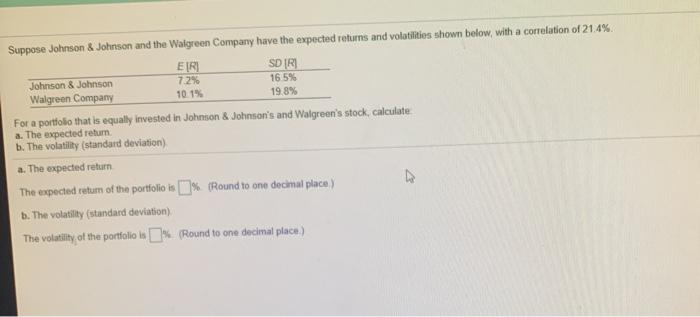

Question: Suppose Johnson & Johnson and the Walgreen Company have the expected returns and volatilities shown below, with a correlation of 21.4% E[RI SD [RI Johnson

Suppose Johnson & Johnson and the Walgreen Company have the expected returns and volatilities shown below, with a correlation of 21.4% E[RI SD [RI Johnson & Johnson 7.2% 16.5% Walgreen Company 10.1% 19 8% For a portfolio that is equally invested in Johnson & Johnson's and Walgreen's stock, calculate a. The expected return b. The volatility (standard deviation) a. The expected return The expected retum of the portfolio is I % (Round to one decimal place) b. The volatilly (standard deviation) The volatility of the portfolio ls . Round to one decimal place)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock