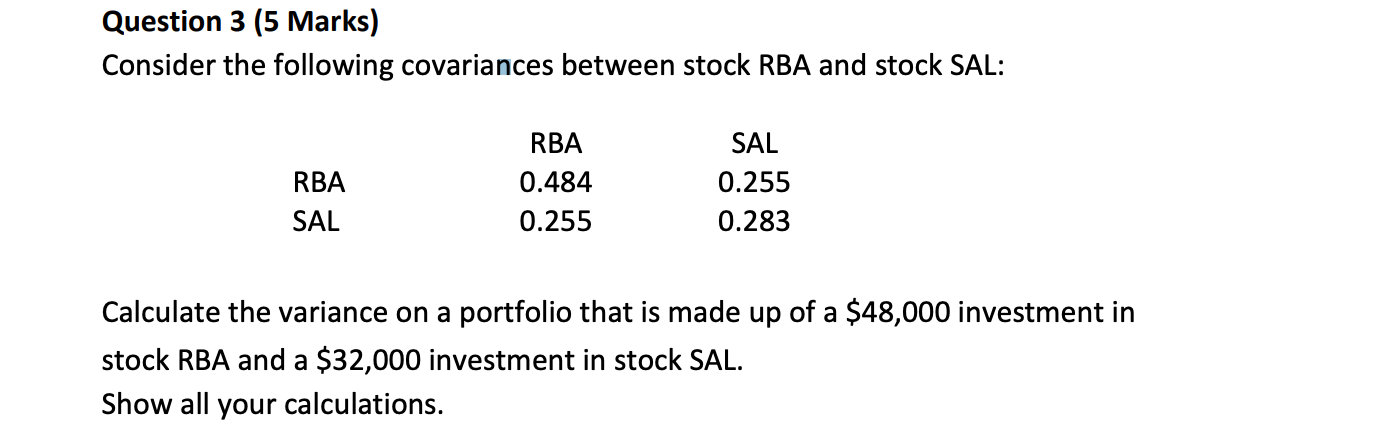

Question: Question 3 (5 Marks) Consider the following covariances between stock RBA and stock SAL: RBA SAL RBA 0.484 0.255 SAL 0.255 0.283 Calculate the variance

Question 3 (5 Marks) Consider the following covariances between stock RBA and stock SAL: RBA SAL RBA 0.484 0.255 SAL 0.255 0.283 Calculate the variance on a portfolio that is made up of a $48,000 investment in stock RBA and a $32,000 investment in stock SAL. Show all your calculations. Question 3 (5 Marks) Consider the following covariances between stock RBA and stock SAL: RBA SAL RBA 0.484 0.255 SAL 0.255 0.283 Calculate the variance on a portfolio that is made up of a $48,000 investment in stock RBA and a $32,000 investment in stock SAL. Show all your calculations

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock