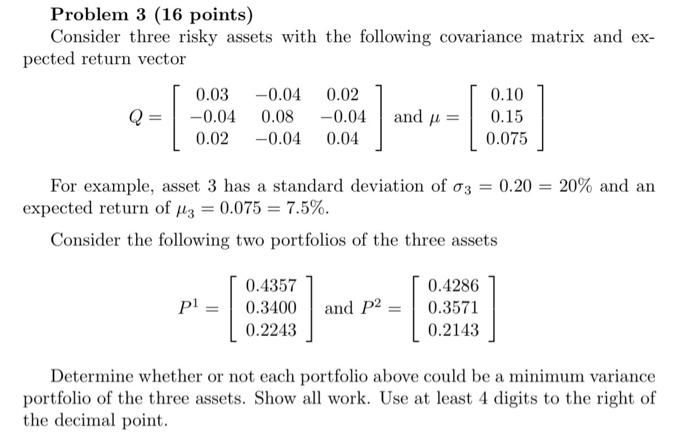

Question: Problem 3 (16 points) Consider three risky assets with the following covariance matrix and ex- pected return vector 0.03 -0.04 0.02 0.10 -0.04 0.08 -0.04

Problem 3 (16 points) Consider three risky assets with the following covariance matrix and ex- pected return vector 0.03 -0.04 0.02 0.10 -0.04 0.08 -0.04 and p = 0.15 0.02 -0.04 0.04 0.075 For example, asset 3 has a standard deviation of 93 0.20 = 20% and an expected return of pz = 0.075 = 7.5%. Consider the following two portfolios of the three assets pl 0.4357 0.3400 0.2243 and p2 0.4286 0.3571 0.2143 Determine whether or not each portfolio above could be a minimum variance portfolio of the three assets. Show all work. Use at least 4 digits to the right of the decimal point. Problem 3 (16 points) Consider three risky assets with the following covariance matrix and ex- pected return vector 0.03 -0.04 0.02 0.10 -0.04 0.08 -0.04 and p = 0.15 0.02 -0.04 0.04 0.075 For example, asset 3 has a standard deviation of 93 0.20 = 20% and an expected return of pz = 0.075 = 7.5%. Consider the following two portfolios of the three assets pl 0.4357 0.3400 0.2243 and p2 0.4286 0.3571 0.2143 Determine whether or not each portfolio above could be a minimum variance portfolio of the three assets. Show all work. Use at least 4 digits to the right of the decimal point

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts